24 March 2022

Client Question: There is a possible world war going on along with a seemingly never-ending pandemic, inflation is at multi-decade highs, the Fed and other central banks are tightening monetary policy, and the world may lose access to Russian oil and gas entirely soon – why aren’t you massively bearish on stocks, which everyone knows is the high-risk asset class?

Answer: While naturally reserving the right to get more cautious on stocks (we downgraded equities to neutral on Feb. 14th), there are a few reasons we are not more bearish on stocks or the broader economic outlook at the moment.

- Arguably a fair amount of the bad news has actually been priced in, or at least was a couple of weeks ago before the latest rally.

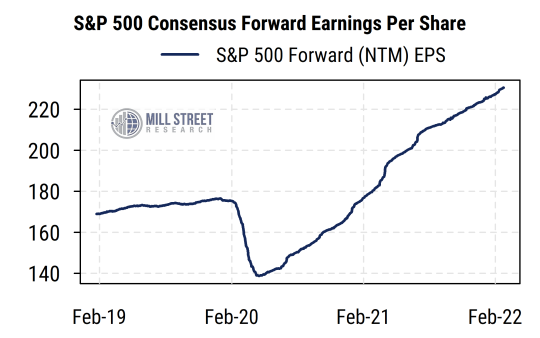

- If inflation is the concern, stocks are a better natural inflation hedge than bonds, since corporate earnings will broadly move along with inflation. Earnings estimates are still rising for the S&P 500.

- In our view, unlike many past cycles, bonds are still unattractive relative to equities even after their latest rise in yields.

- The Fed looks less likely to over-tighten monetary policy than it has in past cycles, limiting the scope for a Fed-induced recession.

- Fiscal and trade policy among Western economies looks better positioned to adapt to the challenges of COVID and Ukraine than might have been the case previously.

A key reason inflation is typically associated with recessions and bear markets is that inflation is associated with aggressive central bank tightening, and often over-tightening, which is what causes the recession (not inflation itself). The Fed in particular seems to have changed its response to inflation/growth to allow more inflation (particularly if driven by supply constraints the Fed cannot control) and try not to fight inflation purely by forcing the economy into recession with very tight money. Will it in fact follow through on that now that inflation is quite high and it is feeling the pressure? We don’t know, but so far the markets are priced as though they will not overtighten, and we tend to agree, marking a dramatic difference with many of the past cycles.

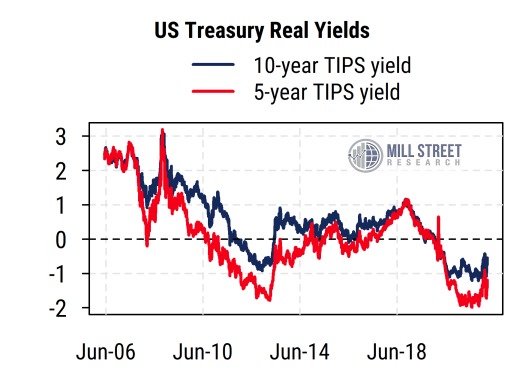

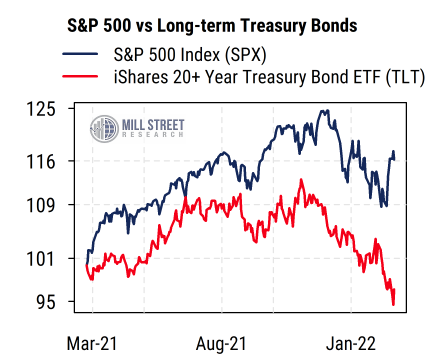

Relatedly, in many past cycles, the Fed’s tightening and investor sentiment had pushed interest rates, both real and nominal, up high enough relative to stock yields to make bonds an attractive alternative to stocks. That is not the case in this cycle so far. Even after the recent back-up in yields, bonds are still yielding less than expected inflation and TIPS yields remain negative. Thus bonds still do not offer an appealing alternative to stocks in our view, and indeed long-term Treasuries have underperformed equities materially this year (both are down, but “safer” bonds are actually down more than stocks).

Source: Mill Street Research, Bloomberg, Factset

Source: Mill Street Research, Bloomberg, Factset

On a shorter-term basis, investor sentiment got quite bearish recently:

-

- The Investors Intelligence survey showed more bears than bulls (a relatively rare occurrence),

- the VIX index had been very high (above 30) for some time,

- Major equity index deviations from 200-day averages had reached levels often associated with at least interim lows.

Thus the sharp rebound in stocks we have seen recently is not surprising as a response to excessive near-term pessimism. If sentiment reverses to more optimism while other conditions are negative, it would potentially argue for another step down in equity exposure.

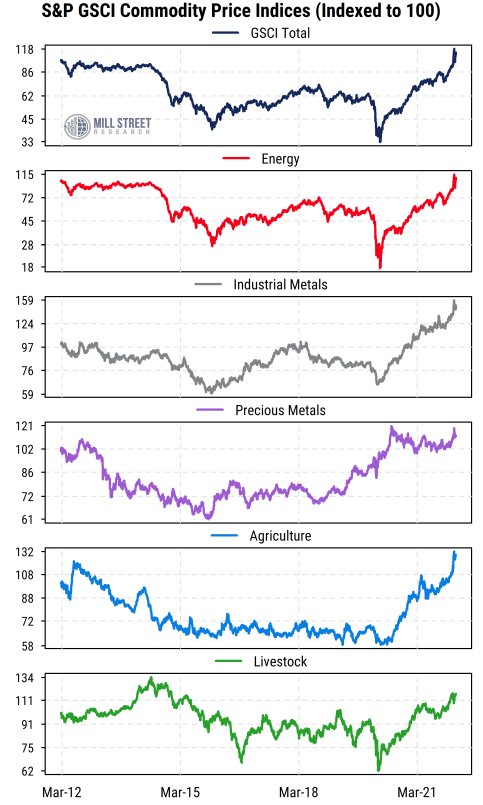

Higher commodity prices, particularly oil, are certainly a negative for inflation and economic uncertainty, but the economy is less sensitive to energy now than it was in the past (certainly than in the 1970s). Also, there is still scope for supply increases in oil if prices remain elevated. The same is true for natural gas and LNG (liquified natural gas) trading, though these will take time.

And as we pointed out recently, commodity indices are even now only modestly above the levels of 10 years ago for several categories. So while the pace of increase recently is distressing, we have lived with prices like these before and the economy and markets held up. Higher prices eventually bring about more supply and reduced demand for things that have gone up the most in price.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

Forward earnings estimates for the S&P 500 are still rising fairly steadily (with inflation being passed through to earnings in aggregate), and the forward P/E on the S&P 500 has fallen significantly from its peak: the current P/E of around 19 is elevated but not extreme, and looks favorable in light of the low level of real interest rates.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

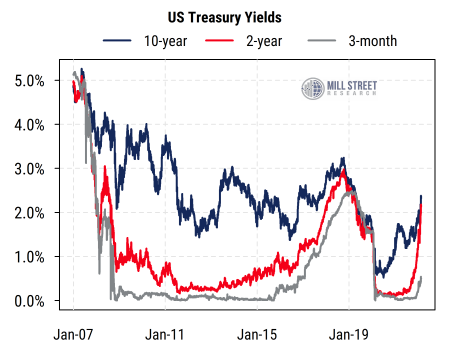

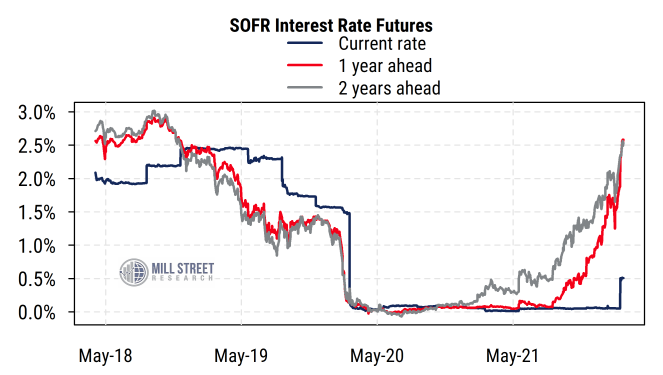

Bond yields have jumped but are not extremely high compared to past cycles, and the flat yield curve beyond the two-year maturity implies that the Fed will raise rates in the shorter-term (next 12-18 months) and then stop around 2-2.5% or so (and we suspect the Fed may not even get that far). This would still be relatively accommodative versus inflation and past rate cycles. Markets and the economy should be able to handle 2% interest rates without a major problem if inflation is 2% or higher and real growth is at least moderately positive.

Source: Mill Street Research, Bloomberg, Factset

Source: Mill Street Research, Bloomberg, Factset

While COVID has clearly not gone away, and the new BA.2 variant is spreading, the economic impact (at least in the US and Europe) is likely to be much more muted now given the presence of vaccines and existing immunity as well as better treatments. Wide-scale shutdowns look less likely, with the risk being a resurgence of people having to self-isolate when they are ill (calling in sick more). The impact on China and some other countries may be more negative, and we will have to see how that develops.

The path of the war in Ukraine is obviously highly uncertain, and we do not claim to be military strategists (nor did we claim to be epidemiologists), but history suggests that markets (at least those not directly involved, like Russia, whose markets are unlikely to ever fully recover) have been able to manage through conflicts like this as long as economic policy makers do not make major mistakes. The US and western Europe seem more willing and able to use fiscal and monetary policy to adjust to conditions than they have in the past (and than many might have expected even last year), especially in terms of Europe’s more coordinated fiscal policy.

We will continue to watch carefully for signs of a major change, and if too much optimism returns to markets, the argument might grow for reducing equity exposure further.

For now, being roughly neutral on stocks overall and underweight bonds should help navigate the current environment, with positioning within equities being important. In our view, this means favoring developed markets over emerging, large-caps over small-caps, and commodity-sensitive regions (like Canada, Australia, UK) and sectors (Energy, some Materials), or areas less sensitive to commodities (Technology, Real Estate). We would continue to avoid expensive, small-cap Growth stocks and the consumer and industrial stocks that are most sensitive to energy and other input costs.