17 August 2022

The stock market has rallied sharply since mid-July, while long-term bond yields have been stable to lower. Even the mighty US dollar has paused a bit in its uptrend. But inflation remains high (though likely peaking) and Fed officials continue to say they will continue to raise rates (and reduce the balance sheet) well into next year. The old market adage says “don’t fight the Fed” (i.e., be cautious when the Fed is tightening policy, and more aggressive when they are loosening), but it looks like markets have in fact been rallying in spite of the Fed lately.

There are a few reasons why the markets are behaving as they are, which may make they idea of “fighting the Fed” less worrisome, at least for now:

- A lot of bad news, including further aggressive Fed tightening, was priced into markets by June, making any sign of improvement a reason to rebound.

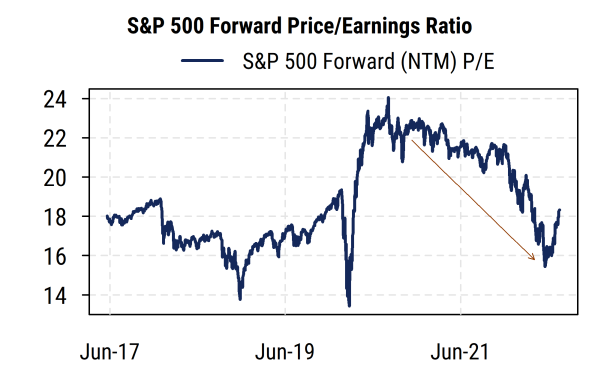

- The forward P/E on the S&P 500 fell 32% from its peak, a large move historically, and in mid-July it had reached more compelling levels around 16.

Source: Mill Street Research, Factset

-

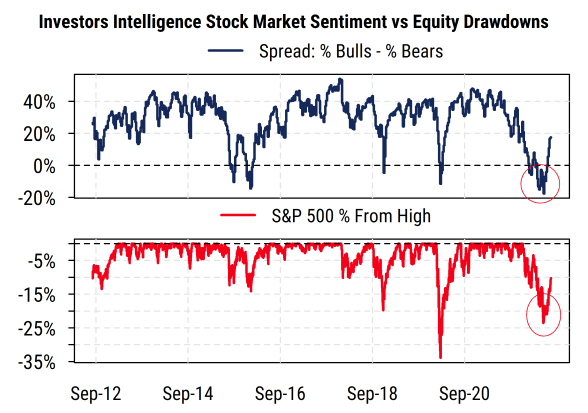

- Investor surveys showed levels of bearish sentiment typically seen near market lows.

Source: Mill Street Research, Factset, Investors Intelligence

Source: Mill Street Research, Factset, Investors Intelligence

This is somewhat less true now that stocks have rallied significantly.

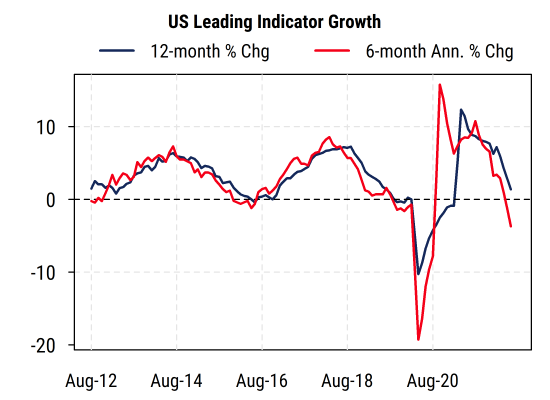

- Investors are betting that, in the end, the Fed will respond to the economy rather than strictly to reported inflation. Leading economic indicators have already slowed, and further slowing is likely to cause the Fed to slow or halt its rate hikes by early next year.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

