8 May 2023

“Objects in the mirror are not as bad as you thought they were”

After several sub-par quarters and a period of aggressive estimate cuts, Q1 earnings reports have broadly beaten the reduced earnings forecasts. This has triggered not just higher stock prices but a broad and rapid upturn in the pattern of earnings estimate revisions by equity analysts.

With about 85% of the S&P 500 now having reported Q1 earnings, Factset reports that 79% have beaten consensus earnings estimates. Q1 earnings are running about -2.4% below the year-ago quarter, which while still negative, is notably better than the -6.7% decline that had been projected as of March 31st.

For comparison:

For Q4 2022, 70% of the S&P 500 beat consensus earnings forecasts, and Q4 earnings were down -4.6% from the year-ago quarter.

For Q3 2022, 71% of the S&P 500 beat estimates, and earnings were up 2.4% from the year-ago quarter.

But more important than the backward-looking results themselves is the guidance from company management and analysts’ resultant changes to future earnings estimates.

In that regard, the news is clearly positive. Analysts have heard better reports and are responding.

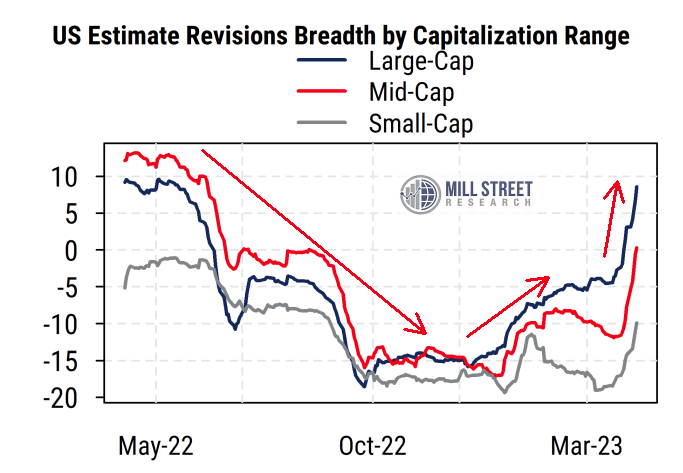

The chart below is based on Mill Street’s broad 2300-stock US universe, and is broken into three size categories based on market cap:

Large-caps: top 20% of stocks

Mid-caps: next 30% of stocks

Small-caps: bottom 50% of stocks

Source: Mill Street Research, Factset

The data show the average estimate revisions breadth within each category (revisions are equally weighted within each category, i.e., the mega-cap stocks do not get more weight than others). Revisions breadth is the proportion of analysts covering a stock who have raised their EPS estimates for the next 12 months net of those who have lowered estimates, based on estimates revised within the last 100 calendar days. So breadth can range between -100% (all analysts cutting estimates most recently) and +100% (all analysts raising estimates), with 0% indicating a balance between positive and negative revisions. We then average the breadth reading for each stock across all stocks in the group.

We can see that for most of this year, large-caps have had better (less negative/more positive) revisions breadth than the smaller size categories, and the gap had been widening before Q1 earnings reports. But the impact of Q1 earnings reports is quite stark: the “hockey stick” jumps in all three revisions series is the analyst response to the earnings news and guidance. This follows a long stretch of deteriorating and net negative revisions, with October-January being heavily negative across the board.

Revisions have jumped recently for all three categories, with large-caps remaining in the lead. Large-caps (blue line) had negative average revisions (more cuts than raises) since early summer last year, but have jumped into positive territory (more raises than cuts) recently.

Mid-caps (red line) have also surged, and are just now crossing the zero line from net negative to net positive revisions breadth.

The lagging small-caps (grey line) have also turned up sharply. This is occurring despite the drag from severe weakness in many mid- and small-cap regional banks recently, which make up a substantial proportion of mid- and small-cap stocks.

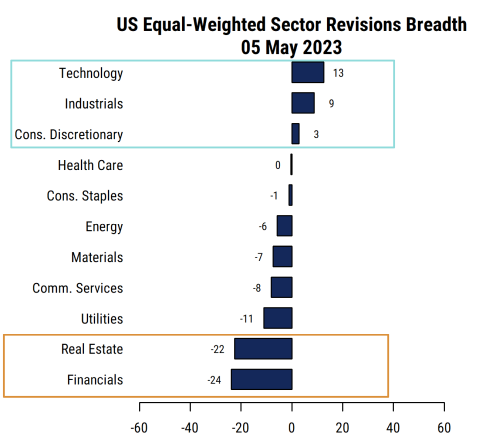

Turning from size-based trends to sector aggregates, the chart below shows the average revisions breadth for our US stock universe broken down into the 11 GICS sectors.

Source: Mill Street Research, Factset

We can see that the large and pro-cyclical Technology, Industrials, and Consumer Discretionary sectors are leading the strength in revisions, and are now all showing net positive average revisions breadth.

Perhaps not surprisingly, the Financials sector is the weakest now, weighed down by persistent negative revisions in the Banks industry. Real Estate has been among the weakest sectors for months now, still hampered by both rising interest rates and weak demand for commercial real estate in the post-COVID world.

The message from the trend in revisions and the sector profile of the revisions leadership is that bottom-up corporate earnings trends are improving and are being led by pro-cyclical sectors rather than defensive (counter-cyclical or non-cyclical) sectors. This pattern would be extremely unusual to see if the US economy was indeed about to slide into a substantial recession imminently, or the equity market was about to plunge. Those things may happen again some day, but perhaps not just yet.

Along with our views on the macroeconomic trend, inflation, the Fed, and investor sentiment, this bottom-up view of the trend in estimate revisions (rather than the level of forecasts, or analyst buy/hold/sell recommendations) supports our relatively positive view of equities and our view that the US economy is still in the process of slowing but not heading into recession right now, along with a selective pro-cyclical sector bias in equity allocation.

It also more broadly suggests that the severe negativity among investors and analysts late last year and early this year was excessive, and reminds us that the news doesn’t have to be “good” (i.e., earnings are still slightly down from a year ago), it just needs to be “better than expected” for markets and analysts to respond favorably.