15 January 2023

Some of the common questions among fund managers who are looking at Mill Street’s stock selection and asset allocation tools are on the topic of whether using analyst estimate revisions metrics for stock return forecasting is useful:

“Do analyst estimates really matter for stocks nowadays? “

“Aren’t equity analysts always conflicted, and late in capturing news about stocks?“

“Or hasn’t the information already been arbitraged away by now?”

These are reasonable questions, and crucial to our work given the weight we put on estimate revisions-based indicators. Thus we can offer a summary of our views on the topic. However, even a “summary” is somewhat longer than our usual blog posts!

To jump to the punchline first, the short answer is “yes, our work strongly indicates that relative analyst estimate indicators are (still) useful for forecasting future relative stock returns, and can be enhanced further when combined with other measures like price momentum and valuation.”

The underlying concept is that changes (revisions) in analysts’ forecasts for a company’s profits are a predictor of future relative returns. This is distinct from the levels of the earnings forecasts, which are more likely already incorporated into the stock’s price. That is, even if analysts are optimistic in their earnings forecasts (on average), which many institutional investors know, the revisions to the estimates still contain useful information. We also note that we do not rely on analyst recommendations (buy/hold/sell) in our work, only the changes to earnings forecasts.

This captures two tendencies:

- Estimate revisions impact stock prices — investors respond to analyst forecast changes

- Estimate revisions tend to move in trends (i.e., are not random) and are thus partly predictable

Similar to the “earnings surprise” literature in academic finance, research has shown that investors tend to underreact to the news embedded in analyst forecast revisions — they do not always fully incorporate the changes in profit forecasts into prices immediately.

The other key element is that equity analysts often have incentives or biases that cause them to:

- change their earnings forecasts incrementally (i.e., a series of smaller changes rather than one big change), and

- move in herds (analysts often use similar information sources and come to similar conclusions but do not all act at the same time or to the same degree).

So the basic idea is: revisions affect stock returns when they occur, and potentially a while afterwards, and revisions can be partly predicted based on their persistence (i.e., autocorrelation, or tendency to trend). Those two ideas combined mean that revisions today can be used to forecast future revisions, which impact future returns.

How do we measure estimate revisions?

We use earnings estimate data compiled by Factset for a broad global universe of stocks, currently including over 6000 listings (roughly 40% US listings, 60% rest of world). For most stocks we use the data for consensus earnings per share (i.e., operating EPS), while for most REITs we use Funds From Operations (FFO) per share.

We have studied two key metrics most closely:

Revisions breadth: the net proportion of analysts covering a stock that have raised estimates versus lowered them in the last X days (we normally use X = 100 days). This is “how many estimates are going up or down”.

Revisions magnitude: the percent change in the consensus (mean) earnings estimate over the last X days (we normally use 1 month). This is “how much have estimates gone up or down.”

To account for widely varying volatilities across stocks and control risk, we scale the percent changes in the context of each stock’s trailing 5-year range to produce a percentile score (0 – 100).

Unscaled revisions magnitude is probably the most commonly used metric in research studies, followed by breadth. We generally find breadth to be most important because it is more persistent (predictable), and is naturally a scaled variable (i.e., it is a proportion that must fall between -100% and +100%).

Revisions persistence

A key reason for focusing on the direction of estimate revisions (which way the majority of analysts are moving their estimates) is that it is much more persistent and thus predictable than returns.

We have found that the direction (i.e., positive or negative sign) of revisions breadth for a stock is maintained one month later about 83% of the time (vs ~50% for stock returns).

As noted above, simply knowing the current direction of revisions provides some predictability for the future direction of revisions over the next several months.

Why are revisions persistent?

The reasons that earnings estimate revisions are persistent tend to fall into two broad categories:

- Fundamental business trends

- Analyst behavioral biases/incentives

Many businesses have trends in their underlying sales and profits that persist over multiple quarters or years. These can be driven by many factors related to the company itself (a popular product), the industry (new technology or regulatory changes), and the macroeconomic backdrop (interest rates, taxes, consumer behavior, etc.). Analysts following a company and forecasting its profits will try to take all these factors into account, but the complexity of the task means longer-term forecasting is very difficult and thus a focus on near-term (i.e., next quarter/year) results often dominates, leading to “surprises” when longer-term trends develop.

Analysts working at brokerage firms also have significant incentives and biases related to earnings forecasting. Many rely on access to company management for guidance (or investment banking business), and thus try to avoid having their estimates deviate too far from company guidance. Also, making forecasts that differ sharply from the consensus raises the reputational risk if they are wrong. Thus analysts often act conservatively when changing estimates, moving incrementally rather than more dramatically even when their private views would argue for doing so.

A key point to make here is that even though analysts may have biases or incentives related to their jobs, this does not mean that their estimate revisions are not useful information. Analyst activity does influence stock prices, and does capture useful information about future earnings, and the behavioral biases may even be one reason why estimate indicators are useful for forecasting returns.

Our studies

Our own research indicates that earnings estimate revisions breadth and revisions magnitude are each correlated with future returns over 1-6 month horizons, and reinforce each other when used together. And importantly, stronger revisions are also associated with lower risk (volatility) than weak revisions.

