12 January 2022

We often hear the narrative that rising long-term bond yields are harmful to valuations of “long duration” Growth stocks, especially the Technology sector that dominates the Growth style. This has been evident in day-to-day swings in the market recently.

While we understand the concept embedded in discounted cash flow models that higher discount rates depress current equity values more when capitalizing earnings that occur further in the future, we have been skeptical that the discount rate effect in most cases is sufficiently large to dominate changes in growth expectations or investor risk tolerances, at least for the Tech sector. In other words, our view has been that an investor’s bigger concerns when evaluating higher-Growth Technology stocks are the future earnings growth rate and the risk involved, not whether Treasury bonds yield 1.5% versus 2%. Changes in growth expectations and investor risk perceptions will typically have much larger effects on stock prices than moderate changes in Treasury yields, especially when interest rates (and real rates in particular) are at such a historically low level.

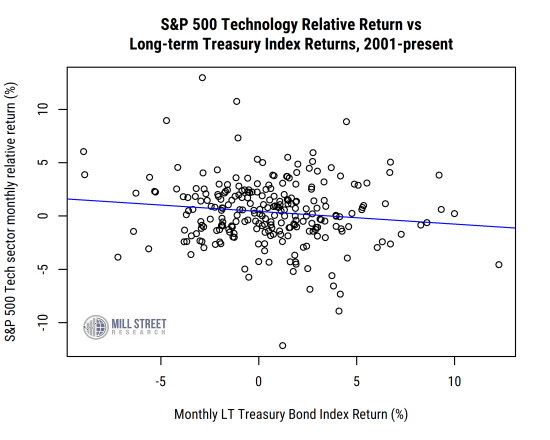

So we performed a relatively simple study to see if there has been a reliable relationship between contemporaneous monthly returns to long-term US Treasury bonds (using the ICE BofA 10+ Year Treasury Total Return Index) and the relative return of the S&P 500 Technology sector, using data since 2001.

The scatter plot below shows the results along with the linear regression line for the data. If the common assumption were true that higher rates (negative bond returns) are bad for Tech stock relative performance and positive bond returns are good, then the regression line should slope upward. In fact, the relationship is fairly weak but if anything the reverse is true: the line slopes downward.

Source: Mill Street Research, Factset

These longer-term results mean that in months when bond yields rose (T-bond returns were negative), Tech stocks actually outperformed more than usual. To put some numbers on it, in months when the long-term Treasury index rose (bond yields fell), the Tech sector had essentially no outperformance on average (3bps per month). In months when bond prices fell (yields rose), Tech outperformed the S&P 500 by 78bps.

The negative statistical relationship is only moderately significant but clearly does not show the decisive positive relationship one would need to see to validate the common worry about bond yields and Tech stock performance on a longer-term basis.

So does that mean we should be more bullish on Technology now, given that bond yields have been rising recently? Not necessarily. First, the relationship noted above is a contemporaneous relationship, meaning it is not using interest rate movements to forecast Tech sector returns, only to explain them. If you believe rates will continue to rise going forward, it suggests Tech should hold up relatively well versus other sectors on an intermediate-term basis.

Stepping back to consider our broader view of Technology, we have been positive on the Technology for some time but have scaled back our overweight recently as Value-oriented sectors like Financials and Energy have looked stronger in our work (based largely on earnings estimate revisions trends, price momentum, and valuation). The Technology sector still has solid earnings trends overall, but not as strong as Financials and Energy, and is relatively expensive versus its own historical norms. We have seen a lot of Growth vs Value rotation over the last year, and expect that will continue, with a potential Value bias. Tech is still our favored area within the Growth style, but faces shorter-term headwinds to relative performance compared to areas that benefit more from rising interest rates (Financials) and high commodity prices (Energy).