5 May 2022

Yesterday’s Fed policy announcement was certainly the focus of attention, and monetary policy has been driving headlines and market action for much of the year. However, our view is that fiscal policy is likely the bigger policy force in the economy nowadays, and fiscal tightening started some time ago.

Official monetary policy tightening is just getting started

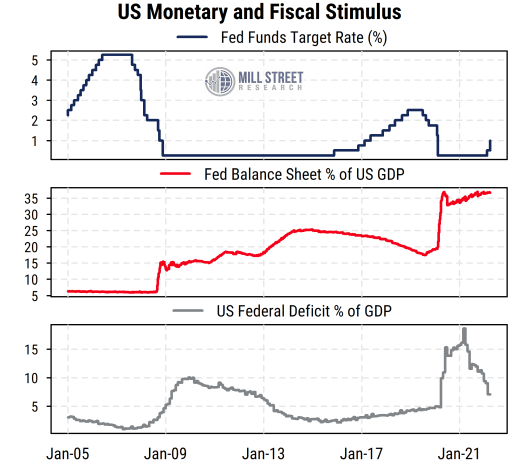

The chart below shows two measures of monetary policy and one measure of fiscal policy. The top section plots the widely-watched Fed funds target rate. This is the rate directly managed by the Fed, and represents the cost for commercial banks to borrow reserves from each other, thus serving as a base rate for most other rates in the economy.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

After having been dropped to near zero in the immediate aftermath of COVID’s first impact here in the US in March 2020, the fed funds rate stayed there for almost exactly two years until the Fed raised the rate 25bps in March of this year. Yesterday the Fed took a more aggressive stance and raised the rate 50bps, the first time the central bank has imposed an increase of more than 25bps at a single meeting since 2000. While this was the consensus expectation for this meeting, markets reacted favorably to comments from Fed Chair Jay Powell that the Fed is not considering an even larger 75bps move in the upcoming meetings.

Even after these two moves, however, the upper end of the Fed’s target rate range is now only 1%. Compared to the recent reported inflation rates of 8.5% for the headline CPI and 5.2% for the core PCE price index (the Fed’s preferred gauge), the current rate still looks very low. That is, real short-term policy rates are still heavily negative, just slightly less so than before.

The market certainly believes the Fed will continue raising rates more aggressively throughout the rest of this year at least, which explains why even after pulling back yesterday, the current two-year Treasury yield is around 2.65% (a proxy for expected average short-term rates in the next two years).

The other thing the Fed announced yesterday was its initial plan for reducing its balance sheet, meaning allowing some of the bonds it had bought as a way to support financial markets and reduce longer-term borrowing rates to mature (“roll off”) and not be replaced. In addition to the dramatic rate cuts in early 2020, the Fed also bought huge amounts of Treasury and mortgage-backed bonds, along with a few corporate bonds, as a way to stabilize markets and keep borrowing costs under control. The bond buying program continued until recently, pushing the size of the Fed’s holdings up dramatically. The Fed’s security holdings reached an amount equal to about 36% of total US GDP, much higher than the previous peak around 2014-15 of about 25% of GDP.

The Fed will now start reducing its balance sheet at a rate of $47.5 billion per month, and move the pace up to $95 billion/month over the next three months. These actions essentially place more bonds in private investors’ hands and thus increases supply and reduces demand relative to the last two years. This is the other reason bond prices have fallen sharply recently (pushing yields higher), as investors have anticipated the Fed’s (well-telegraphed) action and tried to position accordingly.

All of this means that official monetary policy tightening (as opposed to market-driven tightening that has already happened) is only really just getting started. Many investors have argued that the Fed is “behind the curve”, meaning they have waited too long to react to high inflation pressures. This is debatable given the supply-driven nature of much of the recent inflation, but there is little doubt that the Fed has waited much longer than usual to begin tightening policy.

Fiscal policy is well ahead of monetary policy

While investors have long focused more on monetary policy than fiscal policy as a driver of economic growth and inflation, the last 15 years (at least) argue that fiscal policy is more important than Fed policy in driving growth and inflation, in our view.

The dramatic recovery in the US economy (which has generally outpaced other developed economies since 2020) was driven more by the massive fiscal support provided starting in mid-2020 than by the Fed’s actions, in our view. The scale of the fiscal stimulus (stimulus checks, PPP loans, expanded unemployment benefits, etc.) was far larger than anything seen since World War II, and certainly larger than the stimulus provided after the 2008-09 Great Financial Crisis.

That can be seen in the bottom section of the chart above, which plots the size of the rolling 12-month US federal budget deficit as a percentage of US GDP. At the peak reading the deficit was more than 15% of the size of the economy, and a significant portion of it came from direct payments to US households, thus directly providing spendable money to individuals and businesses.

However, many of the COVID-related stimulus programs ended during 2021, and so federal spending has fallen off sharply relative to those peak levels. The deficit as a proportion of GDP has already dropped back down to about 7%, which is below the levels seen in 2010-12 and not far above the pre-COVID levels of 2019.

Thus fiscal policy has already been tightening for roughly a year now and is no longer aggressively stimulative relative to historical norms. Fiscal policy is not yet at a point where it would be called “tight” (restrictive of economic activity), but arguably will be far less of a driver of inflation pressure (“excess demand”) than it was in 2020-21.

This drop-off in fiscal support is one reason why we suspect inflation pressure may also start to ease later this year, due to the lagged effects of fiscal policy. With the Fed also tightening policy, we are now in a situation of both major policy drivers acting to dampen demand. This is one reason why stock prices have been under pressure, as investors are concerned that such a combined policy shift will limit future economic and earnings growth.

Of course, much depends on external factors like the war in Ukraine, China’s response to COVID, supply chains, etc. But current policy conditions suggest some economic slowing is likely already underway, which may limit the eventual scope of Fed tightening relative to current expectations as they opt to avoid tightening aggressively into an economic slowdown.