One of the themes in our sector research for clients recently has been to focus on relative preferences within broader style or macro categories, rather than making big macro bets on Growth versus Value or Cyclical versus Defensive areas. We find that in a more range-bound market with conflicting macro trends, a more granular view is often more effective.

One stance we have held for some time has been within the Value-oriented commodity space. While in many cases historically the Energy and Materials sectors have moved together, this year has seen a dramatic divergence between the two commodity-related sectors. We have favored Materials over Energy this year, and still do, and below are some of the drivers of that view.

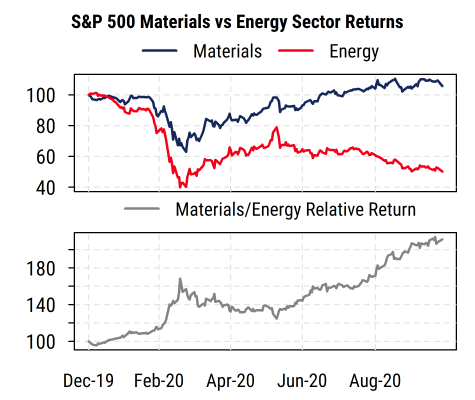

The first chart below shows the returns of the S&P 500 Materials sector and the S&P 500 Energy sector for this year, along with the relative performance (all indexed to 100 at the start of the chart), as of October 27th.

The collapse of the Energy sector this year has been historic, and comes after less extreme underperformance that was already occurring in 2019. The S&P 500 Energy sector total return index has declined -50% this year, by far the worst performing of the 11 major sectors in the S&P 500. This compares to the 6.5% gain for the S&P 500 overall.

The Materials sector, despite also being tied to global economic turbulence and commodity prices, has held up far better. Its year-to-date gain of 5.6% is only marginally behind the overall index, and vastly higher than that of Energy. And the relative outperformance trend has been consistent most of the year, both before the COVID-19 volatility in March and afterwards.

What explains the performance gap in these two commodity sectors?

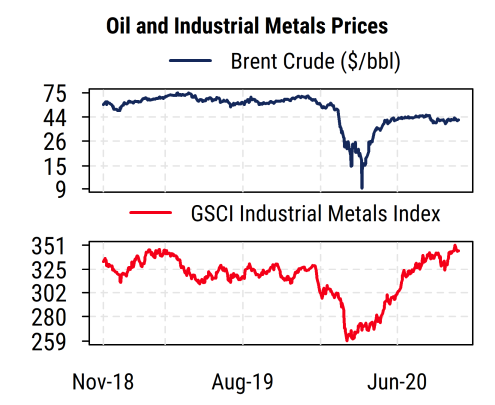

First, the underlying commodities they are most closely tied to have followed very different paths this year. Crude oil prices are still far below their level at the start of the year (down about 40% for benchmark Brent crude), and even the current level of oil prices relies on the aggressive production cuts put in place by oil producers globally. So oil producers are facing the combination of lower prices and lower production, causing a severe drop in revenues. Naturally, the effects of severely depressed fuel usage due to COVID-19 travel limitations are a major factor in oil demand, and remain in place.

By contrast, industrial metals prices such as copper, aluminum, zinc, etc. (represented by the S&P/GSCI Industrial Metals index) have fully recovered their COVID-related decline and then some. Resurgent demand from China in particular as well as the strong US housing market have helped support prices for these metals used in manufacturing and housing, and are benefiting from the reflationary efforts of global central banks. Along with the increases in precious metals prices (gold and silver) this year, many of the stocks in the Materials sector have a relative tailwind to earnings from commodity prices.

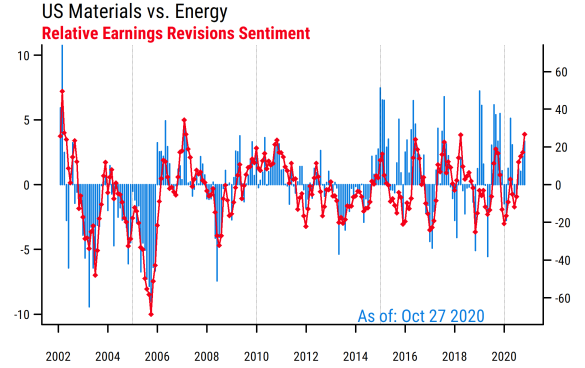

The effect of these divergent commodity price trends is also showing up in relative earnings estimate revisions activity. Analysts have been much more inclined to raise their earnings forecasts for Materials companies than for Energy companies, and that remains the case today. The chart below shows our aggregated relative earnings estimate revisions metrics for Materials versus Energy in the US. Readings above zero on the chart indicate more favorable analyst estimate revisions trends in Materials relative to Energy (red line indicates the relative proportion of analysts raising vs. lowering estimates, right scale; the blue bars indicate the average relative percent change in consensus estimates for the next 12 months, left scale). We can see that the readings are strongly in favor of Materials over Energy and have been for several months now.

With fundamental trends and relative returns both still pointing toward Materials over Energy within the commodity space, we would maintain relative positioning along those lines.