The Tech-related space remains the focus in the US, and we have recently noted a growing divergence between the Technology sector and its cousin Communication Services in the S&P 500: Tech remains strong while Communication Services is weakening. We thus see growing selectivity by analysts and investors in the Tech/AI space and our sector allocations favor Technology over Communication Services.

For some time now, the Technology and Communication Services sectors have, at least within the cap-weighted S&P 500 universe, been moving together as a broader “Tech-related” area that captures both hardware and software makers (NVIDIA, Microsoft, Apple, etc.) and internet and media companies (Alphabet, Meta, etc.). The biggest names in those sectors are dominant in the AI space and are thus heavily interconnected.

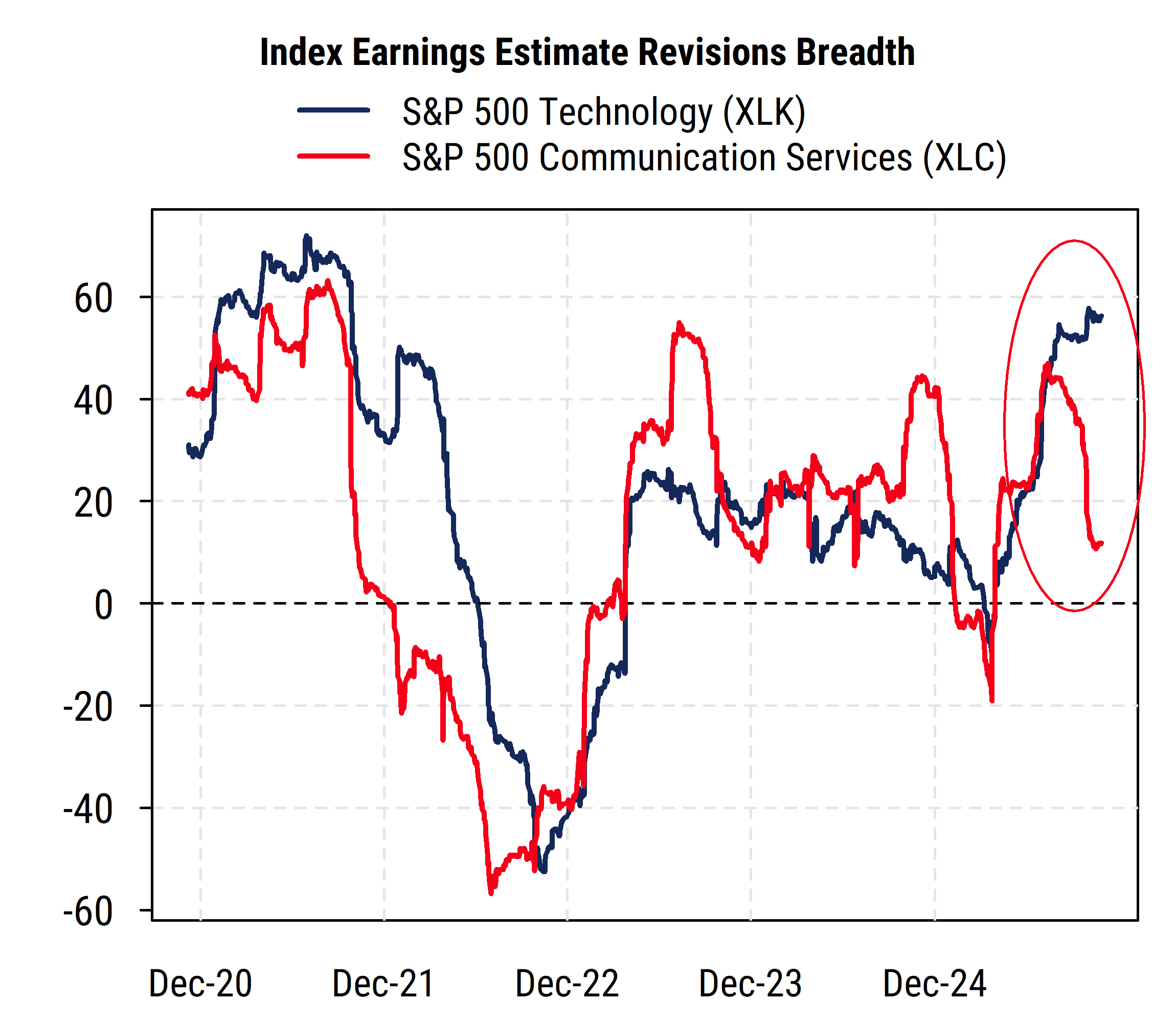

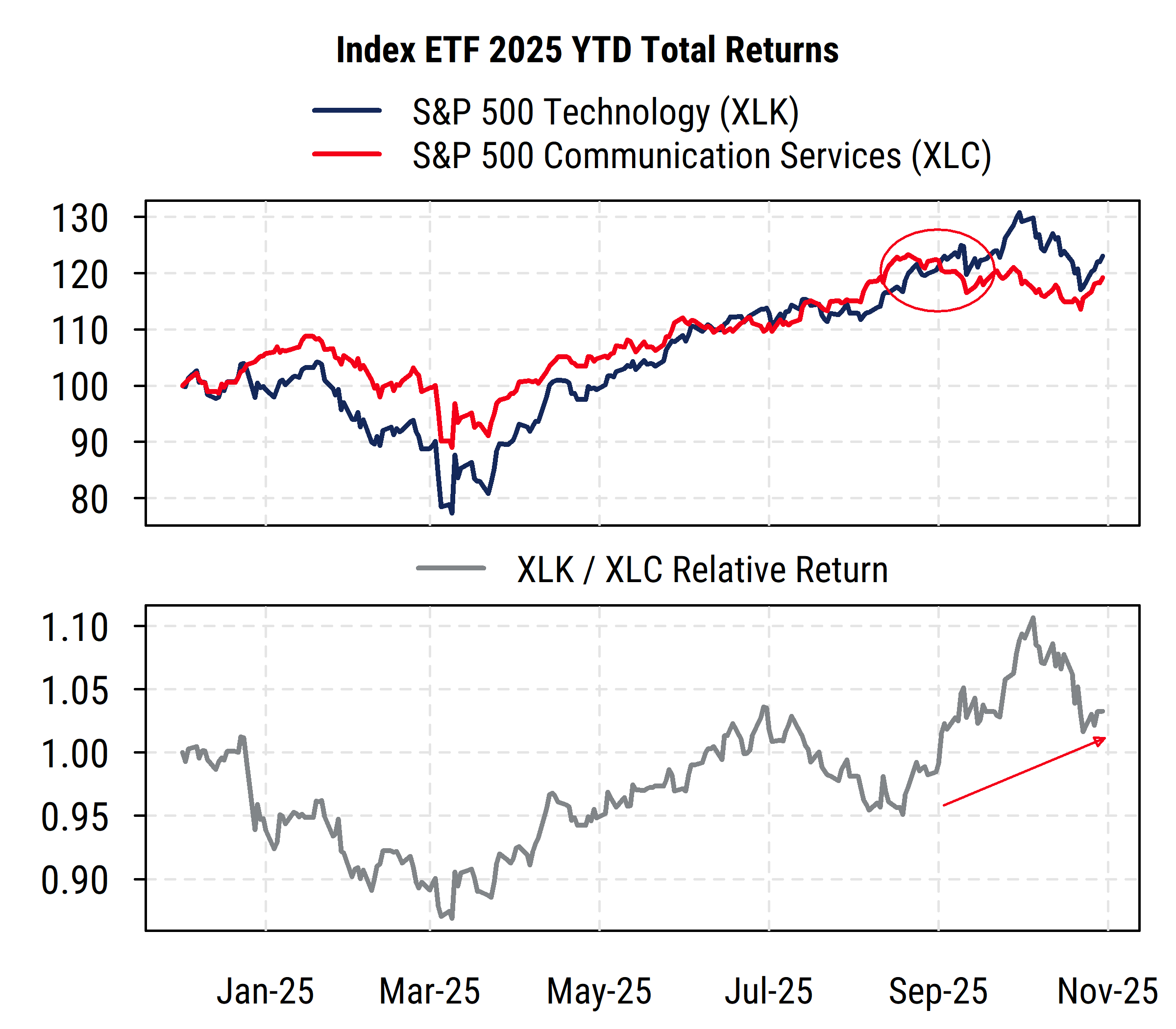

And for much of this year, the Technology and Communication Services sectors have had similar patterns in both earnings estimate trends and relative returns.

