Before the Q1 earnings reporting season, the US had been gradually slipping on relative earnings estimate revisions metrics, but the Q1 results came in much stronger than expected almost across the board. With the Tech/AI leadership in the US resurgent, the US has jumped back near the top of our regional revisions rankings, supporting our ongoing overweight stance. At the same time, our estimate revisions metrics within Emerging Markets show AI-tied Taiwan and Korea as the dominant leaders, while the rest of the EM space is mixed to negative. Japan has mostly maintained strong earnings trends despite higher energy prices and lack of dominant AI companies.

Q1 earnings had a big impact on US earnings estimates.

Earnings reports for Q1 are mostly done now, and the regional results were striking: earnings and projections in the US were much stronger than expected, and not just because of mega-cap Tech. Ex-US markets saw far more moderate responses in aggregate.

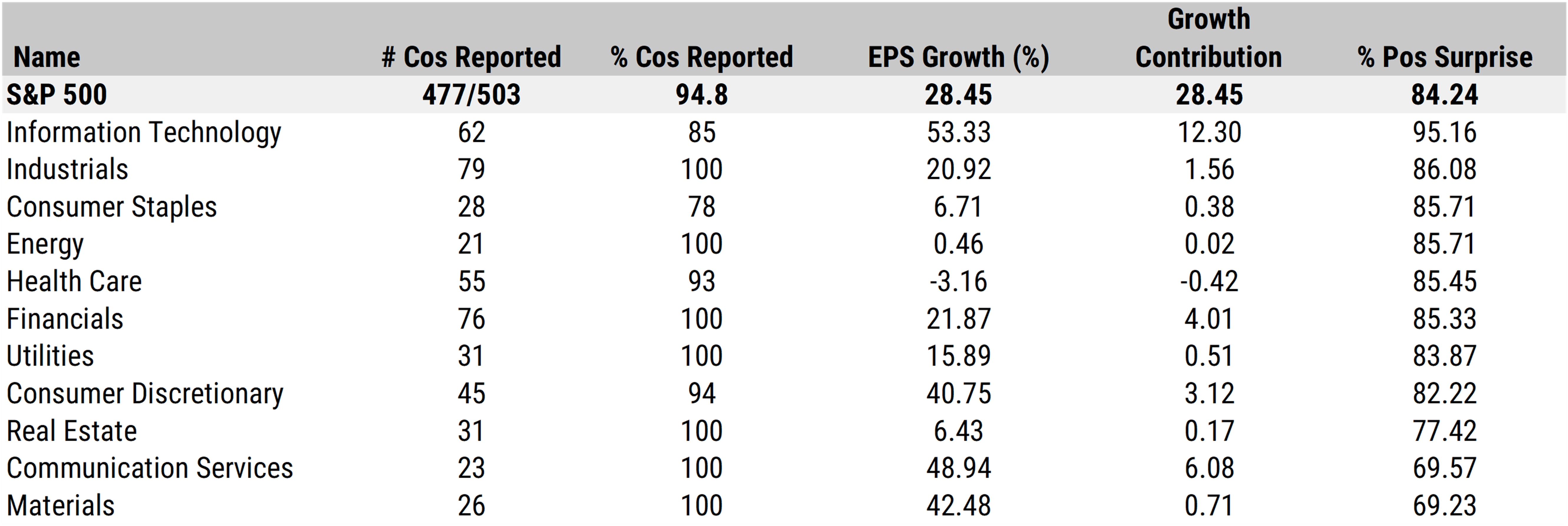

The Q1 earnings season just wrapping up was extremely strong in the US, both in absolute terms (S&P 500 EPS up 28.5% from the year-ago quarter), and relative to consensus expectations. Factset’s data (with 95% reporting) shows that 84% of the S&P 500 constituents beat estimates, a very high number even for the S&P 500. And of the 62 Technology stocks in the S&P 500 that have reported Q1 earnings, 95% beat consensus estimates. And among the Technology industries, Semiconductors, Technology Hardware, and Communications Equipment all have 100% of their constituents beating consensus right now.

But it was not exclusively Tech that came in above expectations. Most other sectors have high beat rates above 80%. And while Technology had a massive 53% year-over-year earnings growth rate, there were big gains in Communication Services, Materials, Consumer Discretionary, Financials, and Industrials.

