16 December 2022

A key topic within the broader inflation debate is the influence of the biggest single component of the CPI: shelter. At about 33% of the current CPI weight, shelter (housing/rent) costs are clearly important, but measuring them is harder than it might seem.

Some key points to keep in mind regarding the CPI and its shelter (housing) component:

1) Shelter costs are not based on the actual price of a home, but on the cost of “housing services”. This is because a house is both a fixed asset that can be financed and resold, and a provider of housing services, and consumer price indices do not want to include asset prices or financing costs. So shelter costs are based on rents, either actual market rents for homes and apartments or “owners equivalent rent” as the extrapolated cost of renting your own home to yourself.

2) The CPI is meant to track the cost of living for the average person, and since the average person does not move or sign a new lease every month, the CPI shelter index is essentially (and intentionally) a “smoothed” measure of actual market rents, with the changes in rents smoothed over roughly a year.1

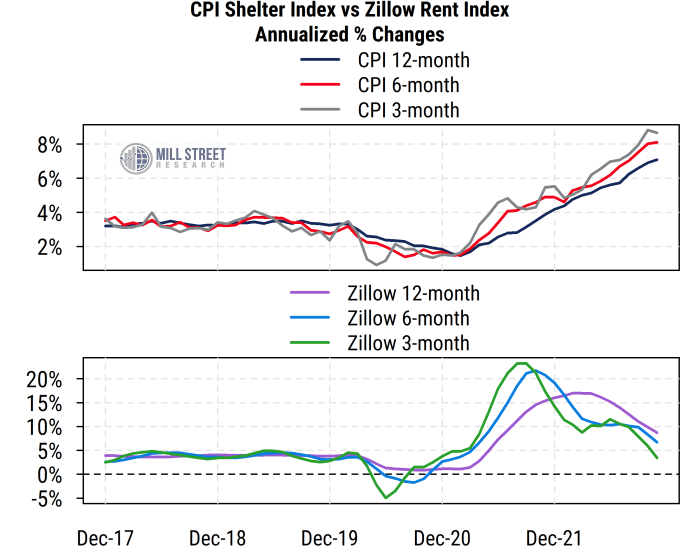

When rents are not moving too much, the differences are less visible, but the post-COVID period has seen extreme volatility in prices generally but in shelter costs in particular. Below we show two measures of shelter costs with very different implications: the CPI Shelter index and the Zillow Observed Rent Index (both through the November), a proxy for current market rents for homes across the US.

The 3-, 6-, and 12-month annualized rates of change for each are plotted, and the divergence is dramatic: the CPI series are all still accelerating, while all measures of the more timely (but volatile) Zillow data are rapidly decelerating.

Source: Mill Street Research, Factset, Bloomberg

Source: Mill Street Research, Factset, Bloomberg

Which series is “right”, or should the Fed be watching? Depends on the goal, but for forward-looking monetary policy purposes, the more sensitive and timely market rent (Zillow) data seems more appropriate despite its higher volatility. The Zillow data along with data on home prices from S&P Case-Schiller and others clearly show a rapid slowing of housing prices in recent months, in stark contrast to the data reflected in the CPI Shelter data.

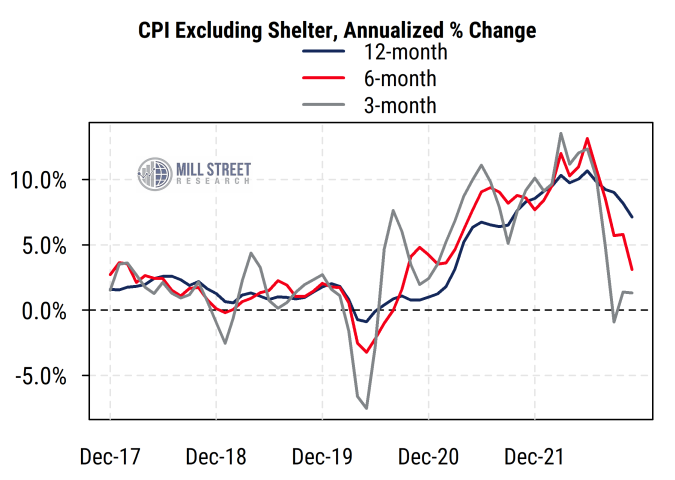

And at the December 14th Fed meeting, Fed Chair Powell indeed suggested that the Fed is well aware of the lags in the shelter price component of the CPI, and said they are also closely watching prices excluding shelter. The second chart below shows the three-, six-, and 12-month annualized rates of change in an index of the CPI excluding shelter, which thus avoids the issue of the lagged shelter inputs to the CPI.

Source: Mill Street Research, Factset, Bloomberg

Source: Mill Street Research, Factset, Bloomberg

It shows very clear and rapid deceleration in non-shelter prices, and in fact shows that the three-month and six-month annualized changes are already at or below the Fed’s 2.5% target for the CPI. However, the Fed seems to remain focused on the more widely-watched 12-month (year-on-year) changes in prices, which still reflect the jumps from early in the year before the Fed had even started its tightening campaign. The 12-month change in CPI ex shelter, though falling, is still at 7.1% and thus looks too high for the Fed to pause the tightening process given what they have said thus far.

Given the well-known lags in the effects of monetary policy, often estimated at 6-12 months, and the clear signs of slowing of both inflation pressures and economic activity, one could make a strong argument that the Fed should pause and watch the data for a few months. But thus far its rhetoric has remained hawkish, clearly indicating that more rate hikes are expected next year. The bond market, however, does not fully believe that the Fed will keep rates as high as long as their projections indicate, and thus has kept the Treasury yield curve heavily inverted.

Could the Fed really “look past” such high readings on one-third of the CPI to argue for less hawkish policy? Possibly, but it would be quite a messaging challenge given what they have said thus far. It therefore keeps alive the risk of overtightening and causing more economic pain than might really be needed to bring inflation under control.

1 For more background on CPI shelter/rent calculations, see the BLS working paper: https://www.bls.gov/osmr/research-papers/2022/pdf/ec220100.pdf