A lot of last year’s losers are this year’s winners, and vice versa, as investors stay in equities but have rotated aggressively. Much of this is not driven by earnings outlooks (at least for the next year or so), but valuation concerns and short-term sentiment and positioning. While some shifts may be reasonable, some of the recent moves look excessive in light of fundamentals.

Investors not sure which kind of risk they want to take

Markets have been more volatile lately, though not all parts of the equity market. Precious metals and crypto assets have seen extreme volatility, and that has filtered through into equity investor sentiment too. At the same time, investors are reevaluating how they think about AI from a corporate earnings standpoint: how much capex is too much (or will actually happen)? Will AI destroy much of the software and IT services industries? Is the demand for memory, storage, etc. excessive, and will it harm the non-AI parts of the Tech space? Given the weight of all the stocks somehow tied to AI in the major indices, these are questions driving the markets day-to-day.

But while Tech-related areas and metals-related areas are seeing high volatility, other parts of the equity market are doing just fine, and the overall economy so far seems to be holding up ok. Crucially, risk appetite remains positive, but many sectors that lagged last year are outperforming this year as money seems to want to stay in the equity market but got nervous about Big Tech/Growth and is now rotating into other areas. Some have fundamental support from earnings estimate revisions, but some do not, and earnings estimate revisions have not been rewarded much lately (after a longer stretch when they were). Notably, much of the Energy sector and Materials sectors outside of metals miners still have relatively weak earnings trends but have had big rallies as money rotates into much smaller sectors that then have outsized moves, and the same is true for Industrials and some Consumer Staples.

Our indicators continue to support Technology and Financials, keeping some overweights in both the Growth and Value camps. Tech is cheaper than it has been in years and still has very strong earnings estimate trends after a lot of Q4 Tech earnings reports. Rotation and sentiment in Tech is intense, and many stocks (largely in Software) with strong revisions are nonetheless underperforming badly due to longer-term concerns. Financials still have solid revisions, are oversold and cheap.

The strongest spaces in our sector/industry work include a mix of Technology, Financials, some Health Care and Discretionary, and the metals miners. The least attractive areas include many traditional cyclical areas in Industrials and Materials (still affected by tariffs and macro trends), some REITs, and oil and gas producers. My work would continue to avoid most commodity exposure (except metals, though that has higher risk). The heavy cyclicals like Machinery, Building Products and commercial transportation remain weak, and I am biased negatively on much of the consumer space (with a few exceptions like parts of the Auto space and Textiles Apparel & Luxury Goods).

Near-panic selling in parts of Tech space amid massive valuation shift and market rotation – our indicators say stay with Tech