Indeed, through mid-September, the two widely-watched S&P 500 sector ETFs (tickers XLK and XLC) had nearly identical year-to-date returns and similarly strong revisions breadth amid lots of overlap in the AI space among the mega-caps (e.g. NVDA and MSFT in Tech and META and GOOGL in Comm. Svcs).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

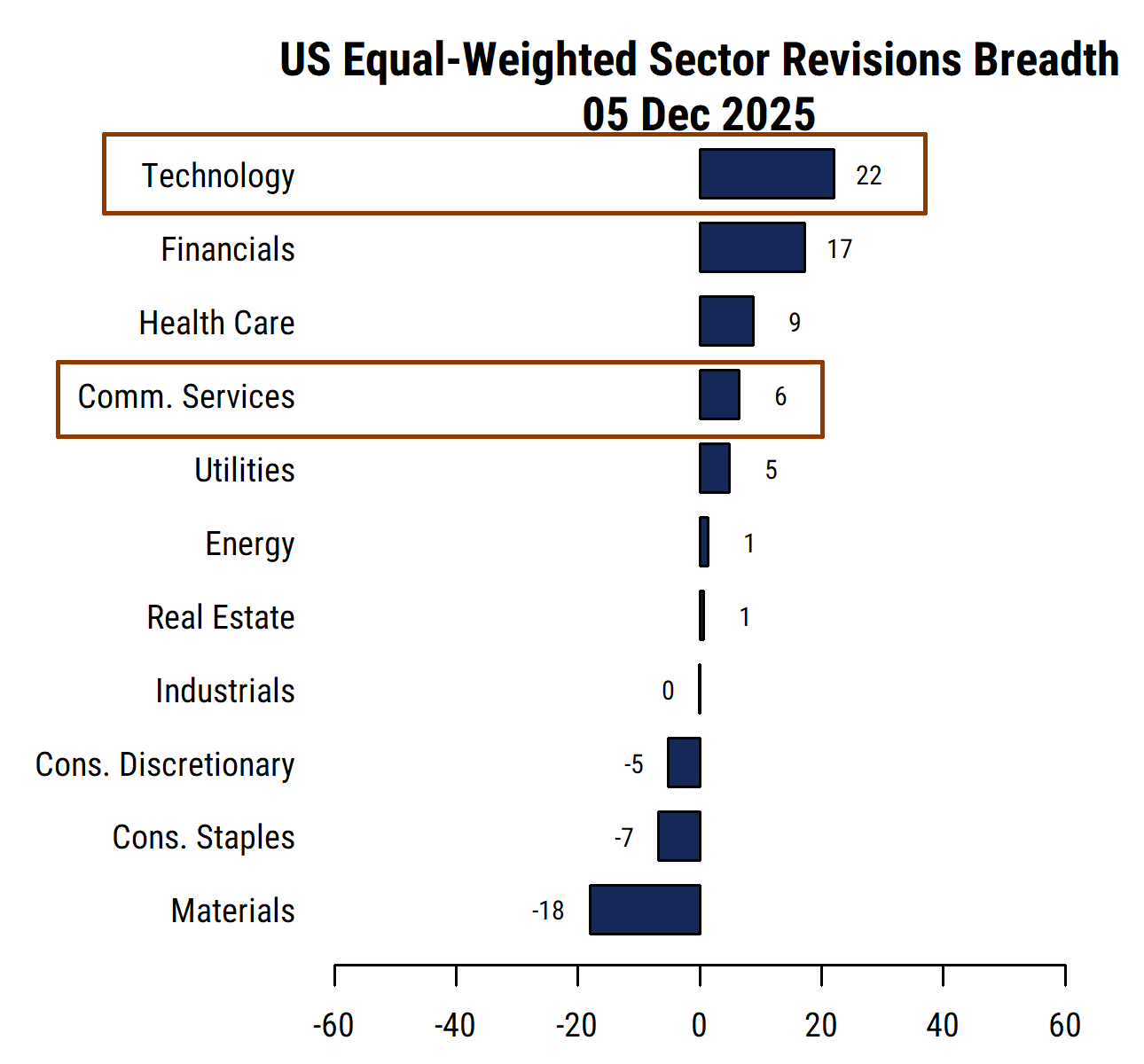

As a reminder, “revisions breadth” is a measure of the net proportion of equity analysts covering a stock who are raising their earnings per share (EPS) estimates for the next 12 months. That is, roughly, the number of analysts who have raised estimates minus the number who have lowered estimates as a percentage of the total. The figure can thus range from -100% if all analysts are cutting EPS forecasts to +100% if all analysts are raising estimates, with 0% indicating a 50/50 split. Our work has long indicated that stocks and industries with high proportions of analysts raising estimates tend to outperform those with low (negative) breadth over time.

More recently, however, and particularly after Q3 earnings reports, the revisions metrics for the S&P 500 Communication Services sector have declined even while those for Technology have held up at very high levels or even improved.

So we have recently downgraded our sector allocation recommendations for Communication Services, while leaving Technology at a strong overweight.

