The turmoil in the Middle East and the rise in energy commodity prices continues, but stock prices have mostly decided they don’t care that much. Energy prices are not a major driver of US corporate earnings, and the inflation seems not to worry the Fed enough to change policy.

Headlines are all about Iran and oil, but investors have moved on already

Investors continue to watch headlines and events in the Middle East closely for indications of whether the conflict there is going to get better or worse, and when commodities will again be able to move through the crucial Strait of Hormuz again. Prices for crude oil and all of its derivatives (gasoline, diesel/heating oil, jet fuel, components of plastics, etc.) have risen sharply from their levels before the war with and around Iran started at the end of February, though the magnitude of the rise depends on which specific price is used.

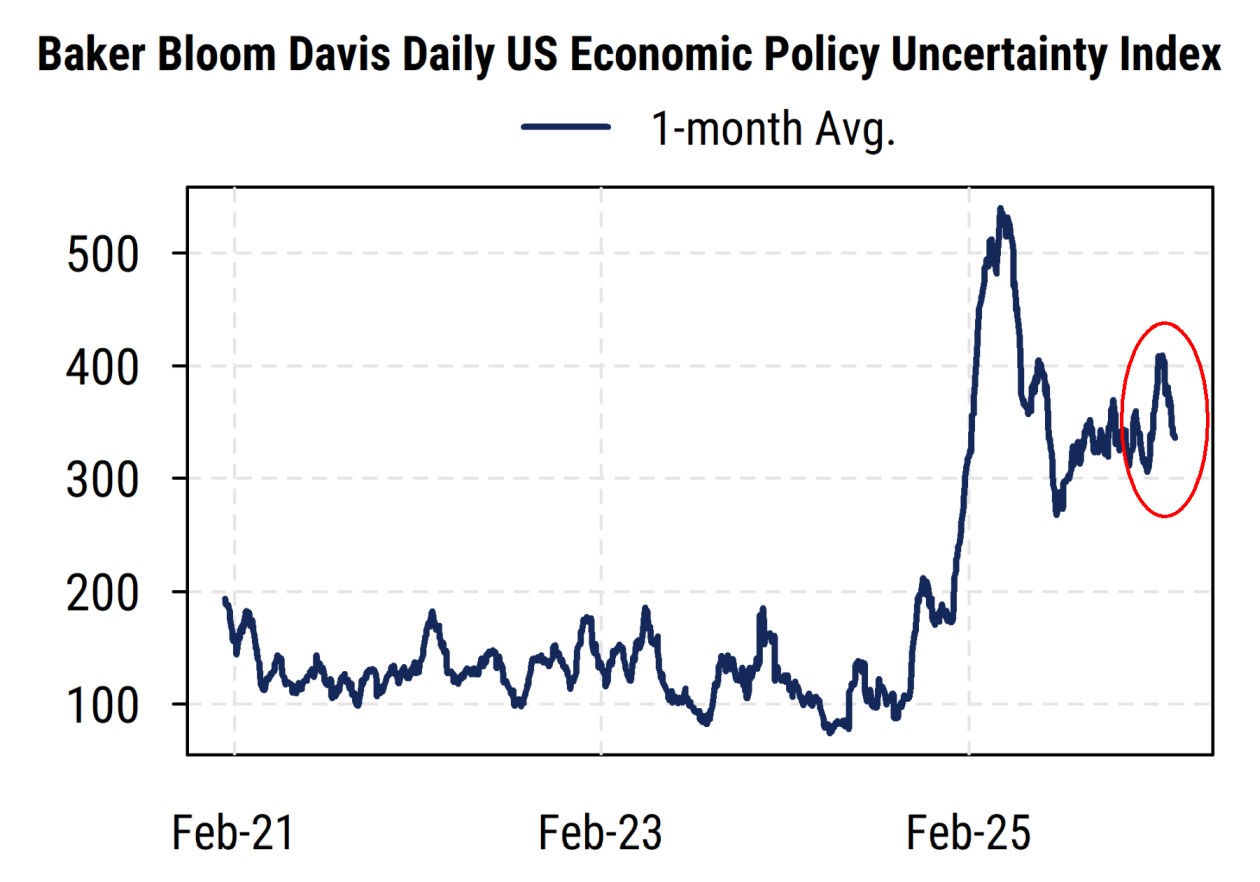

Initially, stock prices responded to the moves in oil prices fairly closely: higher oil pushed stock prices lower, and vice versa. The headlines surrounding the war changed day to day and even hour to hour, producing a surge in uncertainty about how things would play out. Higher uncertainty tends to reduce investor risk appetite and thus equity valuations (all else equal), and this is exactly what we saw during the first half of March.

Source: Mill Street Research, Bloomberg, Factset

But more recently, the stock market has become less sensitive to oil prices or Middle East developments. Even though the crucial Strait of Hormuz remains basically closed, the S&P 500 has returned to its highs, and ex-US stocks have also rallied.