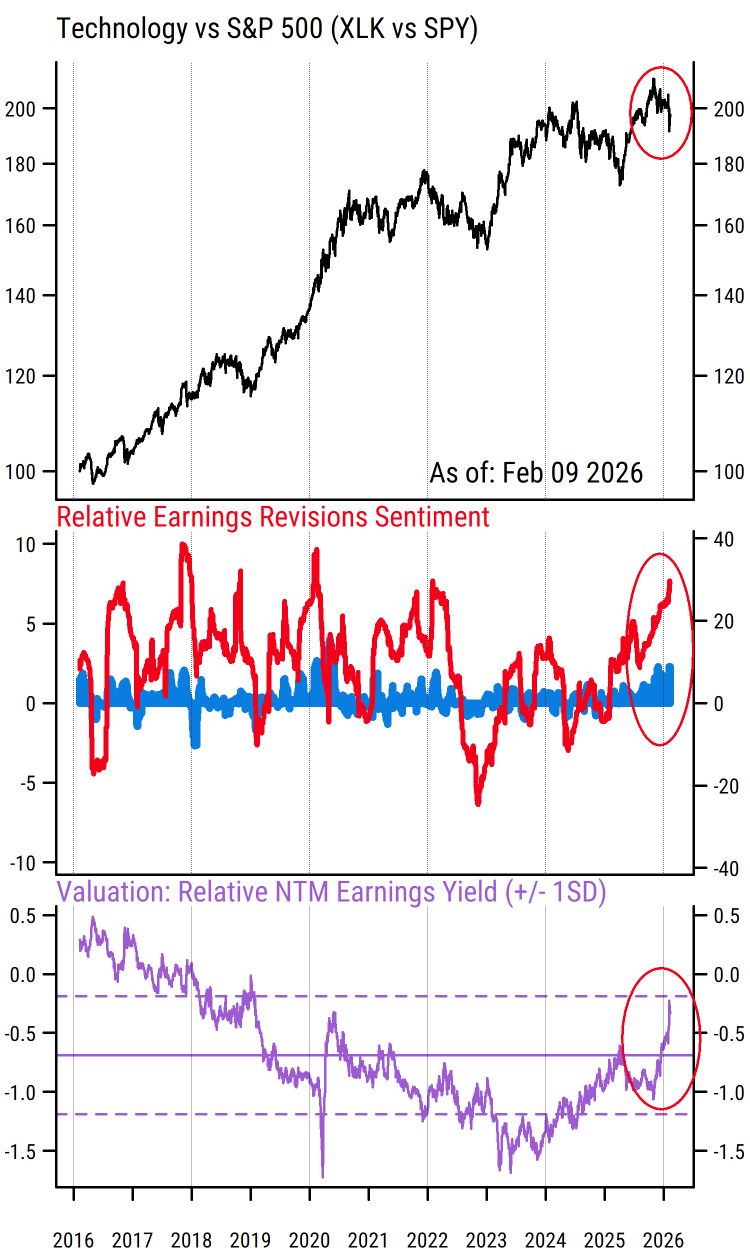

The US Tech space has been buffeted by waves of earnings reports, shifting views on AI, and external sentiment influences from other assets (speculative momentum plays in crypto and precious metals). I continue to overweight Tech despite the volatility as fundamentals remain supportive and valuation has improved sharply.

As always, I focus on the message from our objective indicators rather than headlines or short-term market volatility. As shown in the chart below, the S&P 500 Technology sector’s aggregate estimate revisions metrics (red line, blue bars) remain far above the index average (readings above zero indicate earnings estimate revisions that are stronger than the overall index), and if anything have improved further lately. So analysts are seeing Q4 earnings and the headlines and responding (on average) by raising next-12-month EPS estimates rather than cutting them.

Source: Mill Street Research, Factset

This means that the decline in relative returns has come through entirely in valuation compression. The relative forward earnings yield (purple line) has jumped sharply, now at its highest (cheapest) since 2019-2020. Tech is now only marginally more expensive than the index after seven years of a larger valuation premium.

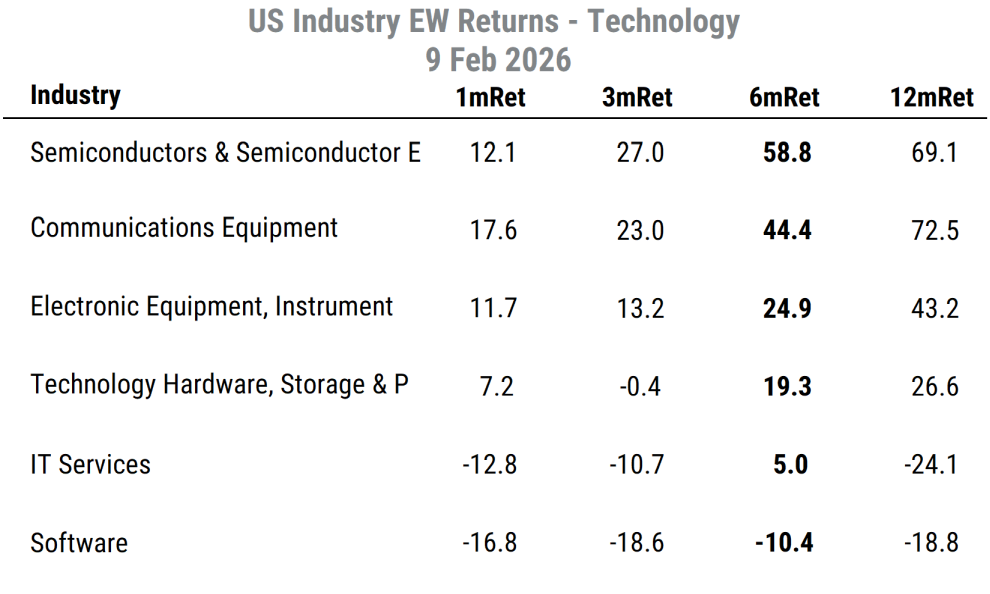

Much of the drag on Tech is focused in the near-panic selling in Software and IT Services industries, which are viewed as having business models threatened by AI. But much of the rest of the sector in the hardware-related areas has been doing ok, or in some cases, very well. Returns for Semiconductors and Communications Equipment have been quite strong, while Electronic Equipment and Tech Hardware are holding up.

