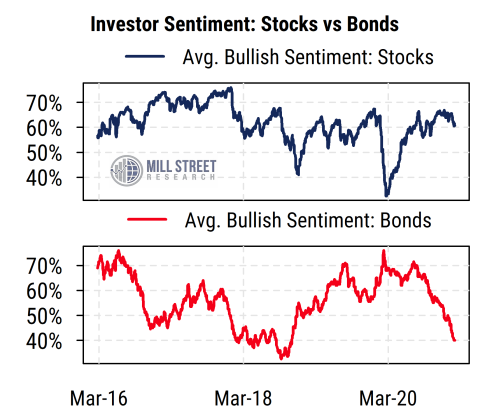

Despite what you might hear or read some places, investor surveys do not show an extreme level of optimism toward US stocks. Bullishness on stocks has in fact declined somewhat recently and is not far from long-term average readings.

Sentiment toward bonds, by contrast, has moved quite sharply and is now approaching extreme bearishness by the standards of recent years. This is not too surprising, given that long-term Treasury bond yields have recently risen to their highest levels since COVID hit early last year. The result has been that investors in long-term (20+ year) Treasury bonds have lost about 13% since the end of November and about 18% since the end of July.

One of our key measures of survey sentiment for equities is shown in the top section of the chart below. It is an average of several sources, each of which monitors the proportion of market commentators who are bullish or bearish on equities. They include Investors Intelligence, Market Vane, and Consensus Inc.

Source: Mill Street Research, Investors Intelligence, Market Vane, Consensus Inc.

The average proportion of bulls on stocks right now is about 60%, down from a recent peak in January of 67%. The average proportion over the last five years has been just over 57%, so the current reading is only slightly above average. The peak in the last five years (and in fact since at least 2003) was at 76% back in January 2018 (when the corporate tax cuts were going into effect), while the lowest point in the last five years was the brief reading around 33% in late March of last year amid the worst of the COVID-related panic. Readings below 50% on this metric are relatively rare outside of panic periods.

These survey readings stand in contrast to other sentiment-related indicators like put/call volume ratios, certain valuation metrics, or anecdotal “indicators” like the popularity of SPACs or the extreme behavior of “meme stocks” with heavy retail trading activity. Other market-based measures of risk appetite (e.g. relative performance of riskier stocks) suggest investors are still broadly in a “risk on” mood.

Sentiment readings that are not extreme in either direction tend to give less information about future returns. But we can certainly see that stocks have often done well when sentiment has been near current levels, as sentiment has been around these levels since August . Extreme bearishness tends to be the strongest signal for stocks, but occurs relatively rarely given the long-term uptrend in US stock prices.

The negative sentiment toward bonds suggests that the recent rise in bond yields may be getting somewhat stretched. If investors continue to assume that the Fed is not changing its current policy guidance and will keep short-term rates near zero for at least the next year or two, then long-term yields may not have too much further to rise.

Taking the next step, if equity investors are growing more concerned recently about risks that higher bond yields may cause regarding the level of stock prices (i.e., a higher discount rate reduces the present value of future earnings), then sentiment toward bonds is worth watching as part of the broader picture facing equities.