2 September 2021

In our regional allocation work, we have been underweight in Emerging Markets relative to developed markets since May, and remain so currently. A key reason for our continued underweight stance is that the relative fundamental momentum for emerging markets remains very weak compared to that of the broader global equity market.

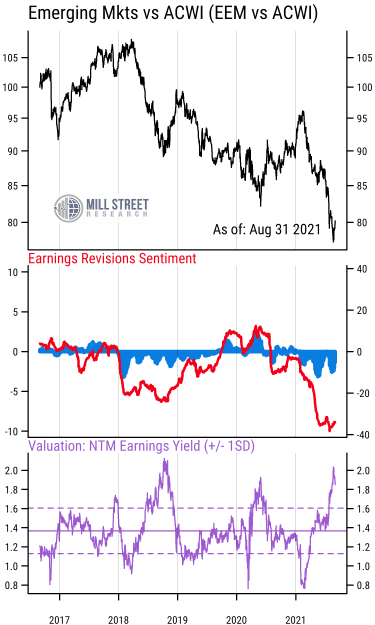

The chart below shows one of our popular composite indicator charts based on the relative performance of the widely-followed MSCI Emerging Markets ETF, ticker EEM, versus the broad global benchmark of the MSCI All-Country World Index (ACWI) ETF, represented by ticker ACWI.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The top section plots the relative price of EEM vs ACWI over the last five years, with the series indexed to 100 at the beginning of the chart. We can see clearly that EM has generally lagged the global equity market (i.e., the black line has declined) for much of the last several years, and especially since early this year. There has been a bounce in EEM relative performance very recently, but the overall trend in relative performance remains negative.

The middle section is perhaps the most important in our work. It plots the relative earnings estimate revisions indicators for the two ETFs. Like the other indicators on the chart, the revisions indicators are based on the actual historical constituents and weights of the ETF holdings, hence the indicators are cap-weighted like the underlying holdings. The red line reflects the difference in earnings estimate revisions breadth (i.e., the positive/negative revisions ratio) between the two ETFs, while the blue bars indicate the difference in estimate revisions magnitude (i.e., the monthly percentage change in consensus next-12-month earnings per share across all the ETF holdings).

Readings below zero indicate that estimate revisions for the EEM holdings are weaker than those of the broader ACWI ETF holdings, and readings above zero show stronger estimate activity in EEM vs ACWI. The readings over the last 12 months have been negative, but most of the weakness has occurred during 2021. Indeed, the recent readings are extremely negative by historical standards, indicating an unusually wide divergence between emerging markets and developed markets in terms of analyst earnings estimate revisions activity.

This tells us that EM stocks in this benchmark have, in aggregate, weaker earnings trends than their developed market counterparts. Part of this is no doubt due to the crackdown by the Chinese government on a number of industries, which has prompted analysts to downgrade earnings forecasts for the related companies significantly. This has a major impact, as Chinese stocks comprise 32% of the weighting in the EEM ETF, the largest country weighting by far.

But it is not only China that is weighing on EM fundamental metrics. We also have the same indicators for the ETF tracking the Emerging Markets ex China index (ticker EMXC), and it shows a very similar pattern. So revisions activity in non-China emerging markets is also quite weak relative to developed markets.

The one potential favorable sign in the chart above is that relative valuations, plotted in the bottom section (purple line) are now much more favorable for EM. The valuation shows the relative forward earnings yield (inverse of P/E ratio) for EEM vs ACWI, with higher values indicating EM stocks are cheaper (higher yield) relative to the global benchmark. Recent readings are at the high end of the five-year range, as stock prices for EM have fallen even faster than the earnings estimates on a relative basis, pushing the relative earnings yield higher.

On a shorter-term basis, we find that valuations are typically less useful for timing purposes than estimate revisions or price indicators, but may be a better metric for longer-term views. Thus we would not overweight EM stocks based purely on relative valuations, but would wait for signs of improvement in relative fundamentals and investor sentiment.

Given the extreme negative relative fundamentals visible in EM right now and the equally strong negative return momentum, we would continue to underweight/avoid EM for now. This is especially true given that the Chinese government’s longer-term plans regarding various key industries remain unclear, and many emerging markets are struggling with COVID-19 and lower vaccination rates than in developed economies. These are trends that are unlikely to reverse quickly, and thus in our view present an ongoing risk for holding EM stocks, even at more favorable valuations.