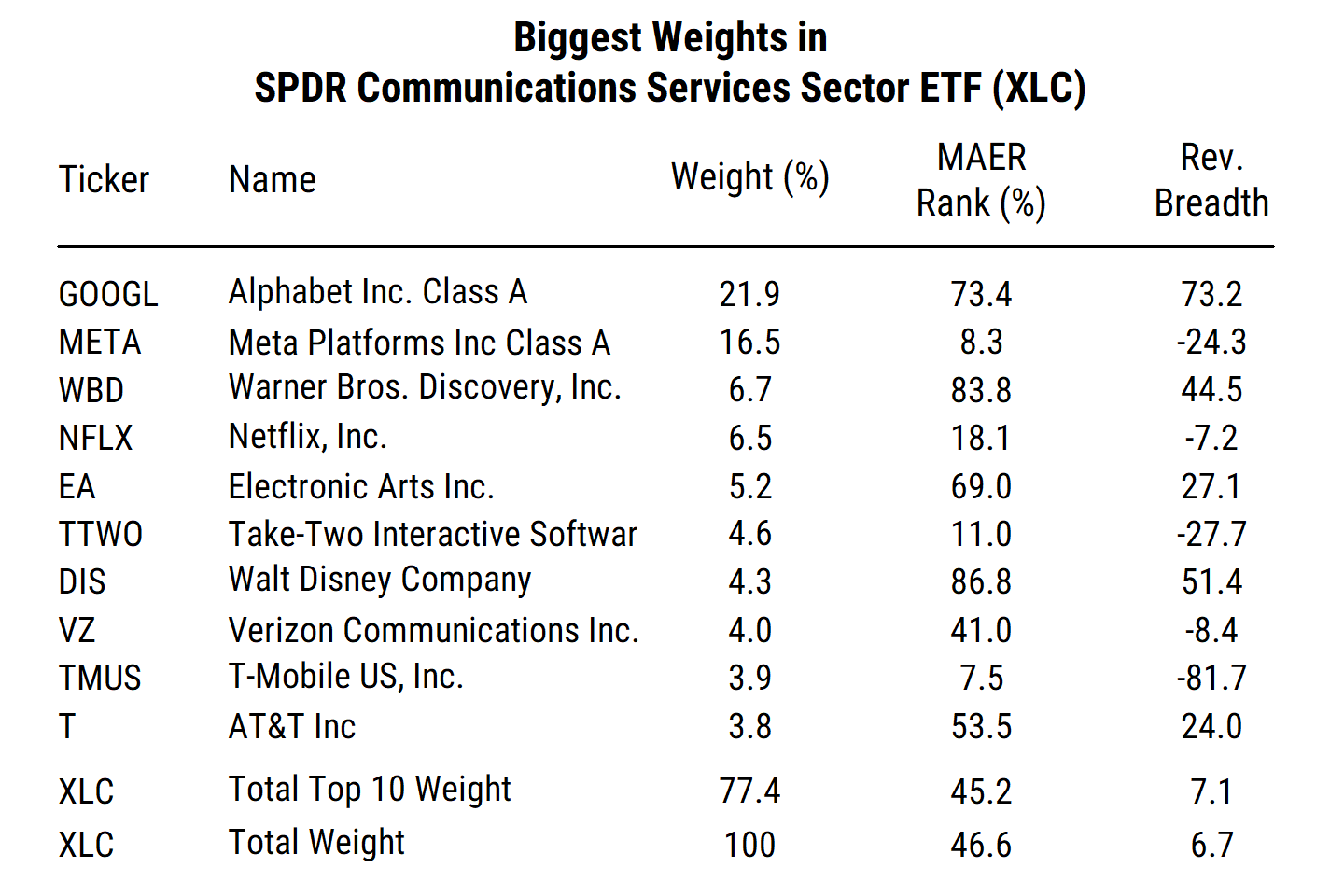

Looking into the big constituents in the sector, the main culprits of the recent downturn in Communication Services revisions have been Meta, Netflix, and T-Mobile. All reported earnings recently that were in some way disappointing to analysts and investors, and our indicators have picked that up. Meta (16% of the sector by weight) in particular is notable as a company that is spending enormous sums on AI development (data centers, etc.), but is having trouble convincing investors the return on investment will be sufficient to justify the huge capital expenditures.

Along with signs of more debt-based funding being used in AI capex, concerns have grown for some companies. Alphabet (Google) seems to be holding up best so far among the mega-caps in the sector, and has gotten a big boost lately from improvements in its own AI product (Gemini) that is garnering more attention than OpenAI’s ChatGPT.

Looking further into the biggest constituents of the two sectors highlights the divergence (tables below). In Communication Services, we see five of the 10 largest names having outright negative revisions breadth and an average in the top 10 of only +7%. And one of the more positive readings among those is for Warner Bros. Discovery, which is now the subject of a buyout by Netflix (which has mildly negative current revisions readings), or possibly Paramount, so it will be a “deal stock” unrelated to its current earnings until a deal closes (assuming it does) and it goes away. Alphabet is thus the main company now holding the sector’s cap-weighted revisions up, along with Disney, suggesting quite narrow leadership, while mega-cap Meta has seen revisions turn negative after Q3 earnings. The big telecom companies of Verizon and AT&T also both have negative estimate revisions to varying degrees.