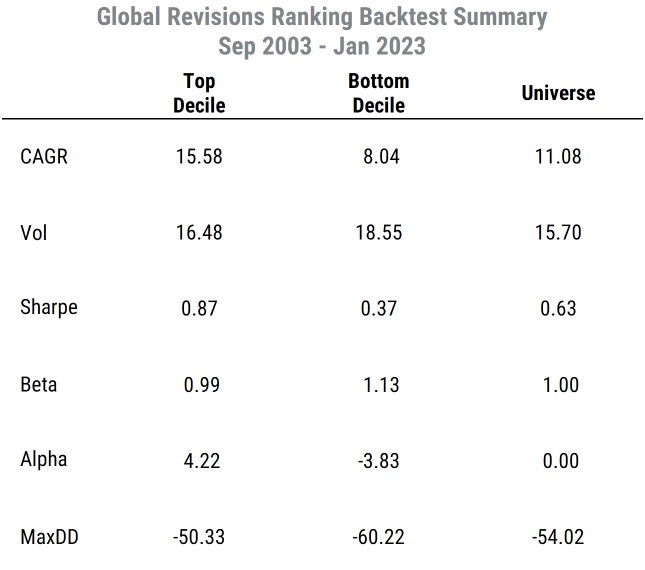

Simple decile backtest results, shown below, reflect the combined ranking of revisions breadth and magnitude for our global stock universe since September 2003, based on monthly rebalancing. Keep in mind that we are looking at relative revisions (i.e., a cross-sectional ranking at each point in time) rather than the absolute breadth/magnitude of revisions.

These results are a quantitative study (backtest) and do not reflect any actual trading or investment strategy. They do not include important considerations such as transactions costs, taxes, liquidity, or other factors. Mill Street Research does not manage client money.

To briefly summarize the statistical results above:

CAGR = Compound Annualized Growth Rate, or annualized total return in local currency.

The top decile of stocks based on estimate revisions would have theoretically returned 15.6% per year on average (before costs) while the bottom decile would have returned 8.0% per year (i.e., a 7.6% annualized return differential), and the equal-weighted global stock universe (benchmark) would have returned 11.1% per year. Thus stocks with the strongest revisions have tended to substantially outperform those with the weakest revisions over the last 19 years, and also outperform the benchmark (all-stock average return).

Vol = Annualized volatility (standard deviation) of returns, a measure of risk

Volatility for top decile revisions stocks was notably lower than that of the bottom decile stocks, and only slightly higher than the overall universe volatility. So stocks with strong revisions do not carry excessively high price volatility risk on average in our work, and are less volatile on average than stocks with weak revisions.

Sharpe = the Sharpe ratio compares the annualized return to the annualized volatility (after subtracting the risk-free interest rate from returns) to give a risk-adjusted return metric.

The top decile has a much higher return/risk (Sharpe) ratio than the bottom decile in our study.

Beta = the average sensitivity of each portfolio to movements in the benchmark, with 1.0 being the benchmark’s beta by definition.

Top decile stocks have had a market beta of about 1.0 on average, while bottom decile stocks have had above-average betas on average and thus bring higher benchmark-relative risk.

Alpha = the annualized excess return of a portfolio versus the benchmark after adjusting for the portfolio’s beta, which is calculated using least-squares regression.

Positive numbers indicate risk-adjusted outperformance, and negative numbers indicate underperformance. The top decile has produced substantial positive alpha in our study, while the bottom decile has produced a similar magnitude of negative alpha.

MaxDD = the maximum percentage drawdown in the hypothetical portfolio returns, meaning the largest decline from an all-time peak to the subsequent trough, another measure of risk.

The top decile had a lower (less severe) maximum drawdown than the bottom decile (and the universe), another indication that stocks with stronger revisions are less risky than those with weak revisions.

A brief comment for the quanty-types in the audience . . .

Some summary tests of statistical significance show that:

1) the difference in returns between top and bottom deciles is significant: the Student’s t-test on the difference in daily portfolio returns shows a t-value of 2.93, indicating a significance level of well under 1% (p=0.003). That is, the odds that the top decile returns and bottom decile returns are actually the same (and therefore that the difference that we see is just random noise) is very low (about 0.3%).

2) comparing actual next-month returns for all 10 deciles with their revisions portfolio deciles to compute a decile-based information coefficient (IC) shows a monthly average IC of 0.23, with a Newey-West adjusted t-statistic of 4.9 (p < 0.001). That is, the statistical odds that the full revisions-based ranking (covering all the deciles, not just the top and bottom) actually has no correlation with future 1-month returns are extremely low (less than 0.1% using the standard assumptions).

Notes about the results

One note about the global stock universe used in the study: to be included, stocks must have had at least $500 million market cap for non-US stocks and $200 million market cap for US-listed stocks, as well as at least 3 analysts reporting estimates and at least $2 million/day average three-month trading value (liquidity). To be ranked, stocks had to have at least two years of valid data. So the stocks included here are all institutionally investable with reasonable analyst coverage, i.e., no micro-caps or poorly-followed stocks are included that might skew the results.

And the historical analysis only includes stocks that were trading at the time (no survivorship bias) and data that would have been available at the time (no look-ahead bias). The results assumed rebalacing on the third business day of each month based on data as of the previous month-end (i.e., a 3-day reporting lag was included).

Again, while these study results are purely hypothetical, they offer good evidence that our measures of estimate revisions are still quite valid to use as part of a quantitative stock selection model. And since the original research paper that provoked the MAER stock selection tool many years ago was published in 1985 by Robert Arnott1 (with many papers confirming the idea thereafter), we can make the case that the potential alpha in revisions indicators has not been fully arbitraged away even after all these years. And the indicators used here were originally constructed in late 2012, so much of the historical data shown here is now “out of sample” data.

As mentioned at the beginning, combining revisions indicators with our own versions of the well-established stock selection factors of price momentum/mean-reversion and valuation improves the results. That is what our cornerstone multi-factor stock selection tool MAER is designed to do. More background on MAER is available here, and interested readers can reach out for more infomation:

1 Arnott, Robert D. “The use and misuse of consensus earnings.” The Journal of Portfolio Management 11.3 (1985): 18-27.