Source: Mill Street Research, Factset

EW = equal-weighted

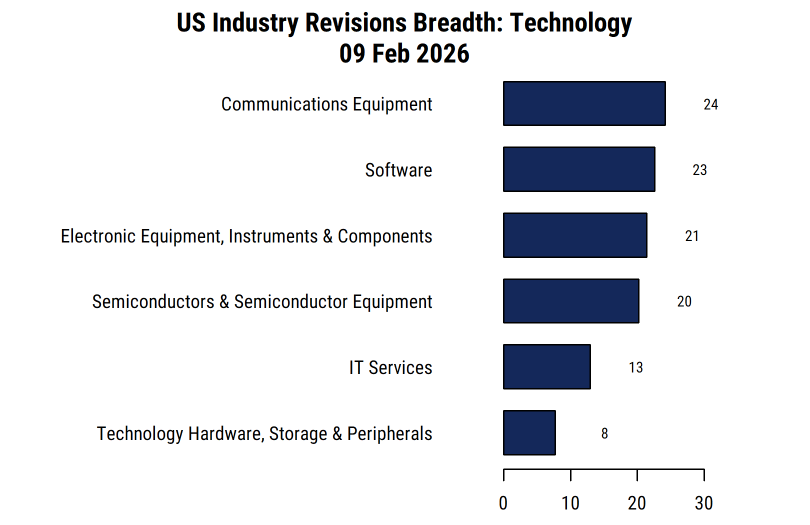

And as shown in the chart below, all six of the US Technology industries have positive equal-weighted estimate revisions breadth, with five of the six having solidly positive (20%+) readings. Revisions breadth is our measure of the proportion of analysts covering a stock that are raising versus lowering their earnings (EPS) forecasts for the next 12 months. It can range from -100% (all analysts cutting estimates) to +100% (all analysts raising estimates). We can then aggregate the breadth readings for each stock in an industry to see how the industry is doing overall.

The solid breadth readings include Software, which is one of the stronger areas, in stark contrast to its severe underperformance. While some software and services companies may indeed see threats to their businesses from AI, and were perhaps a little too highly valued previously, the indicators suggest Tech will recover once the current positioning and sentiment effects fade.

Source: Mill Street Research, Factset

Tech is part of the big Growth to Value rotation, but Growth still has the better earnings support. Watch out for Energy and non-metals Materials.