Source: Mill Street Research, Factset

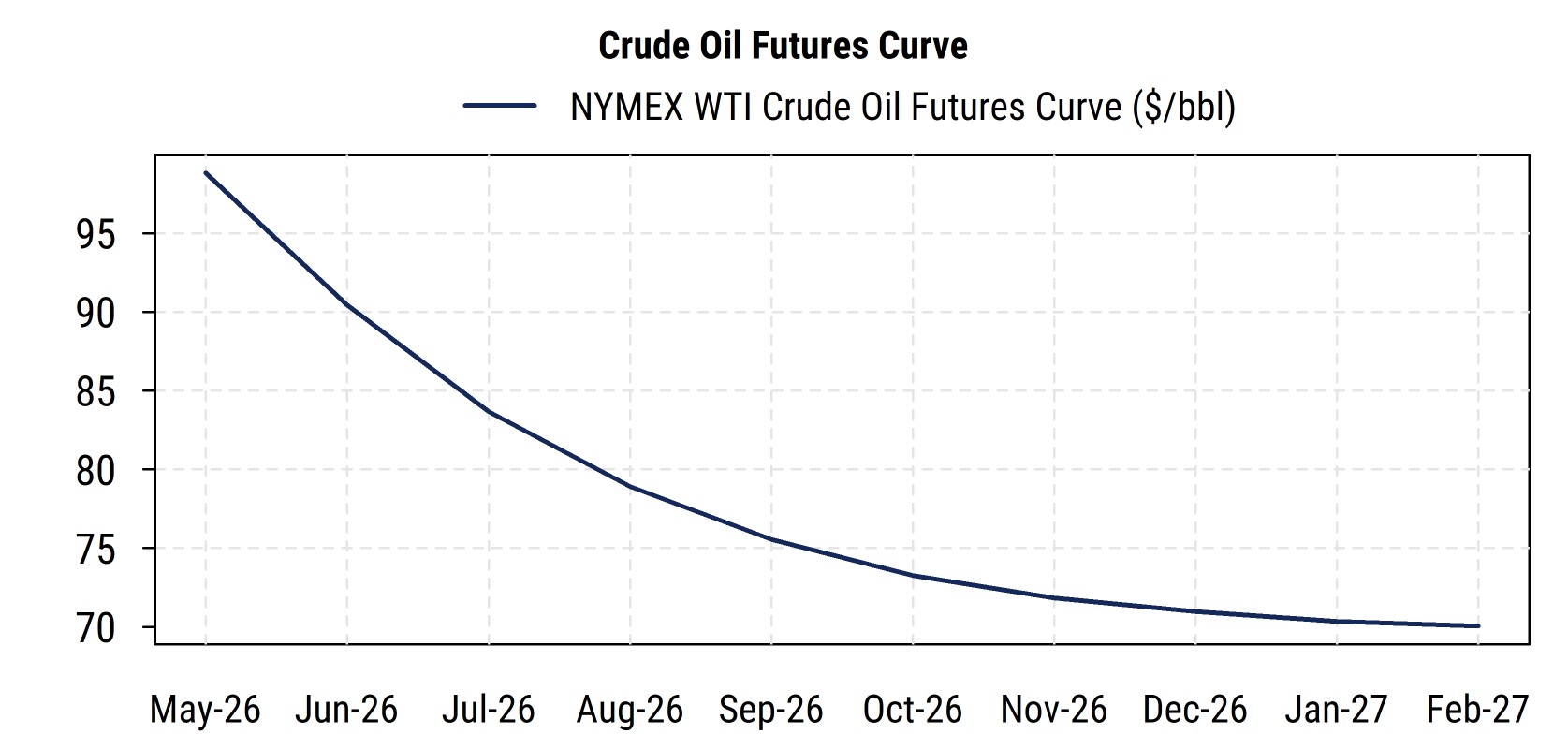

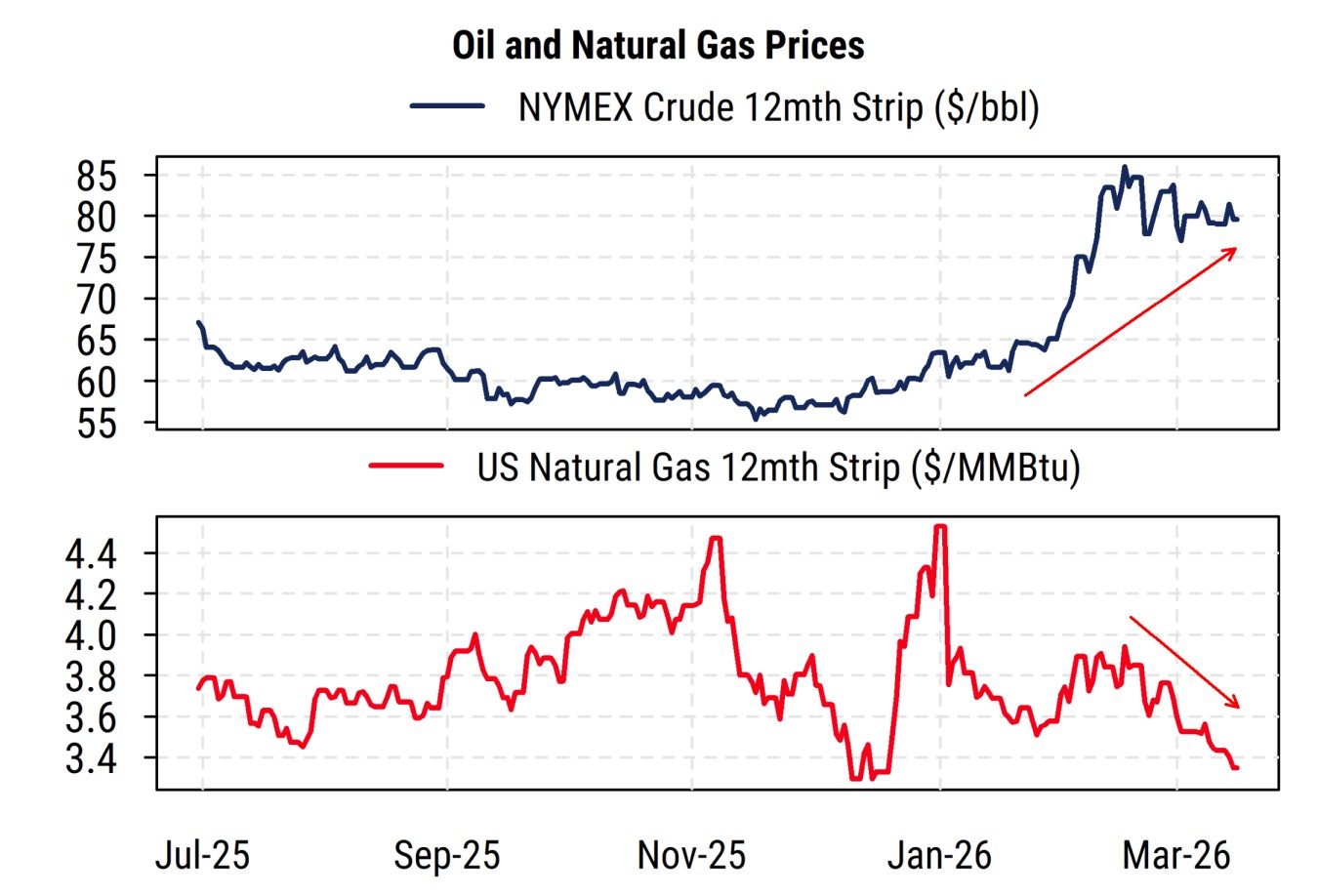

Partly this simply reflects the market’s assumption that the war will end fairly soon and trade in the region will resume within a few months at most. Crude oil futures continue to show a dramatic difference between prices for near-term delivery and longer-term contracts (chart below). Pricing for December shows prices of around $70/bbl for WTI crude oil, compared to the price of $62 at the end of January. While this is a notable increase, it is much less than the current prices of $90-100/bbl. The longer-term contracts show prices expected to continue gradually declining over the next few years.

