19 May 2022

The level and growth rate of corporate earnings remain reasonably good – earnings are at record highs, and are expected to grow about 10% this year and next. However, analysts are no longer revising their earnings forecasts higher on average, halting a trend that has generally been in place since mid-2020.

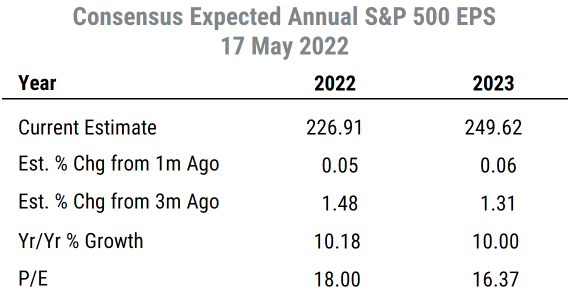

The table below shows the current consensus earnings per share estimates for the S&P 500 index (based on the bottom-up aggregation of individual company estimates). While estimates are slightly higher than they were three months ago, in the last month there has been essentially no change in either this year or next year’s estimate.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

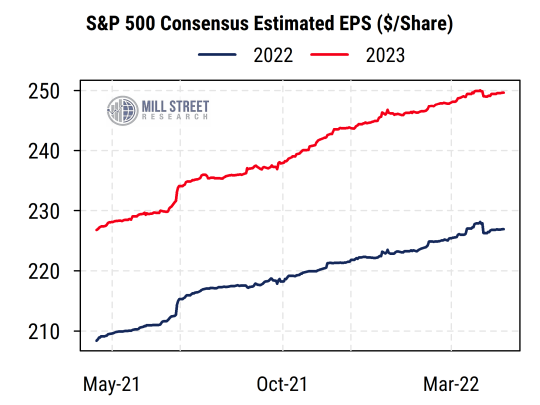

The chart below shows the evolution of the 2022 and 2023 estimates over time. After a long period of relatively steady increases, they have now mostly stabilized. This loss of momentum in earnings estimates is likely one reason (along with the rise in interest rates and inflation) that stock prices have corrected recently and brought equity valuations lower.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

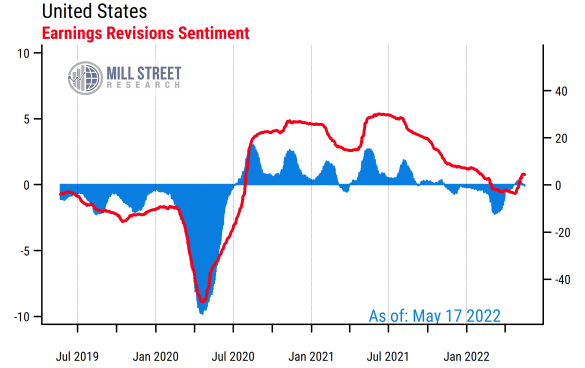

While it is useful to keep an eye on the index-level aggregate earnings estimates, we often look deeper to see where analysts are revising their earnings estimates most significantly, either up or down. Our favorite metric is what we call “revisions breadth”, meaning the proportion of analysts who have most recently raised their earnings estimates for a company net of those who have lowered their estimates. So breadth can range from -100% (every analyst has cut estimates) to +100% (every analyst has raised estimates), with 0% indicating a balance between positive and negative revisions (50/50 up vs down).

We calculate the revisions breadth for each company and aggregate the readings into an overall US aggregate (all ~2500 US stocks we track) as well as sector aggregates (among others aggregates). This allows us to see whether analysts are, on average, raising or lowering estimates overall and within each of the 11 major GICS sectors.

The red line in the chart below shows the US average breadth reading over the last three years. The blue bars show a shorter-term measure of the average monthly percent change in earnings estimates. Recently the readings have been fluctuating around zero, meaning an roughly equal number of upward versus downward revisions on average across all US stocks (each stock’s revisions figure is equally weighted in the calculation of the average)

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

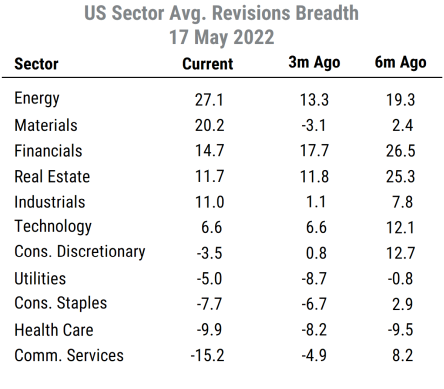

But when we drill down into sectors, we can get an idea of where the relative strength and weakness is. The table below shows the average revisions breadth for each sector currently, and the readings as of three and six months ago for comparison.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The commodity-related sectors of Energy and Materials are the strongest, both having clear majorities of analysts raising estimates versus lowering. This makes sense given the continued high prices for many commodities, especially for oil and gas, as well as steel, fertilizer, etc.

Financials, Real Estate, and Industrials are also above-average on revisions right now. Financials and Real Estate have been strong for a while, helped by greater demand for mortgages as well as commercial real estate. Industrials has improved more recently, with signs of improvement in transportation-related areas (air travel, etc.) giving a boost.

At the bottom of the list we see Communication Services, Health Care, and Consumer Staples. Communication Services (which includes a number of internet-related companies) has been under pressure in part because demand for stay-at-home online services has eased as people go back to offices, schools, etc. Health Care remains under pressure from COVID-related disruptions, and Consumer Staples is on the losing end of the inflation/commodity trends as well as the waning stay-at-home behavior. Consumer Discretionary and Utilities are feeling similar impacts as well, while the widely-watched Technology sector is mixed overall, with hardware-related areas doing better than software/services areas within the sector.

Of course, earnings estimates are not the only driver of stock prices, so returns have been influenced by the mostly risk-off market activity recently as well as interest rate movements. But as the trend of “a rising tide lifts all boats” that we saw from mid-2020 fades, it is more important to identify the relative winners and losers on the basis of their “fundamental momentum”.

The revisions data clearly shows this in terms of earnings in the current macro environment, based on the bottom-up estimate activity by analysts covering companies on Wall Street: the commodity theme remains intact, with COVID, supply chains and interest rates also still notable influences.