Source: Mill Street Research, Factset

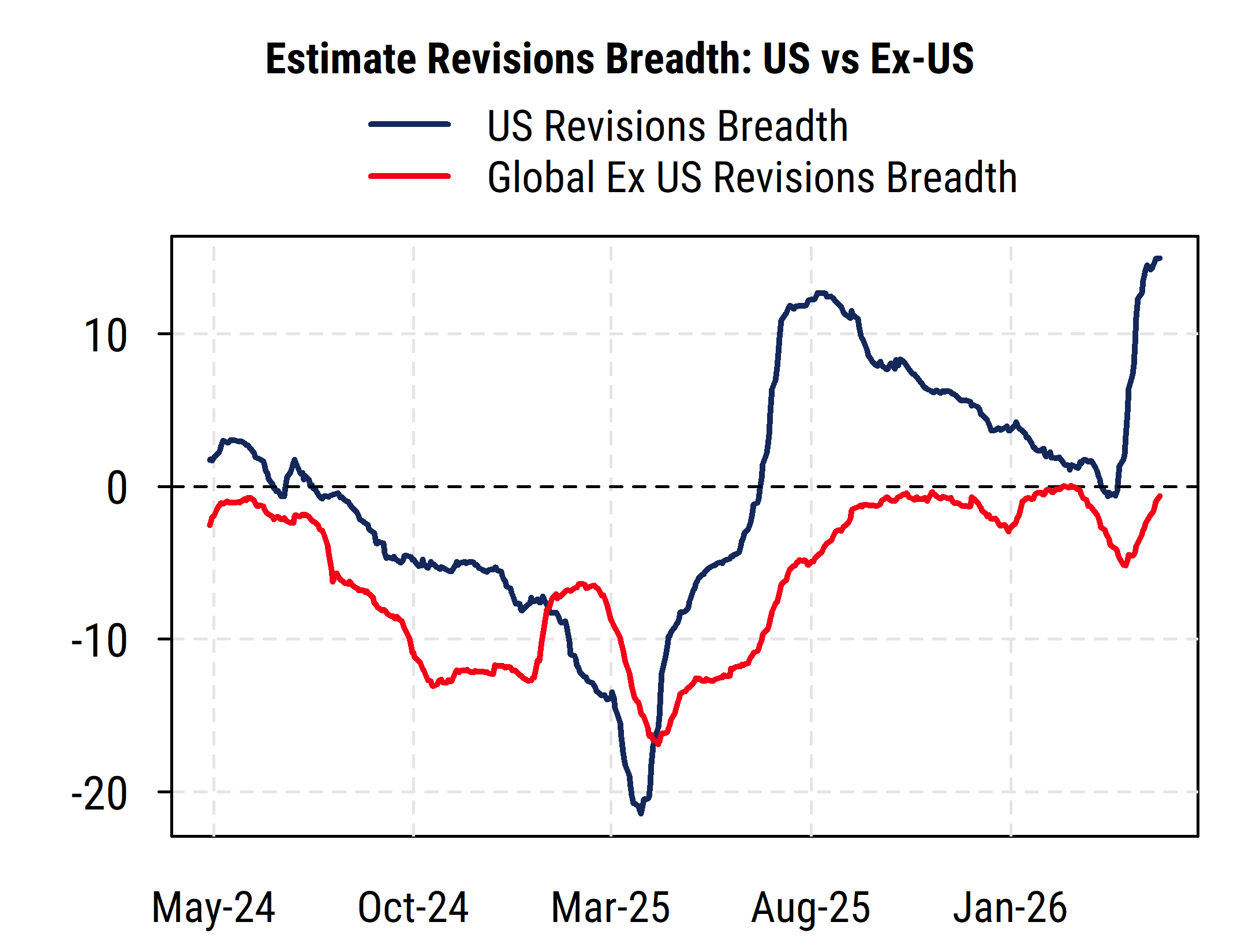

Not only did the earnings for Q1 come in better than expected in the US, so did the guidance about future earnings trends from company managements. The response from analysts has been dramatic: earnings estimate revisions surged to strongly positive readings in the US as Q1 reports came out. However, this was not the case outside the US in aggregate: our revisions metrics in the rest of the world rose only modestly. The chart below shows this clearly, using our equal-weighted, all-cap aggregate revisions breadth readings for the US and global ex-US universes (i.e. not dominated by mega-caps). Revisions breadth is our measure of the proportion of analysts covering a stock that have raised their next-12-month EPS estimates net of those who have lowered estimates in the last 100 calendar days. It thus ranges from -100% (all analysts cutting EPS forecasts) to +100% (all analysts raising EPS forecasts). Broad-based analyst movements tend to be persistent and have more price impact.

Source: Mill Street Research, Factset

The US has been above the ex-US average for most of the last year (interrupted by the tariff-related moves in April 2025), but the gap has now widened dramatically. US revisions are decisively positive, and at some of the highest historical readings outside of post-recession recoveries.

Since the US is the center of the Tech universe and Tech/AI has been so strong lately, does that mean the US revisions strength is just capturing Tech relative strength?

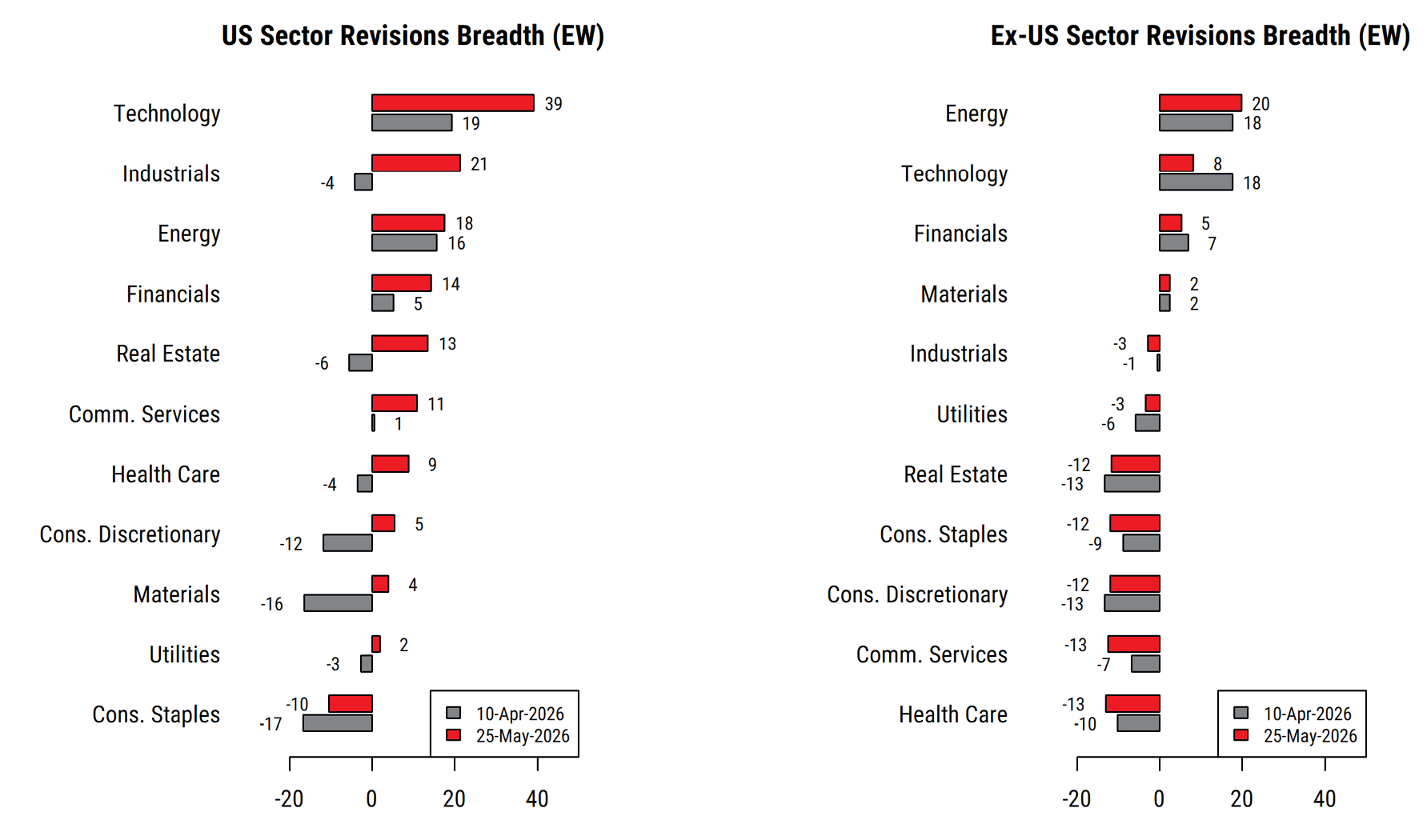

Our data says no: the improvement in US revisions readings is broad-based across sectors, though it does very much include significant improvement in the Tech sector. The left chart below shows the revisions breadth readings for all of the US sectors (equal-weighted) as of April 10th (grey bars), the day before Q1 earnings reports started, and as of May 25th (red bars). Of the 11 sectors, 10 clearly improved and one (Energy) was little changed, including the Consumer sectors despite the impact of higher energy costs.

The right chart below shows the same figures for our global ex-US universe. In stark contrast, it shows much less improvement, with most sectors (also equal-weighted) either roughly the same or worse on revisions breadth after Q1 earnings, with Technology notably worse. So it has been very much a trend in estimate revisions favoring the US, and quite broadly in the US rather than just narrowly focused on Technology.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

AI driving Taiwan and Korea, but not much else outside the US

Emerging markets remain widely divergent, as the AI-tied markets of Taiwan and Korea are extremely strong while much of the rest of the EM space is mixed or weak, with China still lagging badly.

We have maintained our neutral allocation recommendation in Emerging Markets because the majority of EM stocks are below-average on earnings metrics and are not performing very well. There are, of course, some EM stocks and specific markets that are doing very well, and the common theme is exposure to the AI mania that is sweeping the globe now.

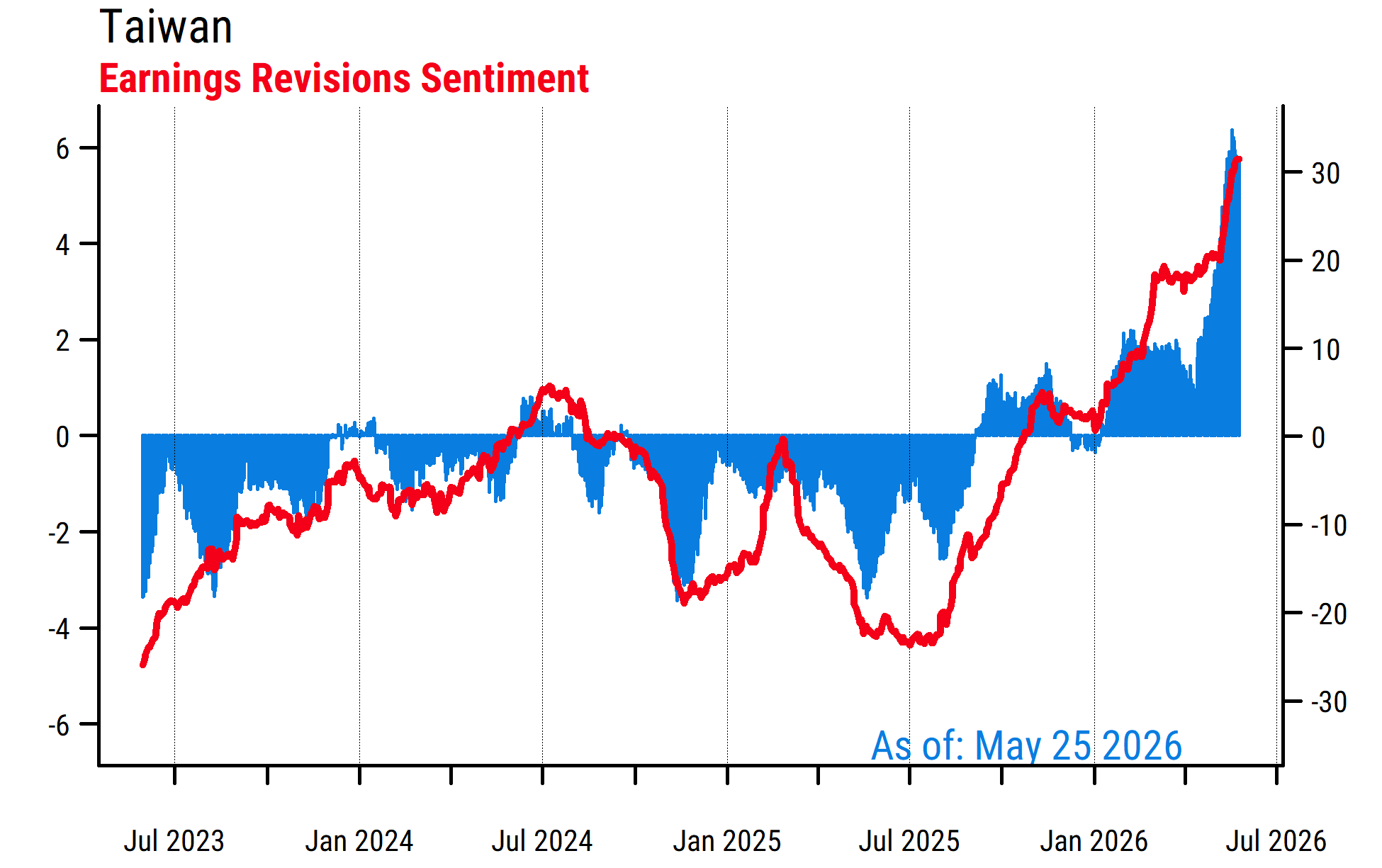

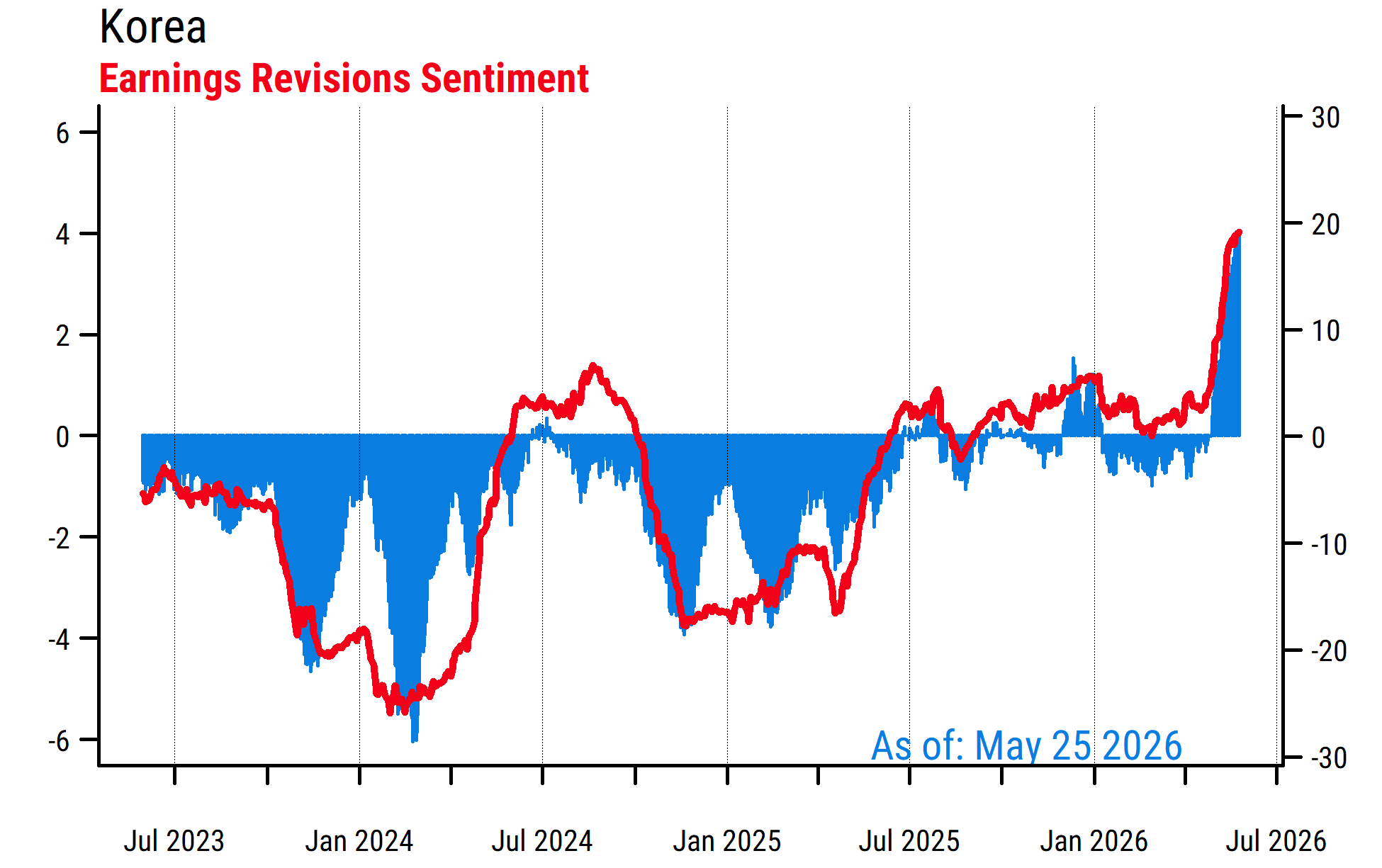

Taiwan and Korea are the two markets seeing the most dramatic support from their ties to AI hardware. And both have seen a big positive response to Q1 earnings reports, extending what were already above-EM-average estimate revisions breadth readings.

The chart below shows our equal-weighted Taiwan revisions metrics, with the red line indicating the average revisions breadth and the blue bars indicating the average revisions magnitude (average 30-day percent change in next-12-month EPS estimates).

Here, giving equal weight to all 118 Taiwan listings in our database is important in light of the massive size of Taiwan Semiconductor. That single company alone, with a $1.8 trillion market cap, makes up 57% of the cap-weighted benchmark MSCI Taiwan index (which has 83 constituents), while the next biggest component is 4.6%. Taiwan Semi also makes up 14% of the full MSCI Emerging Markets index (with 1204 constituents). But our equal-weighted data show that the strength in Taiwan’s revisions extend beyond just the one dominant name, as many other Taiwan listings are in the Tech space and benefiting from the broader demand growth.