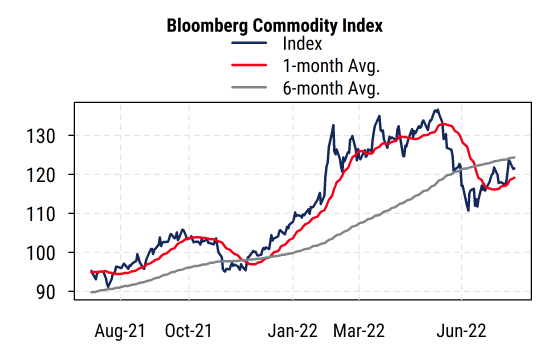

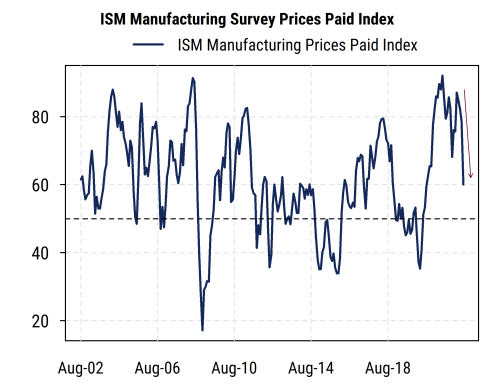

- It looks like the worst of the inflation pressure is behind us, and as that shows up in the data, the Fed will have reason to be less aggressive. Commodity prices have already corrected significantly, as have prices for shipping, and this is showing up in data like the ISM Prices Paid index.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

- The Fed does not necessarily have to do all of the work to slow demand, as China’s economy in particular has slowed dramatically (to the point that they are trying to stimulate their economy) and reduced global demand for commodities and other things.

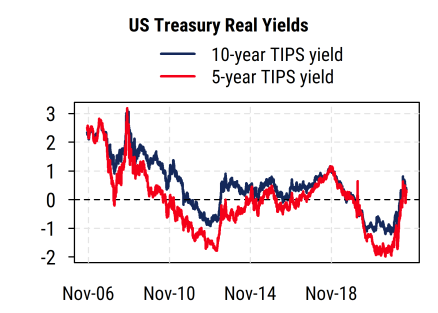

- While well off their lows, real interest rates remain low or moderate by historical standards and thus are not yet particularly restrictive for company or individual borrowing, and do not offer highly competitive returns versus equities at this point. That is, the economy and market may be able to handle current or somewhat higher rates before they become a major headwind (though this partly depends on fiscal policy, which has been tightening as well).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

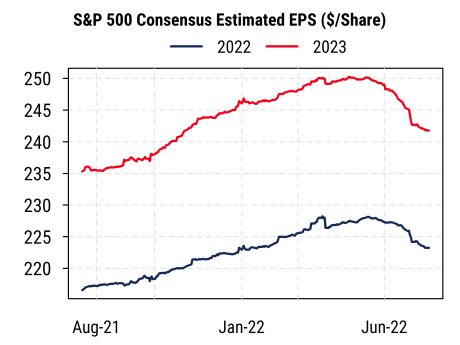

- Earnings estimates have fallen recently, but are still projecting about 8% growth this year and next year.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

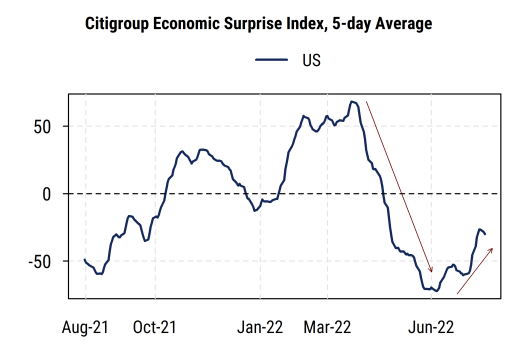

Returning to the first point, it is easy to focus on “what is going to happen” in the economy and earnings and forget about “what is already priced in” when analyzing markets. Surprises, or revisions to consensus expectations, are what drive markets, and recent economic and earnings data has arguably been “less bad” than previously anticipated.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

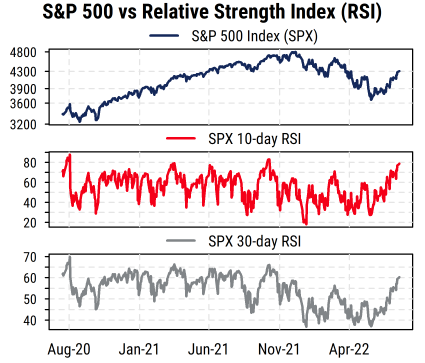

It looks like the downtrend in equities has been broken, but stocks may be overbought in the short-term, suggesting there could be some choppiness for a while.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

We recently shifted from underweight to neutral on equities in our asset allocation work, as our intermediate-term indicators (including the one based on Fed expectations) have improved noticeably but are not yet fully bullish. We still prefer stocks over long-term bonds (which we remain underweight), and are keeping an overweight in cash for now.