One of the most notable market trends in recent weeks has been the corrective action in the formerly high-flying US large-cap Growth stocks. The dominant Tech-oriented companies that have been responsible for much of the gains in US large-cap indices for several months finally saw some significant selling pressure in the first two weeks of September.

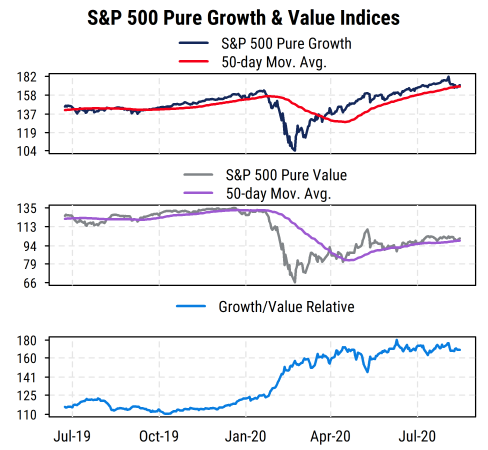

The first chart below shows absolute and relative returns for the S&P 500 Pure Growth and Pure Value indices (i.e., the style indices restricted to stocks that fall entirely into their indicated style, leaving out those with weight in both indices).

Key points:

- The Growth index has been above its 50-day moving average since mid-April (and made new highs recently), but has now returned to that average after its recent correction. Any further declines could raise worries about an intermediate trend change.

- The Value index has failed to even approach its January highs and has made little net progress since early June. It is also sitting near its 50-day average.

- Growth/Value relative returns show little net change in the last two months, following a period of drastic Growth outperformance. This is consistent with our recent sector allocation recommendations to clients that have reduced style-level sector bets in favor of intra-style differences.

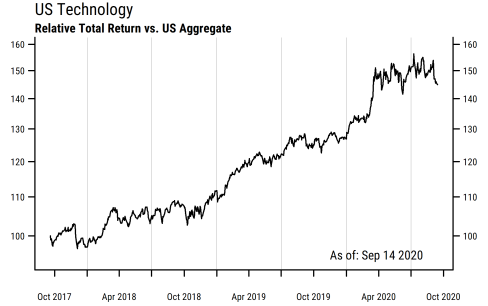

Corroborating the Growth/Value trends is the relative performance of the Growth-heavy Technology sector’s returns. Below is a chart showing our broad (300+ constituents), equal-weighted US Technology sector performance relative to the broad (2000+ constituents) US aggregate.

We can see that after a period of sustained outperformance through the middle of this year, the relative returns for Tech have been much more mixed, and have dipped lately. Investor optimism toward Technology has shown signs of reaching extremes recently, and thus some corrective action is not surprising.

We continue to expect Technology to be a leading sector on an intermediate-term time frame, but both the sector and the overall market may have to go through further choppy trading activity and rotation near-term.