21 April 2022

Inflation remains a big topic among investors, and the charts below clearly show some of the reasons why, but there are also reasons to suspect inflation pressure could ease later this year.

Inflation is high . . .

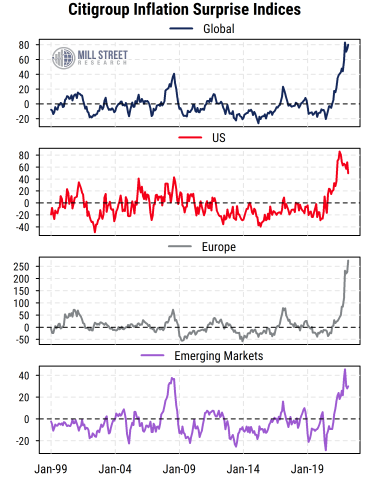

A barrage of recent headlines has made it hard not to notice that reported inflation is very high (e.g. US CPI year-on-year change at 8.5%). More importantly for markets, inflation has continued to come in above expectations. The Citigroup Inflation Surprise indices (chart below) measure the degree to which inflation reports come in above or below consensus expectations. The indices for the US, Europe, Emerging Markets, and the global aggregate are all still extremely high relative to historical norms. Europe is by far the most extreme, as it is affected most directly by the war in Ukraine and the resulting impacts on energy prices and many other commodities.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

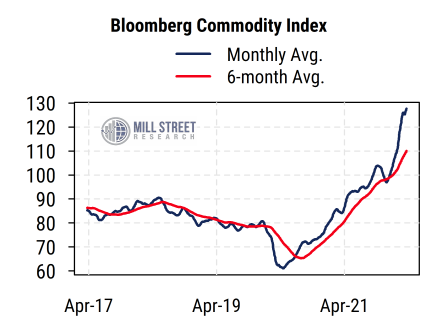

And commodity prices remain a concern. The Bloomberg Commodity Index (chart below) has continued to surge far above its pre-COVID levels. The recovery in demand and still-constrained supplies due to COVID have now run into the additional supply shock caused by Russia’s invasion of Ukraine and subsequent sanctions. While the pass-through from raw commodities to consumer prices varies by sector and by country, the trend remains worrisome.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

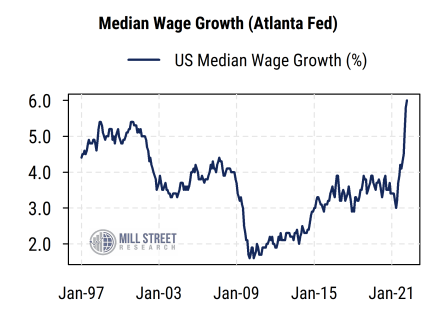

If commodity shortages are one key source of inflation pressure, the other factor most often cited is wage pressure. The chart below shows the year-on-year change in the US median wage as calculated by the Atlanta Fed. It avoids the composition issues that affect the usual average hourly earnings figures (when the types of workers covered in the sample change over time) by tracking individuals’ wages over time, and avoids the skew toward high-income individuals that occurs in aggregate figures like personal income data.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The median wage growth data show a jump in wages recently as labor markets have tightened sharply. The year-on-year rate of about 6% is the highest since the data begin in 1997. Thus there has clearly been cost pressure on companies facing both higher labor costs and higher commodity costs.

While there is no question that inflation is high in the US and many other countries, the question on investors’ minds is whether it is still getting worse or if it might slow down as the year goes on.

. . . but inflation could ease later this year

The war in Ukraine and COVID both remain highly uncertain global factors that could drive inflation higher for longer than currently anticipated. This is especially true if Russian oil and gas become more severely restricted. The effects of COVID seem to be on a volatile but improving trend globally, though China’s recent lockdowns highlight the ongoing difficulties in dealing with the virus.

From an economic standpoint, however, there are reasons we might expect some improvement in the inflation backdrop as the year progresses, especially in the US.

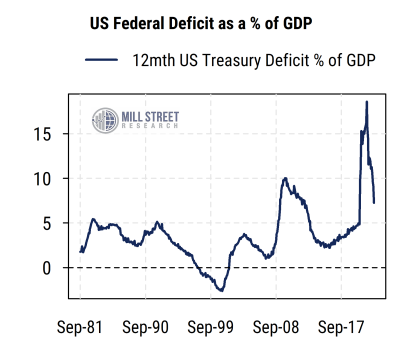

First, while much attention is paid to the Fed and monetary policy, in our view it is fiscal policy that is much more important now. Fiscal stimulus in the US reached historic proportions in the aftermath of COVID, reflected in the extremely high federal deficit/GDP ratio (chart below). That ratio, however, is coming down quickly as pandemic-related spending programs end and tax revenues increase. A narrowing deficit should reduce some of the “excess demand” that forms part of the inflation story.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

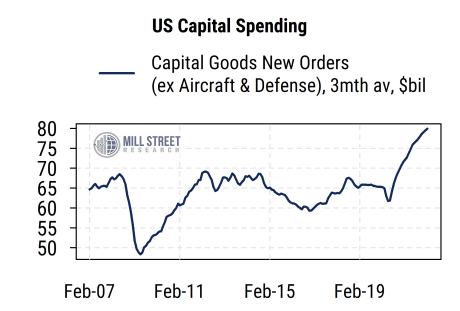

Second, corporations have responded by sharply increasing capital spending to improve productivity and thus keep costs down. We see that new orders for capital goods (excluding aircraft and defense) have been rising sharply and are now well above the levels seen in the 15 years prior. If this spending does in fact improve productivity, that could help mitigate cost pressures.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

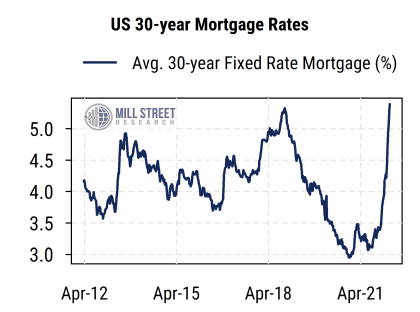

And a third thing to keep in mind is that the debt markets have done some of the work already. In particular, the rate on traditional 30-year fixed rate home mortgages in the US has jumped to just above 5% recently, from a recent low of near 3%. This is near the highest level in the last decade, and will likely impact housing demand and prices in the coming months (refinancing activity has already fallen off sharply).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

All of these factors act with a lag of some kind, making it hard to estimate when and how much they might affect reported inflation. But they remind us that things may look different six to nine months from now, which may also affect the Fed’s eventual policy posture.