Source: Mill Street Research, Factset

Korea is similar, though to a somewhat lesser degree. It too has seen a surge in revisions breadth after Q1 earnings to very strong readings. It has two dominant mega-caps that are massively benefiting from AI-driven demand: Samsung Electronics (32% weight in MSCI Korea) and SK Hynix (21%), but also has broader strength reflected in our equal-weighted universe of 205 stocks.

Source: Mill Street Research, Factset

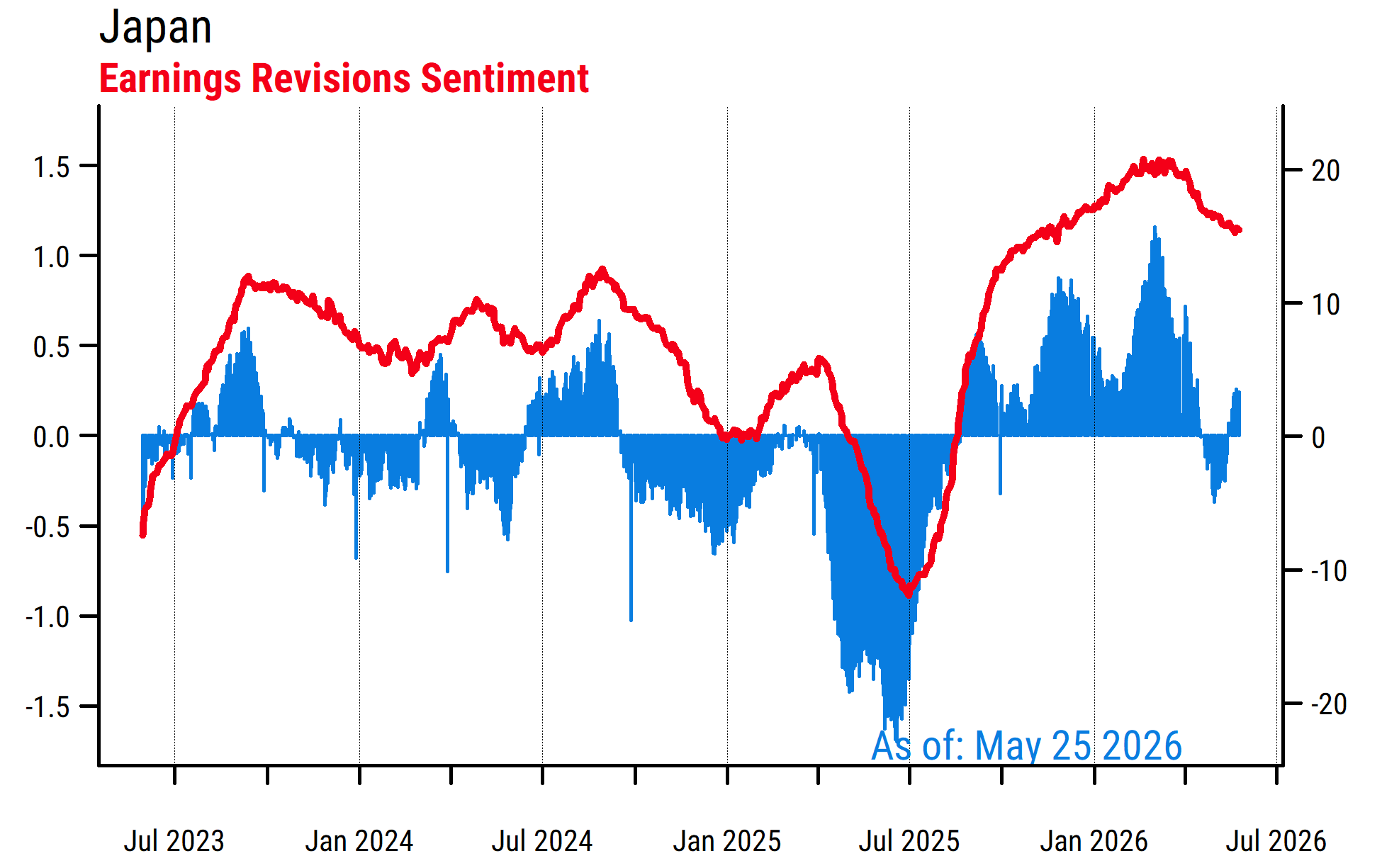

Notably, Japan has had strong estimate revisions metrics for months now, and still does, and we have been overweight as a result. However, Japan has seen a bit of easing lately as the Bank of Japan has intervened in the currency markets to support the yen, and higher energy import costs are having some impact. Japan has some Technology exposure but not much direct AI exposure relative to Korea, Taiwan, or the US. The positive trend in Japan’s earnings are more idiosyncratic, and consistent with the normalization of interest rates there in recent years.