Source: Mill Street Research, Bloomberg

However, the other big reason the stock market seems less worried about oil prices is that even near current levels, it simply won’t matter much for overall US corporate earnings or even consumer spending.

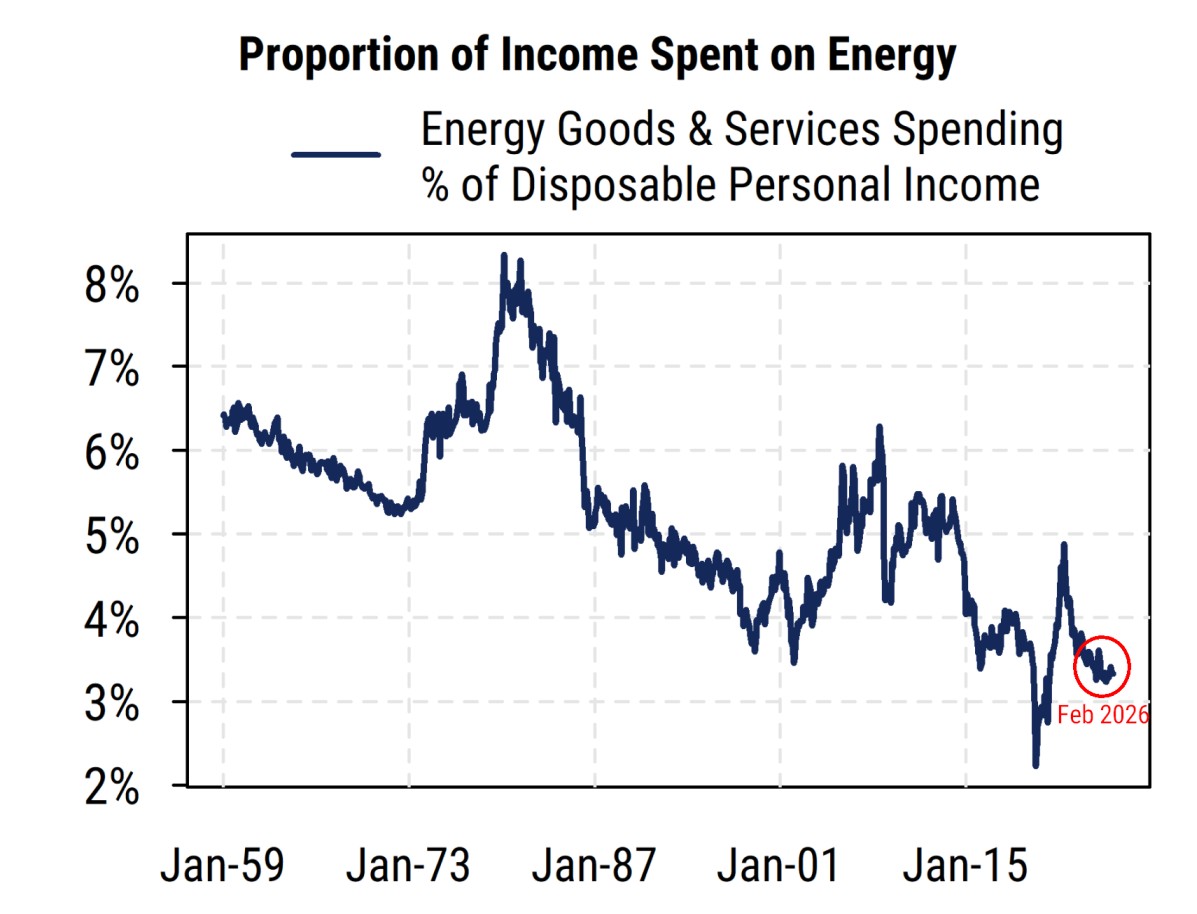

Starting with the economy, the data from the BEA show that as of February (before the war started), consumer spending on “energy goods and services” was only 3.3% of total disposable personal income. This includes both auto fuels (gasoline and diesel) as well as household electricity and natural gas utility spending. As shown in the chart below, the recent reading is near the lowest on record since 1959 outside of the COVID-driven spike in 2020.

Source: Mill Street Research, Factset, BEA

So even a substantial rise in oil prices might only push that proportion up to where it was for much of the 2000-2014 period. And the US (unlike Europe or Asia) has thus far seen no increase in natural gas prices due to high domestic production. The US economy is both more efficient in its use of crude oil and its derivatives than at any time in the past, and more insulated due to domestic production of both oil and gas.

