14 April 2022

As Q1 earnings season gets under way, below we review the current consensus estimates for the US (S&P 500) and Europe (Stoxx 600).

U.S.

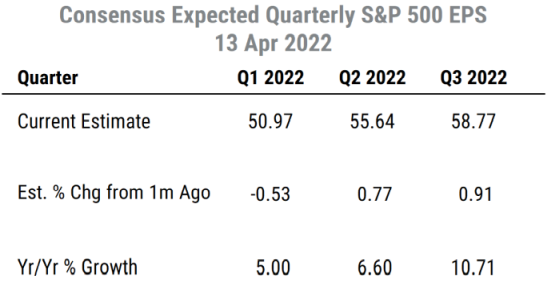

The table below shows the current bottom-up consensus estimates for the S&P 500 for Q1, Q2, and Q3 of this year.

It also shows the percentage change in each quarterly estimate from one month ago, and the expected percent growth in earnings from the year-ago quarter.

Q1 estimates have slipped slightly over the last month, which is typical historically but unlike some recent quarters when estimates continued rising ahead of reporting season. However, estimates for Q2 and Q3 have continued rising.

Expected year-on-year earnings growth is still positive but now more in line with historical norms (5-10%) as the stimulus-driven earnings surge is mostly done.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

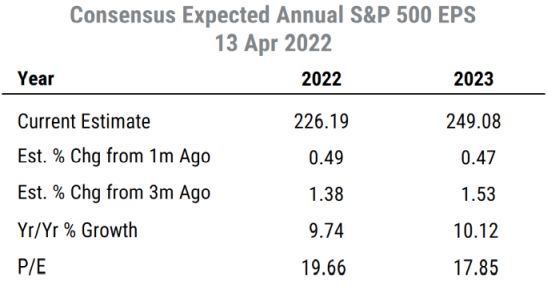

The table below shows the current bottom-up consensus estimates for the S&P 500 for this year (2022) and next year (2023).

It includes the change in each calendar year estimate from one month ago and from three months ago, along with the expected growth rate from the previous year and the current P/E ratio based on each year’s estimate.

Estimates for this year and next are still rising, and by similar amounts. Earnings this year and next are expected to be up roughly 10%, suggesting some real growth on top of inflation.

The P/E for this year is currently just under 20, while next year’s P/E is about 18. These figures are well off their peaks but still somewhat higher than the pre-COVID valuation levels.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

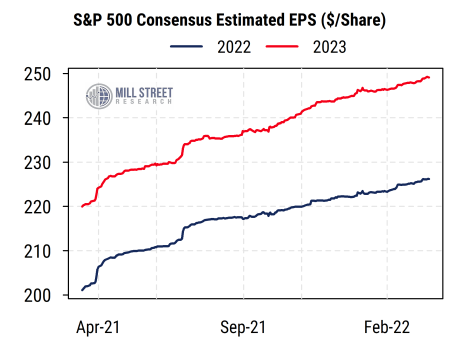

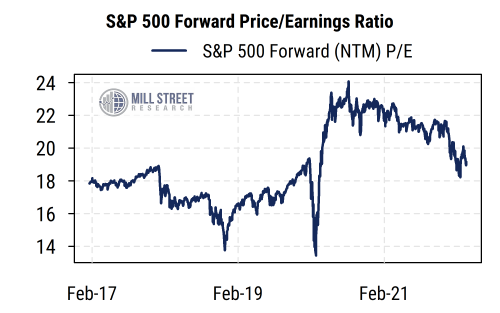

The charts below shows the evolution of the calendar year estimates, and the history of the forward (next-12-month) P/E on the S&P 500.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

EUROPE

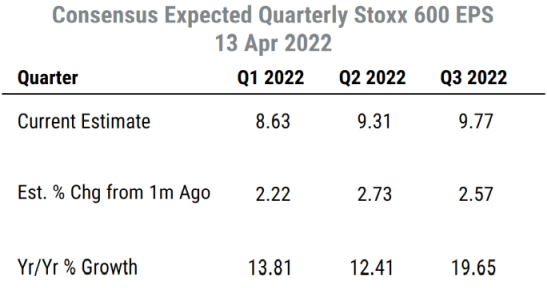

The table below shows the current bottom-up consensus estimates for the European Stoxx 600 index for Q1, Q2, and Q3 of this year.

It also shows the percentage change in each quarterly estimate from one month ago, and the expected percent growth in earnings from the year-ago quarter.

Unlike the US, the estimates for Q1 in Europe have risen significantly over the last month. The estimates for Q2 and Q3 have also risen by similar amounts (around 2.5%).

Year-on-year growth for each quarter is expected to be double-digits, suggesting continued recovery in earnings from COVID-driven weakness despite the war in Ukraine. Rising inflation in Europe is also a driver.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

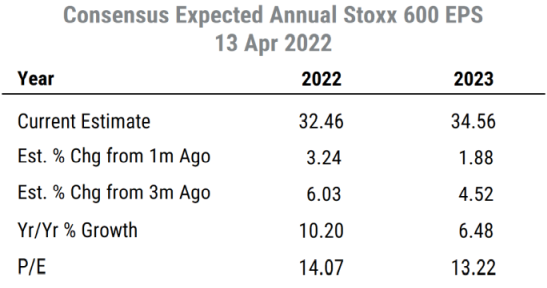

The table below shows the current bottom-up consensus estimates for the Stoxx 600 for this year (2022) and next year (2023).

It includes the change in each calendar year estimate from one month ago and from three months ago, along with the expected growth rate from the previous year and the current P/E ratio based on each year’s estimate.

Estimates for this year and next are still rising at a solid pace (the 2022 estimate has risen 3% in the last month). Earnings this year are expected to be up about 10%, and then about 6.5% next year.

Even though Europe is being affected much more directly by the war in Ukraine and did not have the same level of post-COVID fiscal stimulus as the US, earnings estimates are nonetheless rising sharply. Some, but not all, of this growth in nominal earnings is driven by inflation (especially energy costs).

The P/E for this year is currently near 14, while next year’s P/E is about 13. These readings are in line with pre-COVID valuations, and remain much lower than those in the US.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

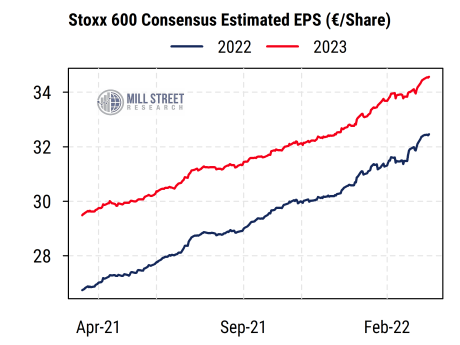

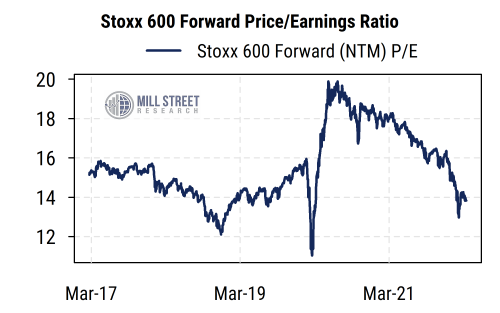

The charts below shows the evolution of the calendar year estimates, and the history of the forward (next-12-month) P/E on the Stoxx 600.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset