Financial headlines have been captivated recently by explosive behavior in certain “meme stocks” that have been the subject of intense speculation by online retail traders as well as some hedge funds. This has been accompanied by a general trend of outperformance by smaller, money-losing, heavily-shorted, and volatile stocks (sometimes referred to as “junk stocks”, similar to risky high-yield “junk bonds”).

Other signs of “froth” include aggressive use of SPACs (Special Purpose Acquisition Company, or “blank check” company that raises money to acquire private companies), historically high trading volumes and activity in short-term call options, and growing margin debt.

This has raised broader questions about why “junk stocks” seem to be rallying much more than “quality stocks” and whether this is historically unusual.

The short answer is: no, this is not historically unusual under these circumstances. The specifics vary, but similar patterns have been seen in the past when markets are recovering from a sharp decline and policy support is very aggressive.

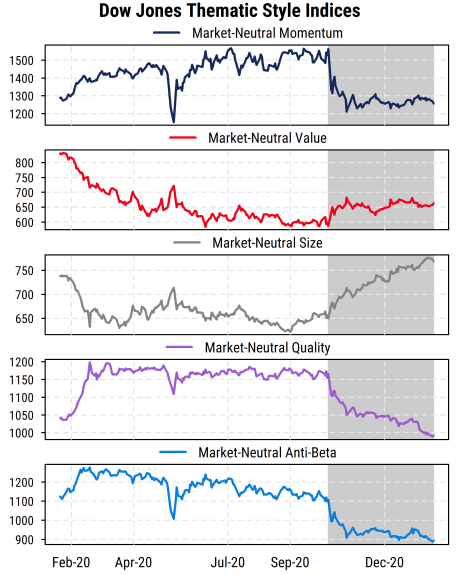

The first chart below plots the recent (past year) returns of the Dow Jones Thematic Market-Neutral Style indices. These are hypothetical long-short indices (i.e., assuming equal dollars invested in offsetting long and short portfolios) based on widely-used factors, using the 1000 largest US stocks, and constructed sector-neutral.

The key points are:

- Quality and Anti-Beta (low beta) are highly correlated, since quality stocks (defined by Dow Jones as those with high Return on Equity and low Debt/Equity ratios) also tend to be lower beta. Size (small-caps) is often negatively correlated with Quality and Anti-Beta (since small-caps are generally lower quality and higher beta). Risk is the key theme connecting these factors.

- November 6th (where shaded area begins) is when Pfizer announced its first COVID-19 vaccine results. This marked the point at which the recent themes really began: outperformance by low-quality, high-beta, small-cap stocks. This initially hurt the price momentum factor since those had not been the leadership areas previously.

- The Value factor had a bounce in November, but since then has shown no net performance. Thus it is not Value that has been rewarded, but risk, in the period since November 6th.

- It is also not coincidental that early November was when the US election occurred, and the results (fully decided in January) increased the perceived odds of additional aggressive fiscal stimulus. Such stimulus tends to benefit smaller, weaker (riskier) companies that had been hit hardest by COVID-19.

- Thus riskier companies have had recent tailwinds from both COVID-19 developments and greater fiscal support.

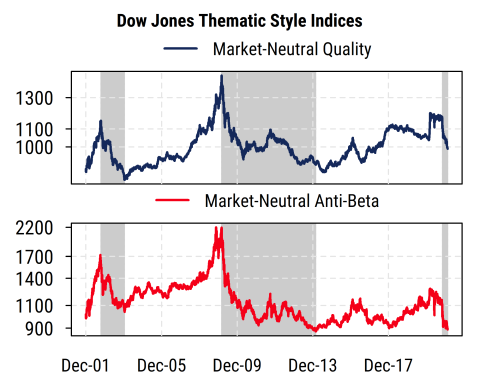

The long-term chart below shows the Quality and Anti-Beta factors since the data begin in 2001. We can see the correlation is clear over the longer-term, including the most recent few months.

The key point here is that in each of the previous periods of post-recessionary aggressive stimulus (2002-03, 2009-13), higher risk (lower quality) stocks were rewarded as investors sought the biggest “bang for the buck” from the stimulus and recovery. Weaker, riskier stocks tend to get the most benefit from policy support, while stable, higher quality companies do not need it and get relatively less benefit. Thus the current conditions are not unusual, and fully consistent with a risk-on environment, in line with our other indicators that remain bullish for equities on a tactical basis.