Source: Mill Street Research, Bloomberg

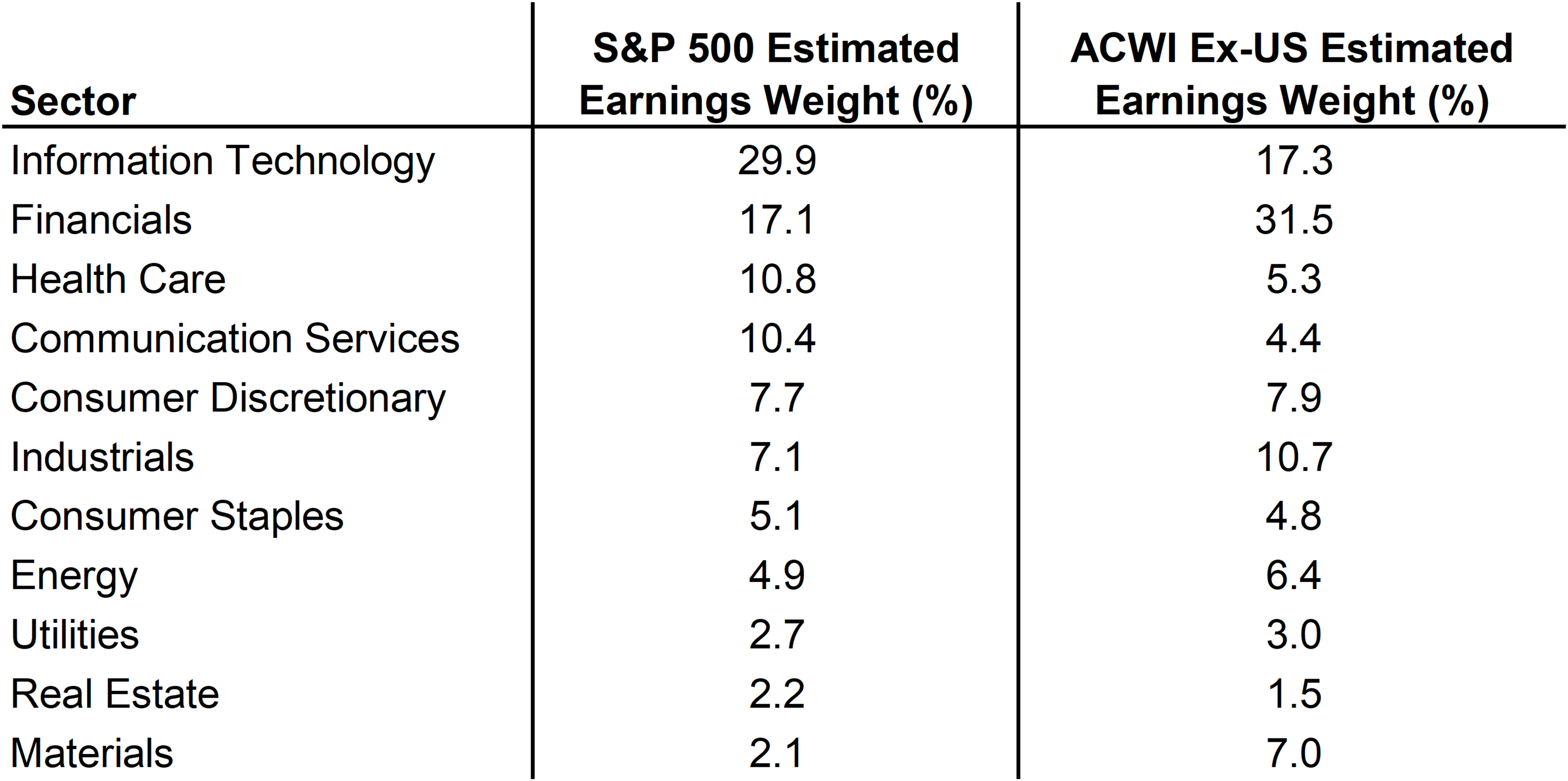

The other reason the stock market specifically does not care much about the rise in oil prices is that most of the biggest companies in the market are not very sensitive to energy or commodity prices. As shown in the table below, the great majority of the estimated 2026 earnings of the S&P 500 come from sectors like Technology/Communication Services, Financials, and Health Care that have little direct exposure to energy costs. The sectors that tend to be hurt most by higher energy costs are the consumer sectors, along with parts of the Materials sector, and some Industrials like airlines and transportation/shipping companies. But those sectors/industries comprise a relatively small part of the S&P 500 compared to Technology, Communication Services, Financials, and Health Care. The same is broadly true for ex-US stock indices like the MSCI ACWI Ex-US index, though with more Financials and less Tech outside the US.

Source: Mill Street Research, Factset

This particularly true when considering that the Consumer Discretionary sector has more than half of its weight in just two stocks, Amazon and Tesla, both of which are treated more like Tech stocks than traditional retailers or car companies due to their other businesses. So the net weight of companies in the S&P 500 that are likely to be significantly negatively affected by oil/fuel costs directly is fairly low.

On the other side, the Energy sector that is the obvious beneficiary (at least in the shorter-term) is only about 3.6% of the index by market cap and 4.9% of the earnings. The big “winner sector” is thus fairly small, but similar to Consumer Staples (one of the oil price “loser” sectors) which is about 5% of the index’s earnings.

The bottom line is that NVIDIA by itself is much bigger than the entire S&P 500 Energy sector, and Technology, Financials and Communication Services make up well over 50% of the earnings for the index, with Health Care another 11%. So what happens with technology spending (AI) and Financials is much more important than movements in the price of oil, unless oil were to go far higher.

Note also that oil prices, using the rolling 12-month crude oil futures “strip” (average of the next 12 monthly futures prices to get a more stable reading), are still not as high as they were in 2022 when Russia invaded Ukraine. That occurred during a period when inflation was already rising and the economy was slowing (due to removal of COVID stimulus and rapid monetary policy tightening by the Fed), unlike today.

Inflation is only a problem for stocks if the Fed tightens, and it looks like it will not

The other key factor affecting the response by stock and bond investors to the moves in oil is the effect on inflation and thus monetary policy. It is worth remembering that inflation is not always a bad thing for stocks, as corporate earnings will tend to rise in line with inflation, so equity investors are partly hedged against inflation (unlike bond investors). So the main reason inflation is “bad” for stock investors is that it often causes interest rates to rise in response. A higher “discount rate” on future earnings means they are worth less than they would be otherwise, meaning valuations (P/E ratios) tend to fall.

