10 March 2022

Commodity markets have become the center of global economic and financial market attention recently, showing unprecedented volatility. Russia’s invasion of Ukraine, coming on top of the volatility caused by COVID and the subsequent policy responses, has highlighted the supply constraints now facing a wide variety of commodities.

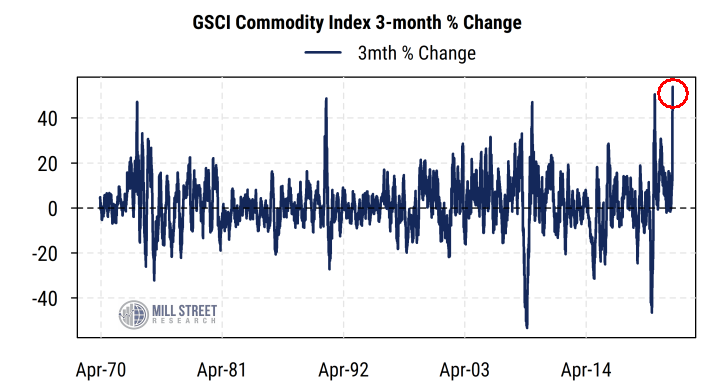

The S&P GSCI commodity price index is a widely-watched benchmark for global commodity prices, with history back to 1970. As shown in the chart below, the rolling 3-month percent change in the GSCI index has just hit its highest reading in its 52-year history. This exceeds the moves following the OPEC oil embargo of 1973-74, the 1979 oil shock, the invasion of Kuwait in 1990, the rebound in prices in 2009 after the 2008 collapse, and the rebound in 2020 from the initial COVID-driven collapse.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The latest headlines have indicated that in addition to heavy sanctions already announced on many Russian goods and services, the US and UK would stop buying oil and other energy commodities from Russia. Russia has suggested it will employ counter-sanctions by halting sales of key commodities, including nickel, which saw such a massive price spike that the London Metals Exchange was forced to halt nickel trading entirely due to the disruption and losses generated.

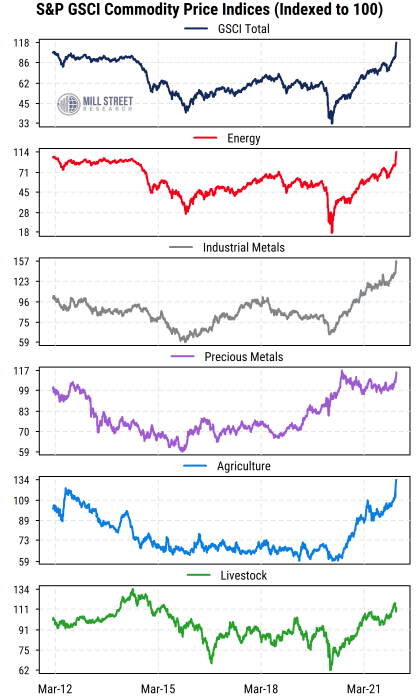

So it is clearly not just oil that is surging and causing concerns. Wheat and other grain prices have also surged, and precious metals have risen to a lesser degree as well. The chart below shows the main subcomponents of the GSCI index over the last 10 years, with each series rebased to 100 as of March 2012 for comparison.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

A few key points jump out:

- Even after the recent historic surge from the 2020 lows, the overall GSCI index is now only modestly higher than it was 10 years ago (up about 17% cumulatively, or 1.7% per year). This reminds us that the recent rise in prices comes after years of mostly flat or falling commodity prices.

- The jump in Energy prices is especially dramatic since 2020 (remember when oil futures prices briefly went negative?), having risen 82% just since December 2nd (just over 3 months ago) and 156% since the beginning of 2021. However, even those gains only bring the Energy index back to a level slightly higher than it was in March 2012 (a 1.2% average annualized rate of change). For comparison, the CPI ex food and energy is up at a 2.3% annualized rate over the last 10 years.

- Industrial Metals prices (copper, zinc, nickel, aluminum, etc.) have also surged, and are in fact higher relative to their levels 10 years ago than any of the other component indices. While demand for industrial metals is often associated with strong global economic growth, recent price trends clearly have also been influenced by supply constraints.

- Precious Metals have risen but have generally lagged the movements in other commodities and have also made little net progress in the last decade. Thus the benefit of precious metals as an inflation hedge has thus far been limited.

- The Agriculture index has made a move only slightly less dramatic than that of Energy. After years of mostly falling prices, the index of commodities like corn, wheat, soybeans, coffee, and sugar has surged due to COVID, weather, and now supply constraints from Russia and Ukraine (which are big global producers of wheat and other agricultural commodities). Like other indices, the recent painful surge (more than doubling since 2020) leaves it only moderately higher now than it was 10 years ago.

- The component that has so far shown the least dramatic movement is the Livestock index. This measure of the wholesale price of cattle and hogs has risen over the last year as well, but is much less directly affected by Russian sanctions. It too is currently only slightly higher than it was 10 years ago.

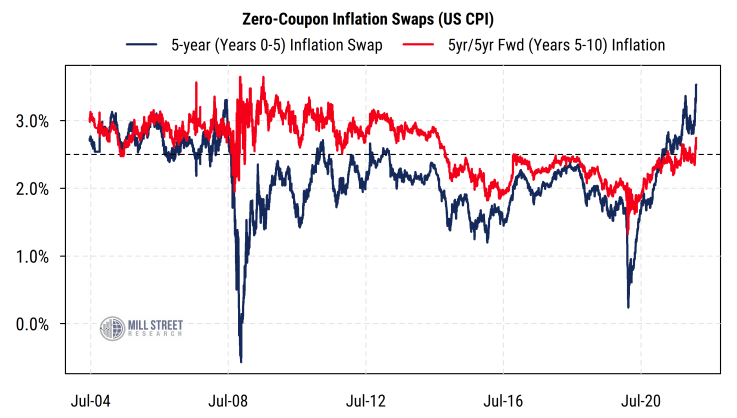

With so many commodity prices jumping recently, the upward pressure on reported inflation is likely to continue near-term. And indeed we see this in the prices of inflation swaps based on the US CPI (chart below). However, it is notable that the jump is mostly in the near-term expectations (next 5 years), while longer-term (5-10 year) inflation expectations have risen much less and remain near the Fed’s presumed inflation target (about 2.5% on CPI).

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

So even after the latest dramatic moves in commodity prices, investors’ long-run inflation expectations remain relatively well anchored, though the next year or two may have continued elevated inflation readings. This implies that investors anticipate the natural long-term mean-reversion in commodity prices that has historically tended to occur, particularly after such large moves as we’ve seen recently.

The key point in the short run is that volatility tends to be persistent in the near-term, so volatility in commodity prices will very likely continue and provoke further volatility in stock, bond, and currency markets. Policy makers will struggle to respond to such rapid movements and thus keep uncertainty higher than it otherwise would have been. In such conditions, prudence suggests keeping bets (risky holdings, or deviations from benchmark for benchmarked investors) smaller than usual.