10 November 2022

UK stocks have been outperforming the global market recently, and our indicators remain supportive, particularly if value and commodity stocks remain in favor.

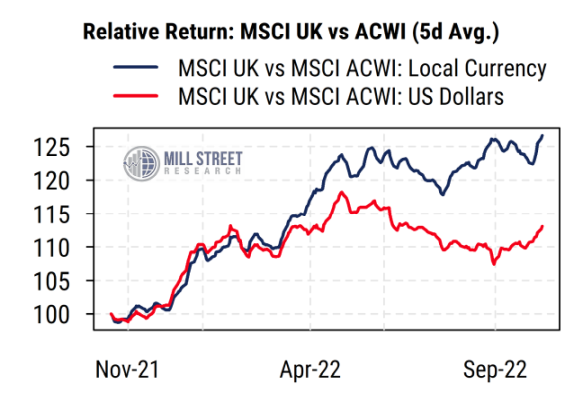

After lagging for much of the last decade, UK stocks have been strongly outperforming the global market this year in local currency terms, and even in US dollar terms more recently. We have been overweight the UK in our regional allocation guidance since March and remain so based on our bottom-up indicators.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

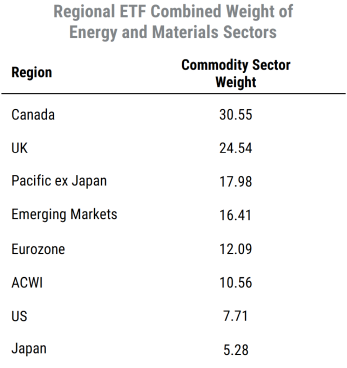

The major large-cap UK indices (the FTSE-100 and the MSCI UK Index) are more heavily weighted toward Value-oriented stocks and commodity-related stocks. Commodity-related stocks, especially those tied to oil, have outperformed dramatically this year, as part of a broader trend of outperformance by Value stocks globally.

The MSCI UK Index (tracked by the US-listed iShares MSCI United Kingdom ETF, ticker EWU) has 24.5% of its weighting in the commodity-related Energy and Materials sectors combined, as shown in the table below. For comparison, the MSCI All Country World Index (ACWI), a global benchmark that includes all major developed and emerging markets, has a total of about 10.6% of its weighting in Energy and Materials. The US (S&P 500) has less (7.7%), while Canada has the most among the regions we track (30.5%).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

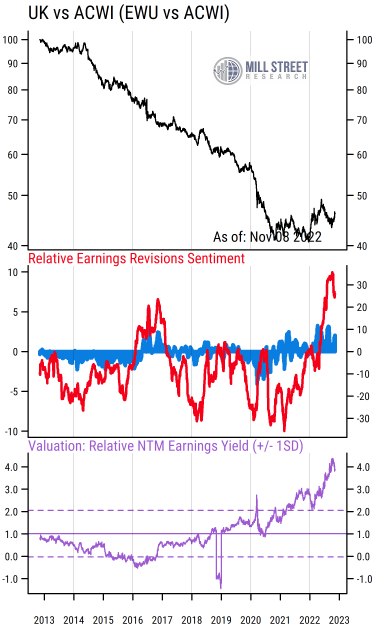

So while the UK has benefited from macro trends in commodities, the generally negative stock market returns and the rise in interest rates globally have pushed investors toward Value stocks. This should be a benefit for the UK, as it is much cheaper than the global average (the ACWI index) on a forward earnings yield basis. And while the UK has most often been cheaper than the global average, its current forward earnings yield (based on consensus earnings estimates for the next 12 months for stocks in the MSCI UK index) has been near 11% recently. This compares to an earnings yield of around 7% for the ACWI index, giving the UK a roughly 4% earnings yield premium. That wide an earnings yield difference for the UK is extreme by historical standards and has not been seen in many years (bottom section of chart below).

But what about earnings trends in the UK?

Sentiment among economists and investors toward the UK and the broader European economy is quite negative, as surging energy costs force drastic action while political turmoil raises risks of policy mistakes. In such conditions one might think that equity analysts would be especially inclined to cut their earnings forecasts for UK companies right now, but that is not the case.

For months now, our data has shown that revisions to earnings estimates for UK stocks have been much better than (or much less negative than) those of the global average (especially the US). This is also true for continental Europe (Eurozone), which we also favor. While the global average (ACWI index) shows revisions breadth (the net proportion of upward vs downward revisions to earnings forecasts by analysts, averaged across all stocks in the index and capitalization-weighted) at -16% (i.e., more analysts cutting than raising estimates), the figure for the UK is about +9%.

That 25% differential in revisions breadth between the UK and the global average is striking, and somewhat below the recent peak above 30%. As shown in the middle section of the chart below, over the last decade (or more), the UK has rarely had better-than-average revisions breadth, so such a wide positive difference is very unusual, with only the readings in 2016 being close. Before that, only the 2008 crisis period was comparable as the UK held up relatively better than other regions.

So when we look at our 3-panel indicator chart below, we see potentially supportive patterns in all three. Strong relative revisions (middle section) and favorable relative valuations (bottom section) join with the recent signs of a shift in the relative performance trend (top section).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The relative return for the US-listed ETF (EWU) vs that of the ACWI (ACWI) had been in a steady and severe downtrend from 2012 through late 2021, accelerating after the 2016 Brexit vote. This year has brought volatile but better relative returns in US dollar terms, and much more favorable relative returns in local currency terms. If the local currency relative returns stay positive, and the extreme strength of the US dollar versus the pound (and other currencies) eases, US-based investors could benefit more from UK exposure as well.

Thus the positive view on the UK is:

- UK earnings are (so far) holding up much better than the rest of the world

- UK stocks are very cheap in both absolute and relative terms

- Relative return momentum been improving (though volatile)

- The British pound may be cheap versus the US dollar

The counter arguments would be that the Value and commodity-oriented tailwinds that currently favor the UK will reverse soon, and that UK stocks and the pound deserve to be cheaper now as the country’s relative growth prospects are lower.

Our work tends to focus on the intermediate-term fundamental momentum and price trends, while using valuation as a risk measure. So our indicators remain supportive for the UK, and while shifts in the macro environment away from commodities and Value will happen eventually, it will likely take time.