15 September 2022

The Fed is raising rates as fast as it can, and the Treasury yield curve is flat or inverted. Is this a bad scenario for US banks? Not right now, since the rates banks pay on deposits have risen much less than rates on Treasury bills or the fed funds rate, as is often the case. And wider credit spreads on corporate loans have also helped improve lending margins. Our stock rankings show higher readings for the Financials sector, helped by strong earnings estimate revisions, particularly in mid- and smaller-cap banks and thrifts. Readings above zero on the chart below indicate analysts raising estimates more in Banks than in the overall US market, and recent readings have been far above average.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

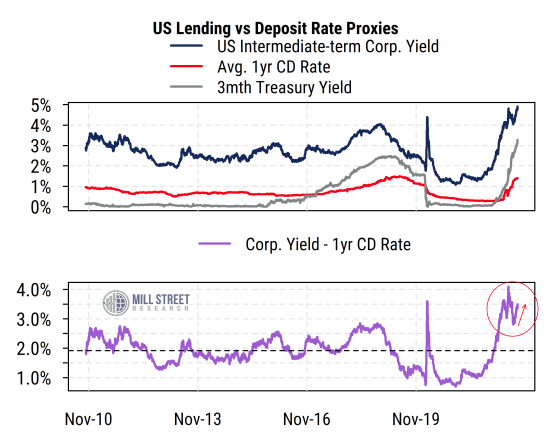

Indeed, despite the flat Treasury yield curve, some proxies of bank lending spreads are historically favorable right now. While banks make many types of loans at varying rates, the average intermediate-term investment grade corporate bond yield is one proxy for lending rates. And the average rate on a one-year certificate of deposit is a proxy for the rates banks pay depositors (cost of funds).

Using these rates we can construct a rough proxy for lending spreads for traditional banks and thrifts (i.e., those that do not have significant capital markets divisions that are under pressure from falling stock and bond prices). As shown below, the spread (purple line, bottom section) has risen recently and is near its highest readings the last 10 years or more.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

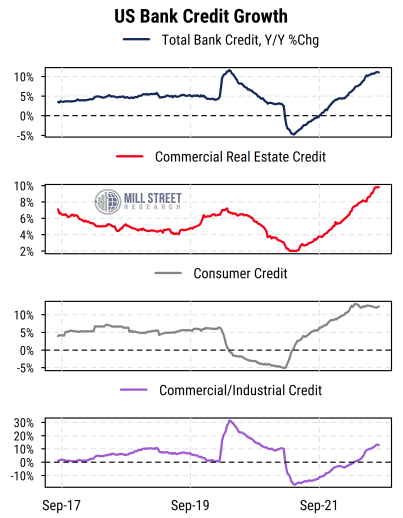

Intermediate- and longer-term interest rates (bond yields, mortgage rates, etc.) are at their highest since 2007-08 now, with corporate loans trading at wider spreads over Treasuries than they were last year. And while mortgage activity has slowed sharply due to higher rates and higher house prices, overall bank lending continues to grow across other categories, including commercial real estate, consumer credit, and commercial/industrial credit.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

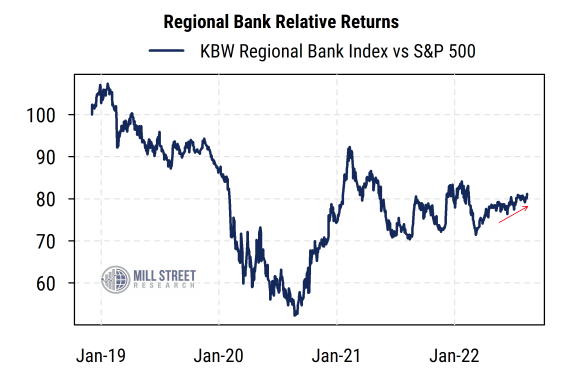

Regional banks have been outperforming the market recently, but not to an excessive degree thus far. The KBW Regional Bank index is a 50-stock index of US banks that range in market value from about $1 to $10 billion. They are representative of the mid-size banks that typically focus on traditional lending rather than capital markets, advisory, or other business lines. The KBW index has been outperforming the S&P 500 since April, but the relative return series remains within the broad range it has inhabited for much of the last two years. If relative earnings estimate revisions remain above-average and the interest rate and lending backdrop holds up, the mid- and smaller-cap lenders could continue the recent trend of outperformance.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg