27 May 2021

Among the biggest losers from COVID-19 and the resulting work-from-home trends that followed was the commercial real estate industry. Office buildings and retail stores that had been mostly full in 2019 were suddenly empty, and the companies that had been renting the space were often unable or unwilling to continue paying. And while stimulus support has helped much of the economy, the impact on commercial real estate has been more limited.

From an investment standpoint, the result was plunging earnings and severe underperformance by stocks in the Real Estate sector, especially those tied to office buildings and retail stores. Note that for the most part, the publicly-traded Real Estate sector has little exposure to residential real estate, which has been showing the opposite trends – the market for single-family homes has rarely seen stronger demand.

Our sector allocation views had been negative on Real Estate for quite some time, reflecting these macro pressures that were corroborated by our “bottom-up” indicators based on aggregated analyst earnings estimate revisions activity (i.e., whether analysts covering the companies were raising or lowering their earnings forecasts).

Recently, however, we have become more constructive on Real Estate, at least among the more defensive and yield-oriented areas of the market. We continue to prefer the Value and Cyclical areas such as Financials, Energy, Industrials, and Materials, but recognize that many investors want some diversification and look for guidance on which of the more defensive sectors is most attractive to balance out a portfolio.

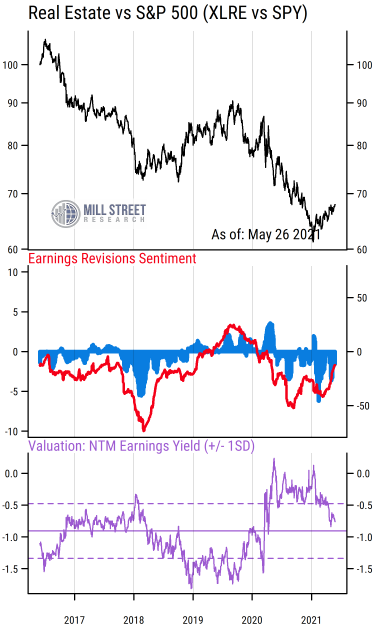

The chart below highlights our key indicators constructed for the relative performance of the Real Estate Select Sector SPDR ETF (ticker XLRE) versus the benchmark S&P 500 ETF (ticker SPY). Since the performance and fundamentals of many sectors often move together, we typically focus on the relative performance, earnings trends, and valuation of a sector versus the overall market to identify potential outperforming or underperforming areas.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The top section plots the relative price performance of the XLRE ETF versus SPY ETF. The dramatic underperformance of Real Estate last year (and actually starting in mid 2019) is clear, and the outperformance in 2018-19 only partly recovered the earlier underperformance in 2016-17. Most recently, however, we now see signs of an upturn in relative performance, suggesting that investors are showing more willingness to reallocate toward Real Estate relative to the broader market.

But is this rebound in relative returns supported by the underlying fundamentals? The middle section of the chart suggests that the answer is yes. The red line and blue bars are our measures of aggregated earnings estimate revisions activity in Real Estate (which is weighted by each company’s market value, just like the stocks in the ETF are). We can see the red line turning up from recent very weak readings, indicating that analysts are becoming less inclined to cut earnings forecasts and more inclined to raise them (relative to the corresponding behavior for all stocks in the S&P 500 index). Improvement in the underlying earnings forecasts for Real Estate companies tells us that there is indeed a fundamental reason for the nascent upturn in relative performance, and these trends tend to persist for months at a time.

Finally, the bottom section of the chart plots a measure of relative valuation of Real Estate versus the S&P 500. We calculate the forward earnings yield (the inverse of the Price/Earnings ratio) for each ETF based on the consensus aggregate earnings estimates for the next 12 months (NTM) and plot the difference between them. Higher values on the chart indicate Real Estate being cheaper (higher earnings yield, more attractive) relative to the overall market, while lower values indicate Real Estate being more expensive.

The underperformance in Real Estate in recent years pushed the relative valuation up to much higher than average levels last year (the solid horizontal line indicates the five-year average of the series), so Real Estate is coming from a position of being relatively cheap compared to the broader equity market. The recent outperformance has muted this valuation benefit, but it remains somewhat above average and far from the opposite valuation extremes (i.e., being expensive) seen in 2019.

Thus we can say that relative fundamentals for Real Estate are improving, and relative returns are also turning up at the same time. Relative valuations suggest further room for outperformance before valuation headwinds are likely to emerge. So even though the Real Estate sector is not one of the traditional cyclical sectors that are currently in the limelight, it is an out-of-favor sector that is showing clear signs of improvement and may have further to go, making it one of the more attractive places to look for defensive or yield-oriented exposure right now in our view.