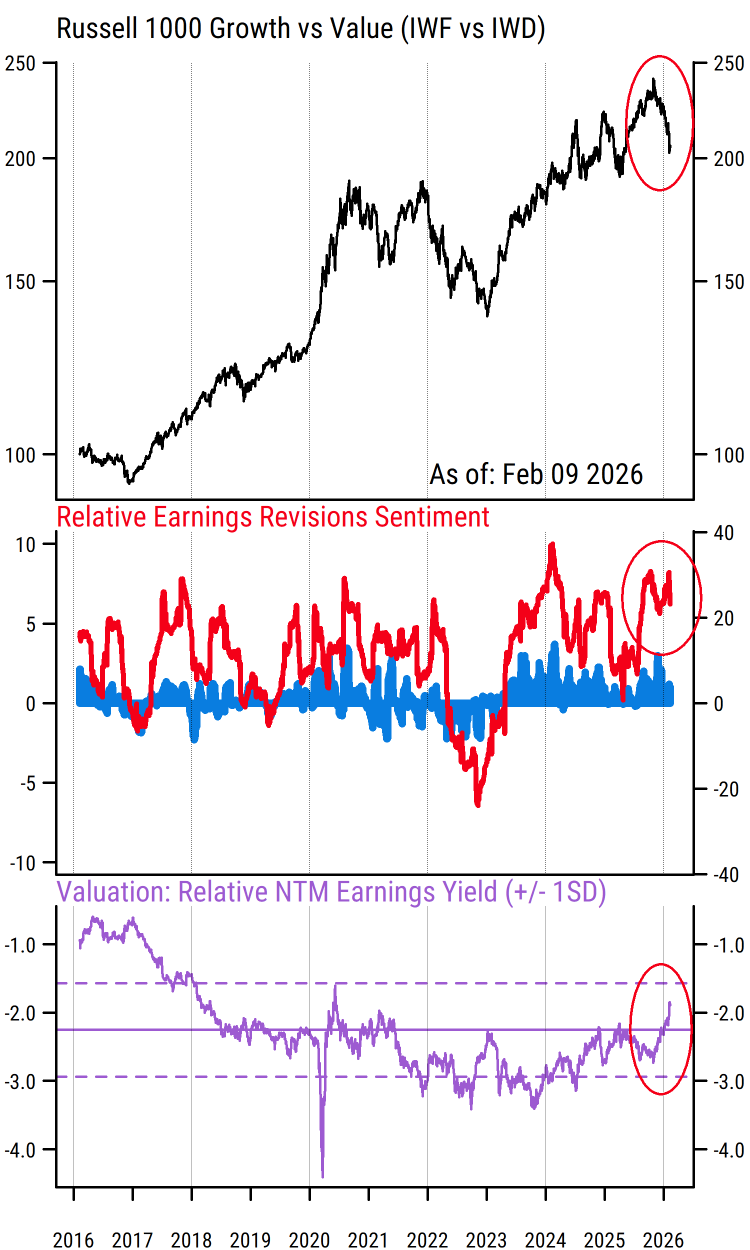

While Tech has gotten most of the focus, it is part of a broader rotation from traditional Growth areas to Value since October. Growth still has stronger earnings than Value and is now much cheaper, so I would not abandon Growth, and be wary of Value-oriented areas that have rallied without earnings support.

Continuing the theme noted above, relative returns have shifted drastically away from Growth areas toward Value areas (and large-caps to smaller-caps) lately, but earnings estimate indicators are still much stronger for Growth in aggregate (chart below).

Source: Mill Street Research, Factset

So the valuation premium that Growth carries (by construction) has narrowed rapidly recently (purple line). The Russell 1000 Growth index is now at its cheapest relative to the Russell 1000 Value since a brief spike in early 2020, and before that since early 2018. Thus the rotation toward Value may not have much further to go unless the relative fundamentals shift meaningfully.