Source: Mill Street Research, Factset

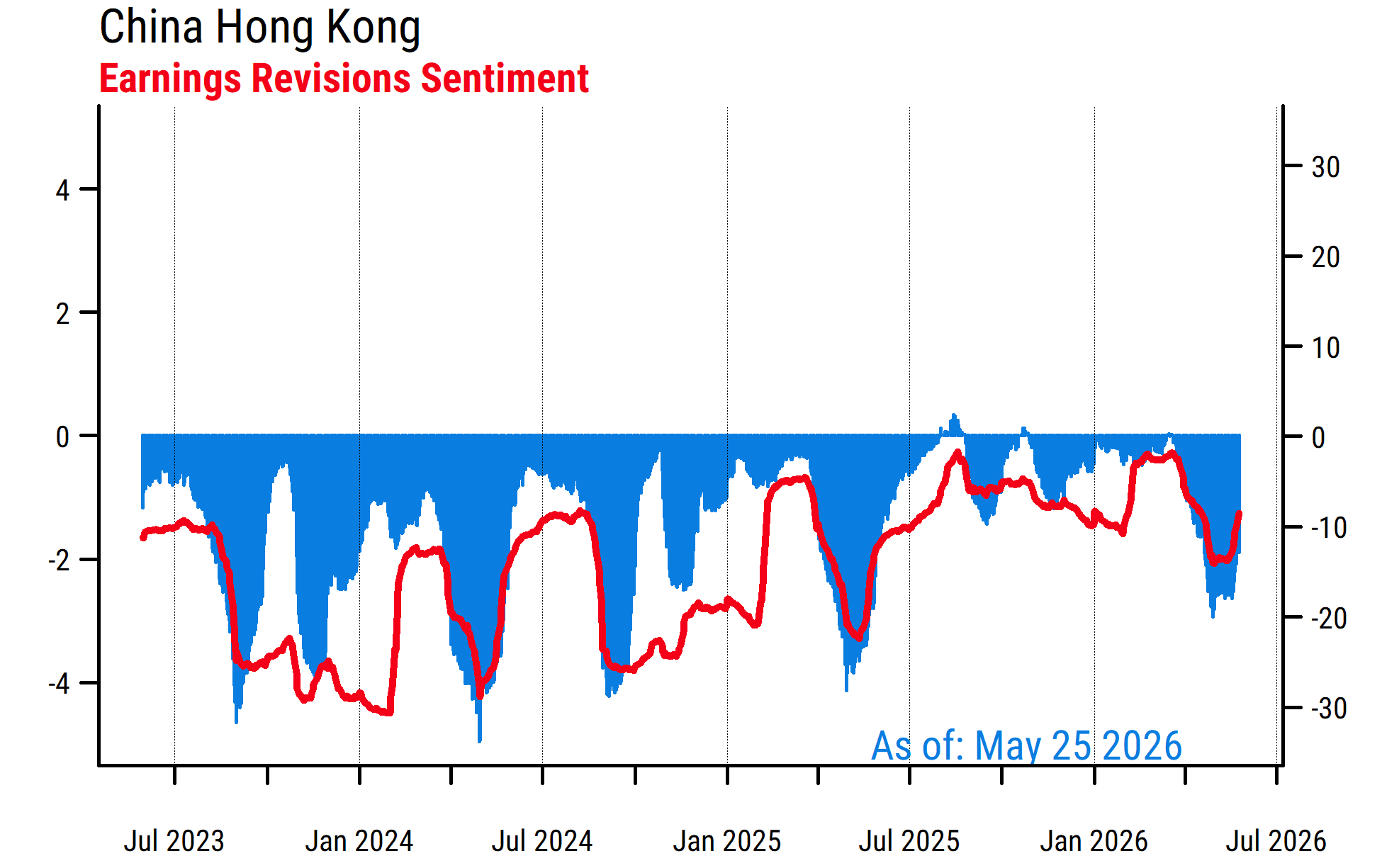

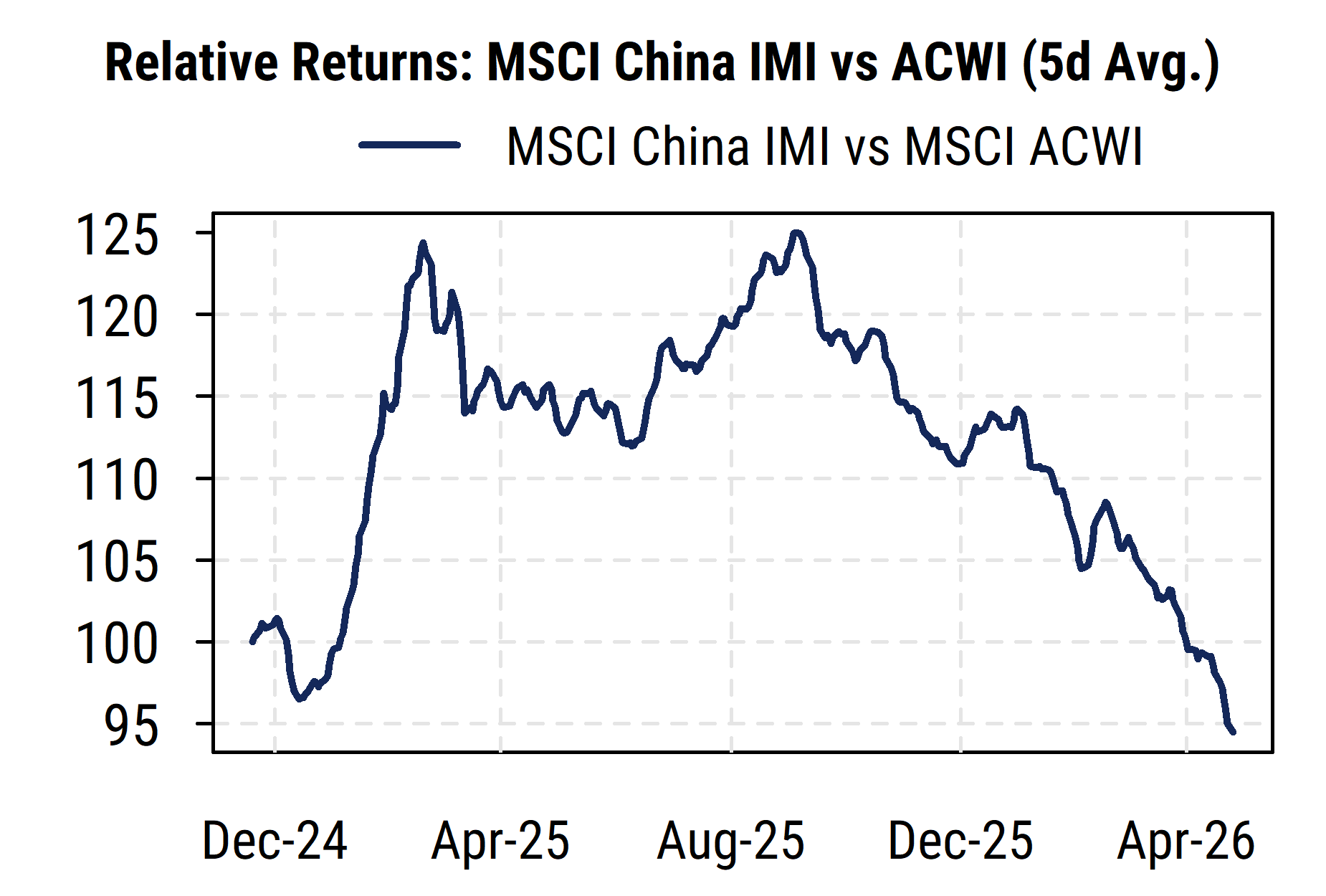

In stark contrast, China remains quite weak, and is still a big drag on the overall EM universe. Revisions breadth for our China+Hong Kong universe (828 stocks) remains solidly negative and has seen only modest improvement after Q1 earnings reports, as shown in the first chart below. The MSCI China index has been lagging the MSCI ACWI index for months and is showing no signs of a turn (second chart below). China has many Tech companies and some AI exposure, but its many other economic headwinds are still offsetting any Tech-related benefit for corporate earnings overall.

Source: Mill Street Research, Factset

Tech/AI is bigger than Oil/Middle East for stock prices and earnings, and the US has strong earnings growth across most sectors.

The key points are that Tech/AI is the key driver of earnings, outweighing energy/commodity industries, and the recent backup in bond yields has done little to dent the enthusiasm for AI-related Tech.

In the US, Tech is the big driver, but not the only sector doing well: other sectors are also seeing big earnings gains. Outside the US, the trends are much more muted, with energy more of a headwind and Tech/AI less of a tailwind, except in Taiwan and Korea that have some of the dominant AI companies right now, and Japan which has its own earnings improvement trend still in place.

Sam Burns, CFA

Chief Strategist