Source: Mill Street Research, Factset

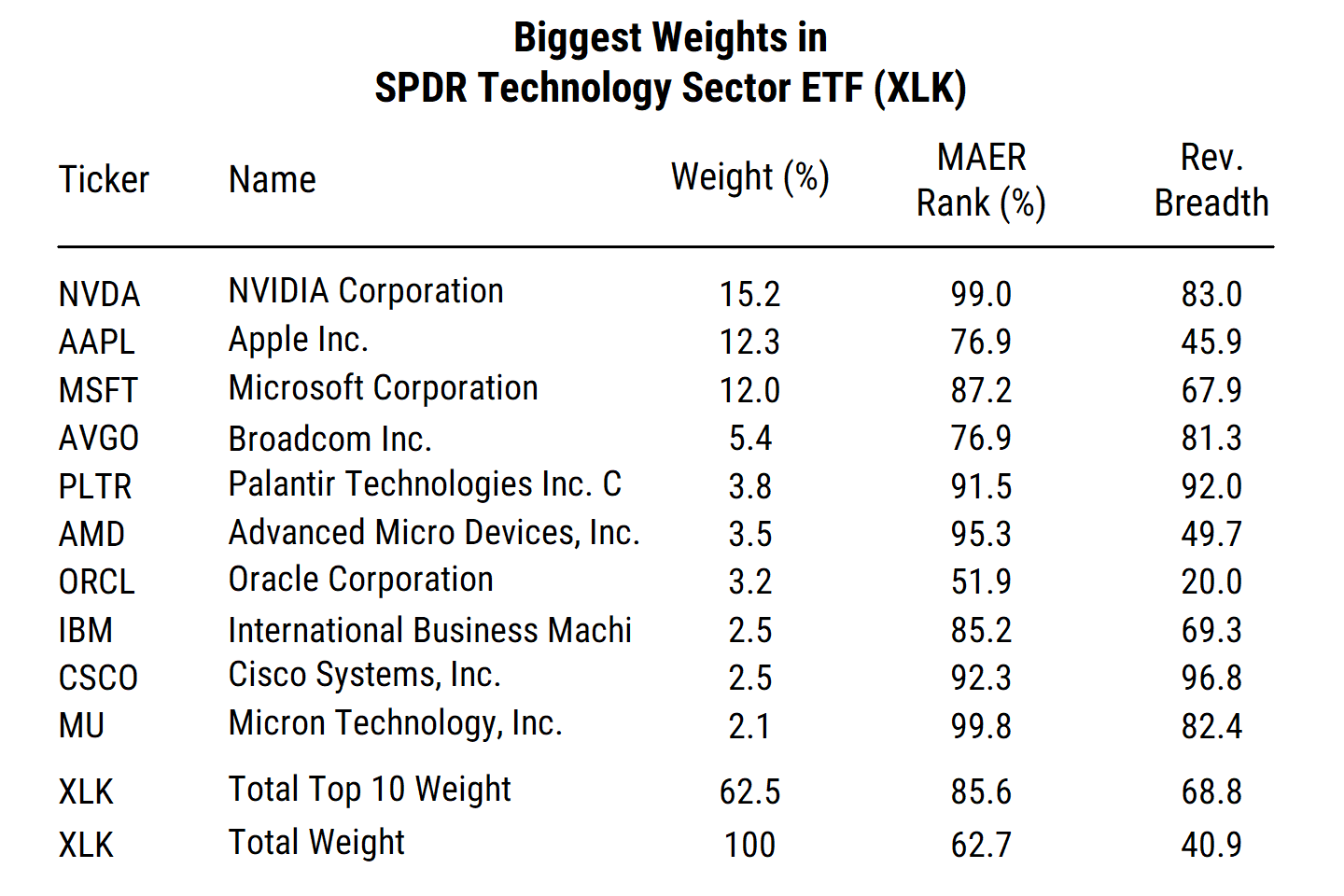

Meanwhile, in the Tech sector (XLK), we see that all 10 of the largest stocks in the sector have solidly positive revisions breadth, including the “big three” of NVIDIA, Apple, and Microsoft. The average MAER ranking for the top 10 is 86%, an extremely high reading, with five of the 10 being in the top decile of the S&P 500 universe. The MAER ranking is our long-standing proprietary multi-factor stock selection tool based on earnings estimate revisions, price action (momentum and mean reversion), and valuation. We can rank all stocks in the S&P 500 (or any other list of stocks) on a percentile basis (0 – 100%), and find that high-ranked stocks tend to outperform low-ranked stocks over the next 1-6 months (and often longer). More information about MAER is available here.

In addition to the indicators shown here based on the cap-weighted index ETF constituents, we also look at the broader universe of Technology stocks (about 300 among our 2500-stock all-cap US universe) and find that Tech revisions readings also remain strongly positive (best of the 11 US sectors), meaning it is not just the mega-cap “Mag 7” or AI stocks driving things. The readings for the broader Communication Services are also lower (though still net positive) than for the all-cap Tech sector.

Source: Mill Street Research, Factset

The key result is that analysts and investors are becoming more selective in their earnings outlooks and stock picking within the popular Tech-related (and particularly AI-related) space, and that increased selectivity can be seen in our data for the S&P 500 Technology and Communications Services sectors.

After months (from mid-April to mid-October) of a market that seemed to want to “buy everything risky” and chased anything tied to AI, the backdrop has shifted in the last month or two. We have been guiding clients to favor Tech over Communications Services recently, and arguing for greater selectivity and focus on companies with strong earnings outlooks in general.

Sam Burns, CFA

Chief Strategist