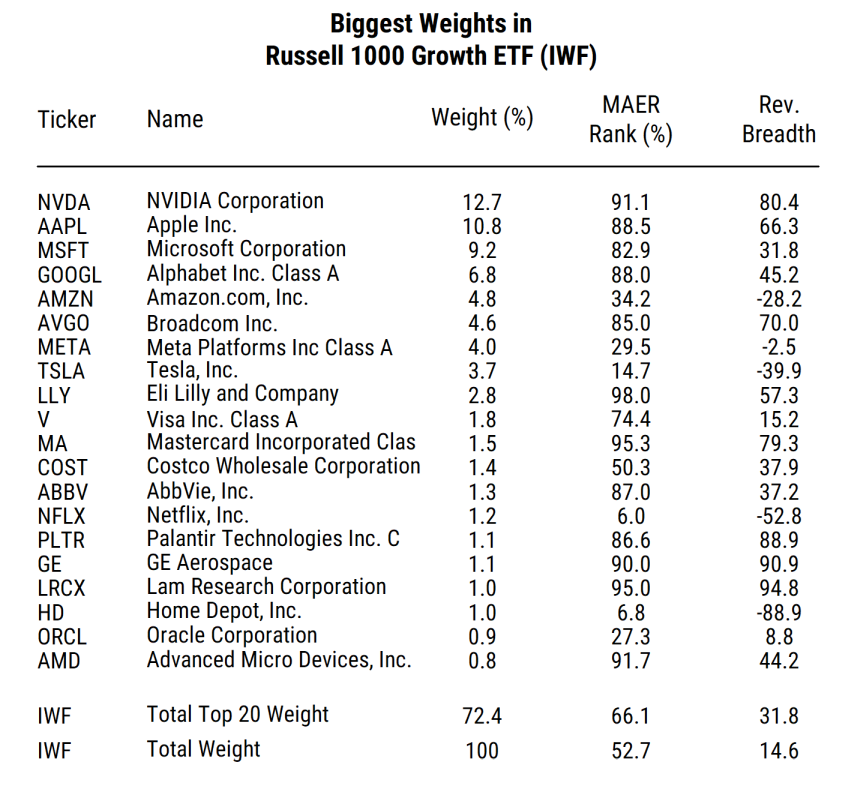

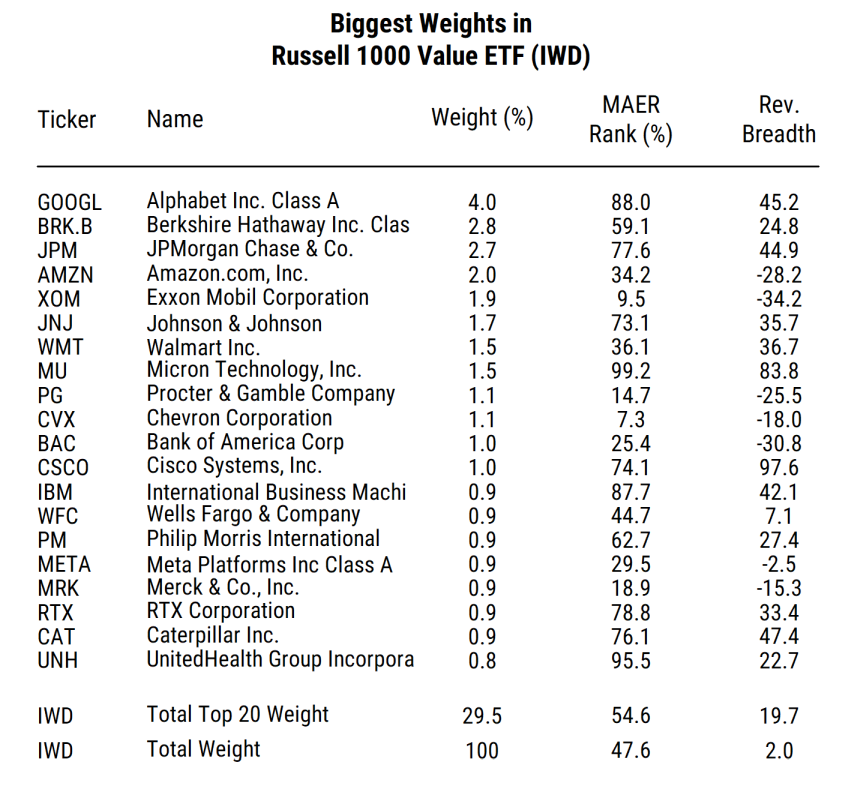

The tables below show the 20 largest stocks in both indices along with their MAER ranking (0-100) and revisions breadth (-100 to +100). The MAER ranking is from our long-standing multi-factor stock selection model, and scores stocks on a percentile basis (0 to 100) based on a combination of earnings estimate trends, price action, and valuation. Higher rankings are more favorable for intermediate-term (1-6 month) relative returns in our work, and stocks ranked above 80th percentile are most attractive in our quantitative model.

The averages for the Growth list are much higher than for the Value list, even though some stocks appear in both (with different weights). The Growth index remains far more concentrated than the Value index (72.4% of weight in the top 20 vs 29.5% in the top 20 Value stocks), and thus “broader” stock market participation tends to be a favorable environment for Value (and smaller-caps).

‘

‘

Source: Mill Street Research, Factset

Areas like Energy, non-metals Materials, parts of Industrials, and some Consumer Staples have seen big rallies, but have little earnings support and thus look riskier in our work now. I am advising clients to be careful in chasing Value too far (focusing on areas like Financials that have more earnings support) and keep some exposure in Growth despite the recent volatility there.

Sam Burns, CFA

Chief Strategist