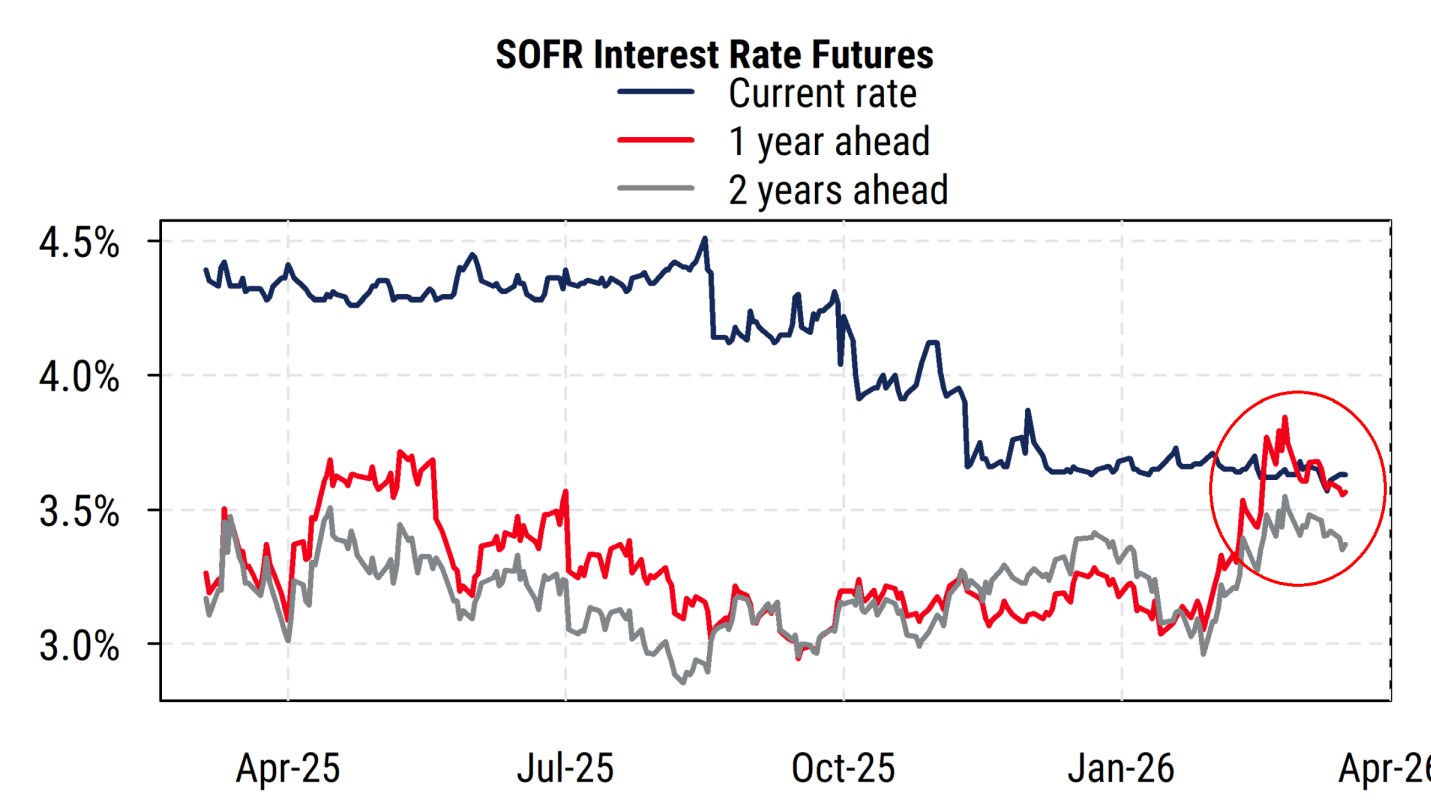

But what happens if inflation rises but interest rates do not go up? That’s what seems to be happening so far. Fed officials have indicated that they are inclined to “look through” the current jump in headline inflation caused by energy prices, on the assumption that it will be relatively short-lived and that the non-energy components of inflation are likely to be contained. The chart below shows the one-year and two-year-ahead futures contracts tied to the SOFR (Secured Overnight Financing Rate) benchmark, which replaced LIBOR as the key short-term interest rate proxy, and moves closely with but trades more actively than fed funds futures.

