2 March 2022

While we hesitate to comment too much on the situation in Russia/Ukraine given how fast conditions are changing, many investors are naturally interested in the market impacts of the recent invasion and the resulting sanctions.

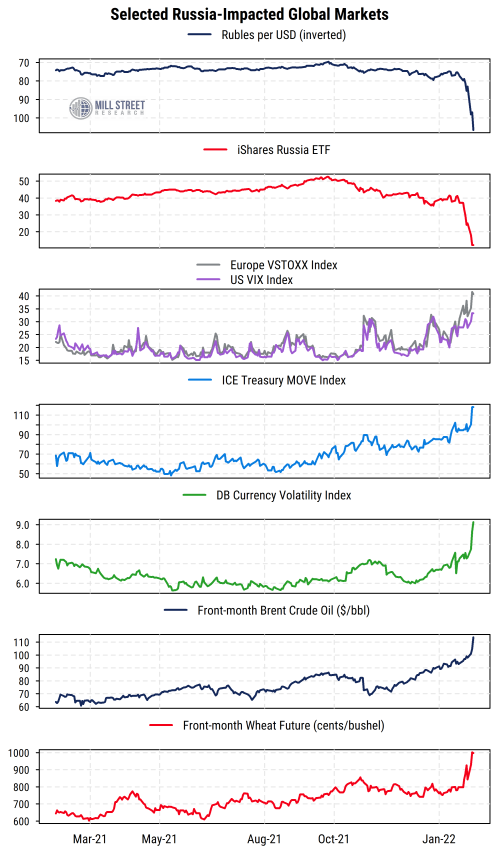

The first order impact is clearly volatility, in many different markets. Stocks, bonds, currencies, and commodities are all seeing increased volatility recently amid extreme uncertainty surrounding the unprecedented global response to Russia’s invasion of Ukraine. And of course, Russian assets of all kinds have seen their prices plunge, if they are still being traded at all — the Russian stock market has remained closed since February 25th.

Oil and gas are the key global commodities being affected, as concerns grow about supply from Russia being reduced or cut off. This is especially concerning in Europe, which relies significantly on Russian energy supplies. Some food-related commodities are also feeling pressure, including wheat (a key export of Russia and Ukraine), along with important inputs for fertilizer.

The chart below captures some of the market movements in the context of the last 12 months.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

The Russian ruble and Russian stock market have collapsed (top and second section of chart), with trading in all Russian markets either closed or severely curtailed. The price of the US-listed iShares Russia ETF, for instance has fallen from about $41/share on Feb. 16th to around 10-12 now (it is very volatile and new ETF share creation has been halted), a decline of around 75%.

The US VIX (implied volatility on the S&P 500) and European VSTOXX index (implied volatility on the Euro STOXX 50 index) have both jumped further (third section of chart). The VSTOXX is now near 40 (vs a 10-year average of 20), and the VIX is holding above 30 lately, the highest since 2020. US stock prices, though volatile, have been mostly in a range over the last week and still in correction territory from the early January peak.

US Treasury bonds, though acting as a safe haven lately, are also feeling the impact. The haven demand for bonds is countered by the Fed’s imminent start of a rate hike cycle to fight inflation, which has pushed yields up in recent months. The ICE MOVE index (fourth section of chart), a counterpart to the equity VIX index for US Treasury bonds, has jumped to 118 as of yesterday’s close, nearly double the 10-year average level of 65.

Currencies outside of the ruble are also being affected. The Deutsche Bank Currency Volatility index (fifth section of chart), similar to the VIX, reflects implied volatility in the major currency markets. It too has surged recently to its highest levels since the COVID shock in early 2020, though it was coming from lower levels and is now only moderately above the 10-year average.

Crude oil prices (sixth section of chart) have been the focus of concern within commodity markets, given Russia’s major role in the global oil market and the existing upward pressure on prices from demand recovery and supply limits by OPEC and US shale producers. The near-term Brent crude price has jumped above $110/bbl, adding to inflation pressures. However, the oil market (like some others) is currently in heavy backwardation, meaning that oil for current delivery is priced much higher than oil for delivery 6-12 months from now – the December 2022 futures price is about $20/bbl less than the current contract, signaling heavy demand for immediate oil supplies relative to longer-term future demand. For context, the futures price differential of current vs eight months forward has averaged near zero over the last 10 years, and rarely exceeds $5/bbl either way.

Wheat prices have also jumped recently (bottom section of chart), though they too have been working higher over the last year. Russia and Ukraine are significant exporters of wheat (and other crops) globally, so the war and related sanctions are expected to constrain supplies. In addition, the costs of key agricultural inputs like fertilizer have risen due to higher prices for commodities produced in the region like ammonia, potash, etc, which may affect other crops (e.g. corn) and food prices more generally as well.

This is far from an exhaustive list of the market impacts of Russia’s recent aggression and global reactions to it, but provides some perspective on how broadly the effects are being felt and some indicators to watch for when conditions change.