Source: Mill Street Research, Bloomberg

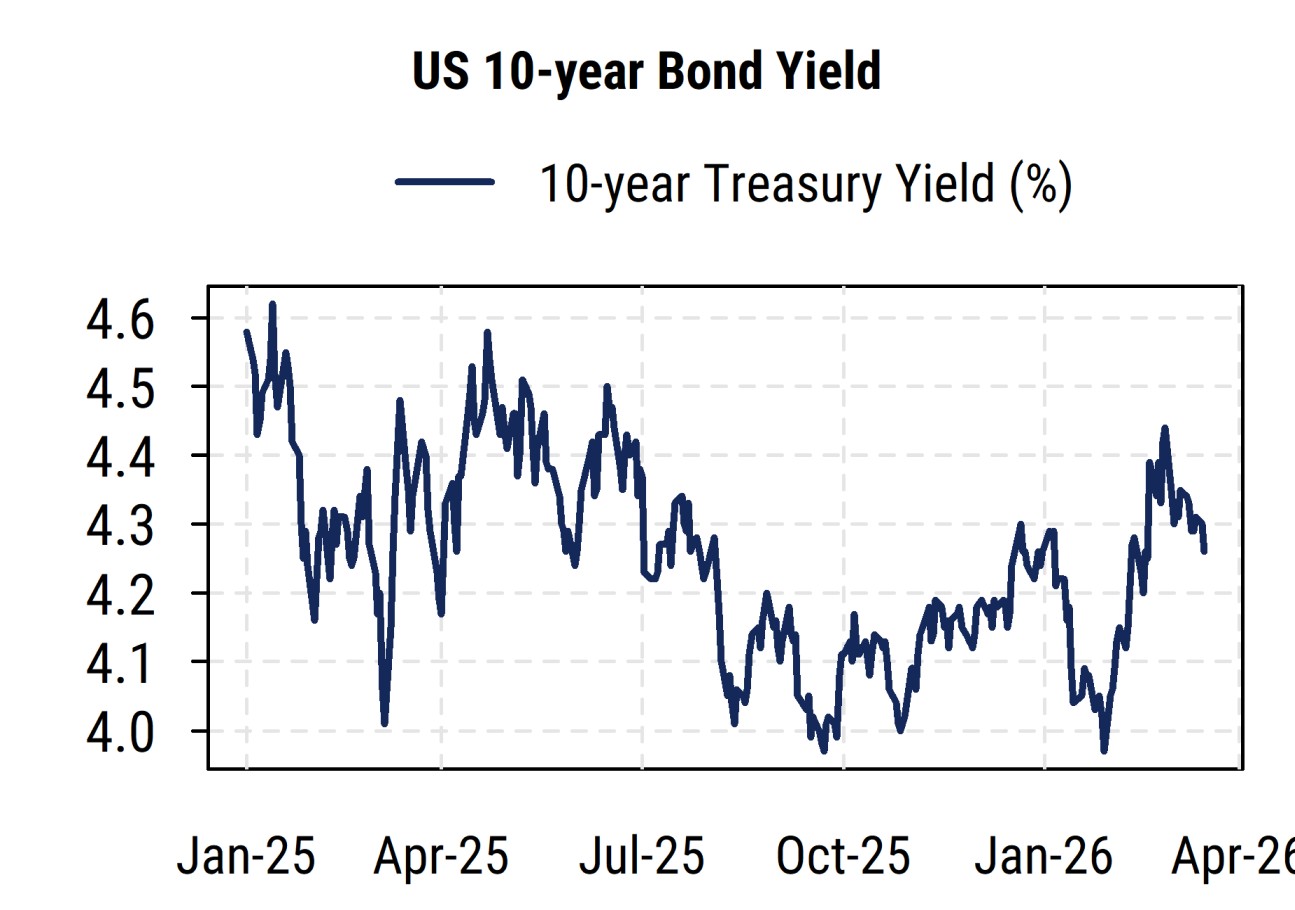

Bond yields have risen since the war started, but not to an extreme degree, and have been coming back down somewhat in the last week or two. The 10-year Treasury yield is still in the same broad range it has been in over the last year, and currently about where it was in late January. Futures markets indicate that investors have removed any potential rate cuts from their view, but are not pricing in any rate hikes either: the Fed is expected to stay firmly on the sidelines for the next few months at least. This is probably the best policy right now, given the high level of uncertainty and divergent influences on inflation (underlying real growth is ok but may be slowing), and the fact that rates are currently viewed as near “neutral” (neither very restrictive nor very accommodative).

Source: Mill Street Research, Factset

Earnings are rising and rates are stable: why worry?

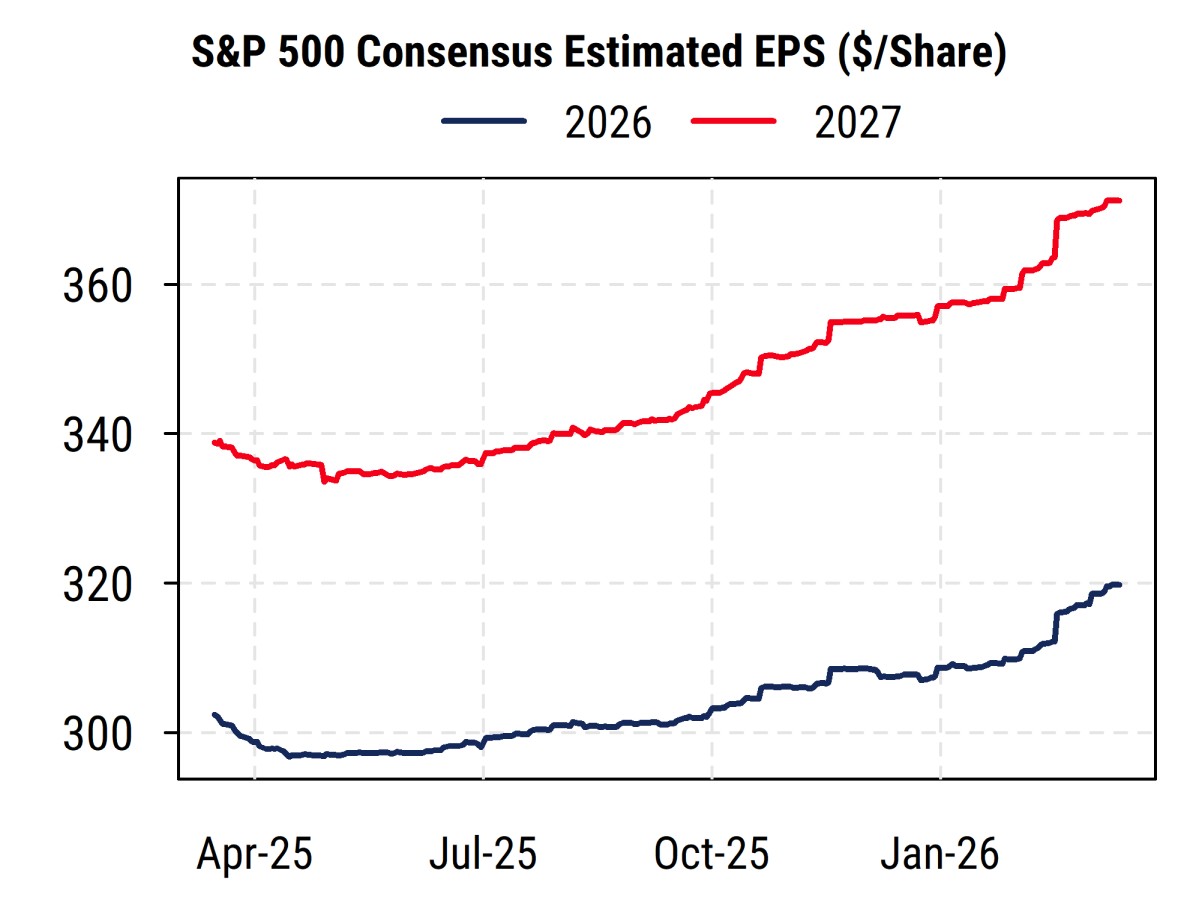

The chart below shows the evolution of aggregate index earnings estimates for the S&P 500 for this year and next. Earnings reports for Q1 are getting underway now, which could bring some shifts in the outlook, but overall expectations are that Q1 earnings will be up 13% or more from a year ago, marking the sixth consecutive quarter of double-digit earnings growth.

Source: Mill Street Research, Factset

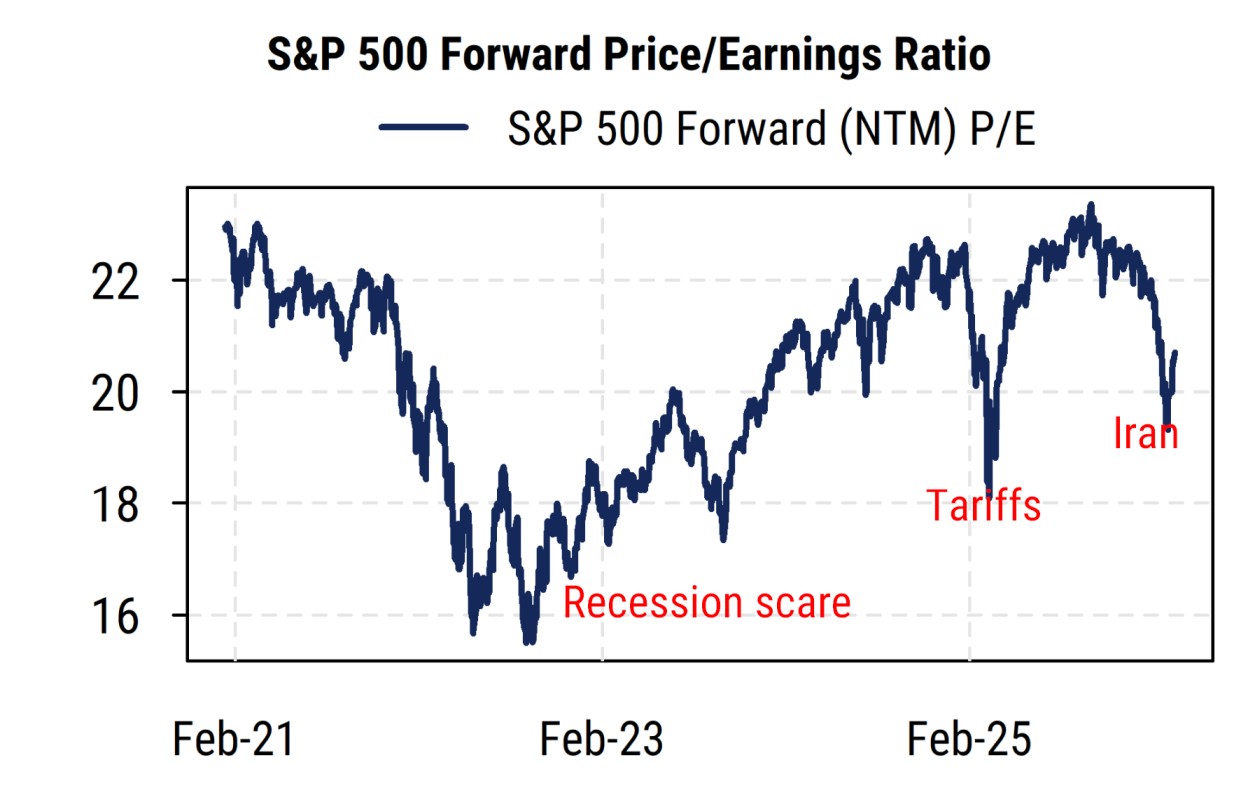

If earnings are still rising at a 10%+ rate and interest rates are stable, the two main drivers of stock prices seem to be supportive. The reason stock prices have struggled this year is that valuations (on forward 12-month EPS estimates) have contracted, as noted above. This reflects some combination of 1) worries about oil and the broader conflict in the Middle East, and 2) concerns about the market’s dependence on AI and how it will evolve.

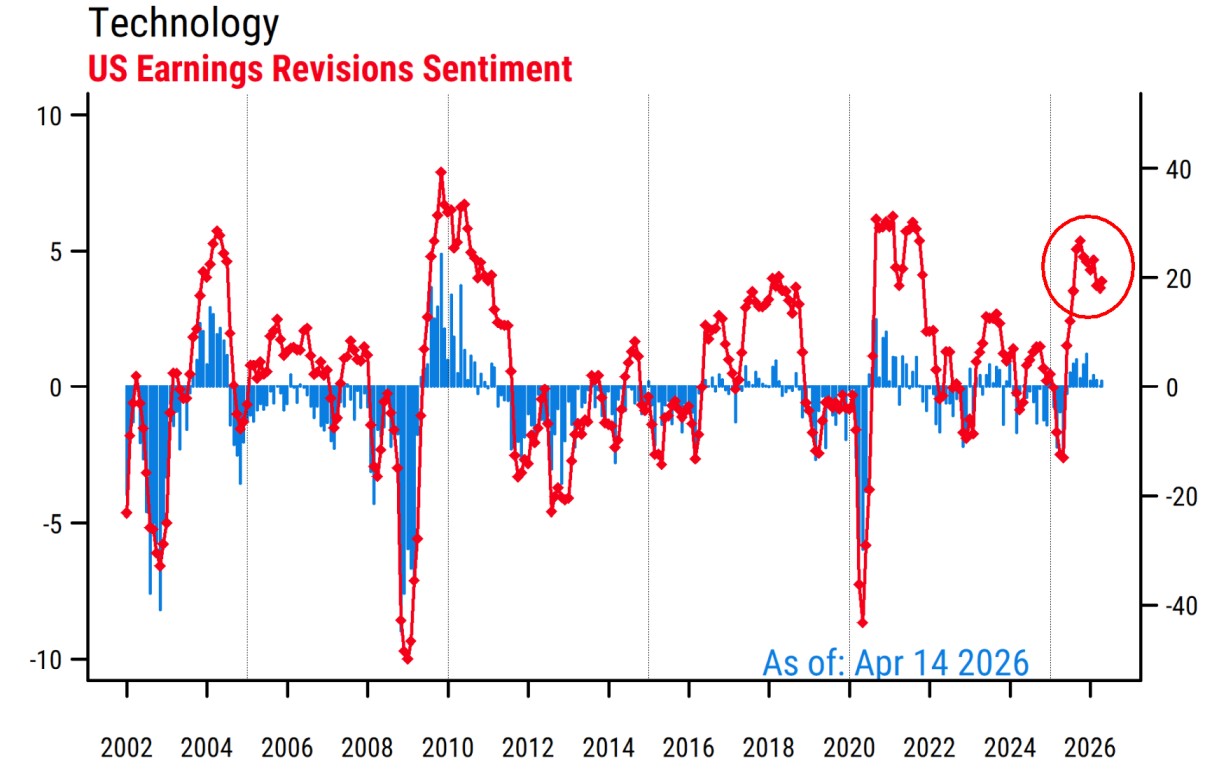

News about AI has caused widespread declines in the software industry, while producing surging earnings for makers of hardware, including not just chips but memory, storage, etc. Any news about plans for capital spending by the “hyperscalers”, which run into hundreds of billions of dollars a year now, are more of a market mover than commodity prices. So far, earnings estimates for the Technology sector, especially in hardware, have continued to rise – whatever damage to software/services business models AI might do is far outweighed (at least in the next year or two) by increased spending by builders and buyers of AI tools. The chart below shows our measure of earnings estimate revisions in the US Technology sector (all-cap, all stocks equally-weighted), with the red line indicating the net proportion of analysts raising vs lowering next-12-month EPS estimates and the blue bars indicating the 30-day percent change in estimates on average in the sector. Readings above zero indicate positive EPS estimate revisions, and recent readings have remained strongly positive. The picture looks similar (and even stronger) when calculated on a cap-weighted basis.

Source: Mill Street Research, Factset

Blessing and curse: Tech and Financials are most of what matters, not oil

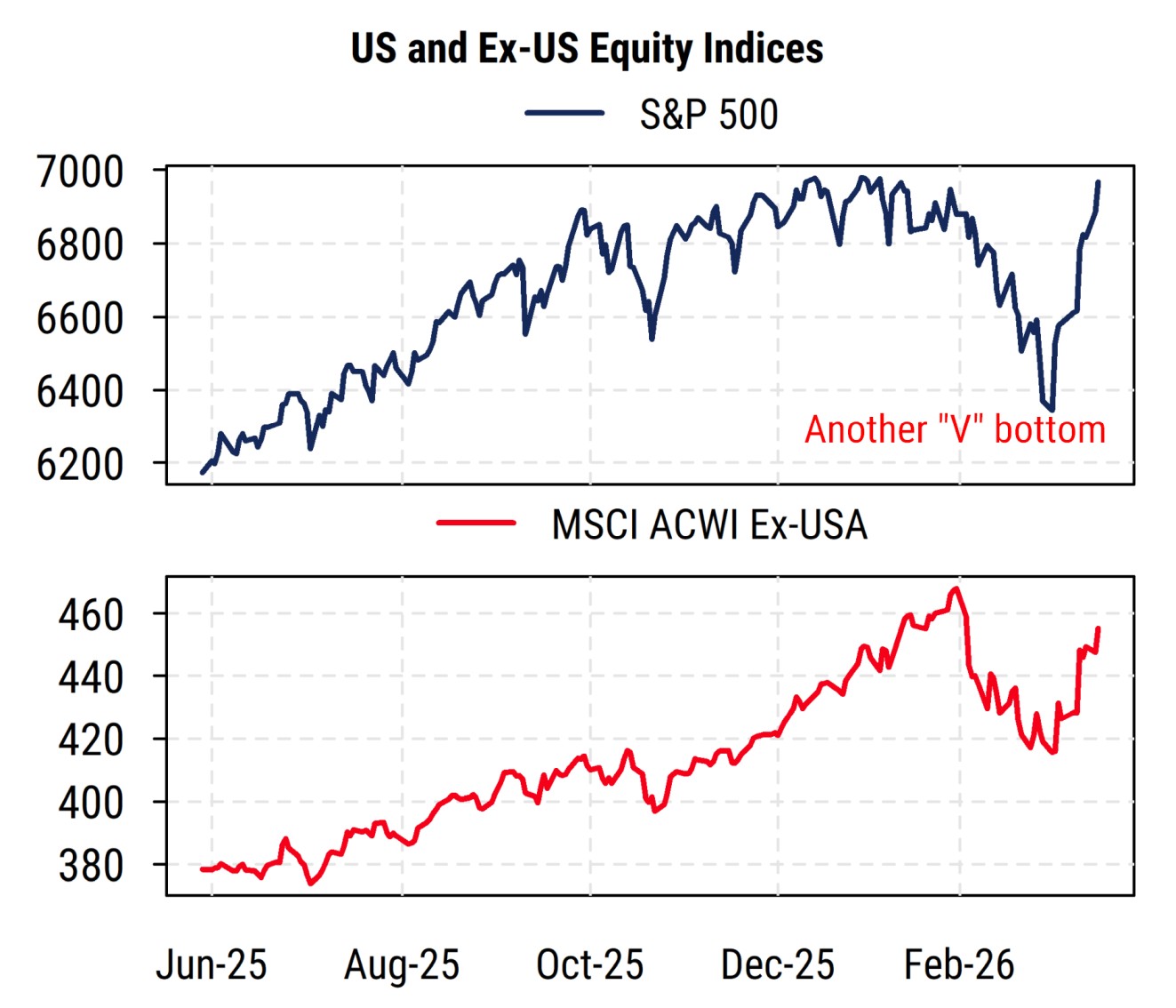

The stock market is currently benefiting from the fact that the majority of US corporate profits are not closely tied to energy or commodity prices generally. It also, however, still has the risk of being fairly concentrated: if a few big Tech companies were to signal weakness in their business (particularly if tied to AI), the market would likely feel the impact more sharply. Monetary policy is stable and not restrictive, and fiscal policy remains relatively loose. Risk appetite is the main swing factor, which has been dampened by geopolitical headlines and higher market volatility, but seems to be recovering lately. First it was tariffs (where AI hardware was quickly exempted), now it is a pointless war with Iran (which so far does not affect Tech demand much): markets are showing more “V” bottoms and learning the “TACO trade” as Tech and Financials drive things more than fiscal or foreign policy.

Sam Burns, CFA

Chief Strategist