5 January 2022

With 2021 now in the history books, earnings reporting season for Q4 and the full year is set to begin soon. Below we update the current consensus earnings outlook for Q4 as well as the coming year for the S&P 500. We also drill into expectations for sector earnings growth for this year.

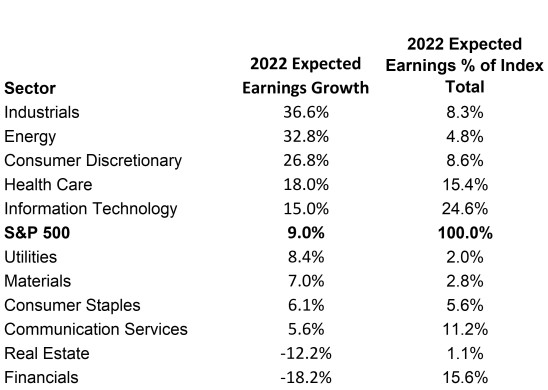

The bottom line, so to speak, is that analysts expect solid but more moderate growth in earnings of about 9%, led by gains in the Industrials and Energy sectors, with Financials and Real Estate the only sectors expected to show declines in earnings this year.

Q4 looks to be another strong quarter, but slower growth after that

For Q4, S&P 500 earnings are expected to be up 32% from a year ago to $50.38 according to S&P, yet another big percentage year-on-year gain. For the calendar year 2021, operating earnings are expected to be $201.86, up 65% from the depressed levels of calendar 2020.

Based on the current 2021 estimate, the S&P 500 ended the year at an estimated P/E of 23.6.

For Q1 2022, the consensus according to S&P is calling for $51.46, which would be 8.5% growth over Q1 of last year but only marginally higher than the Q4 2021 figure. It is clear that the easier year-on-year comparisons with depressed 2020 figures are going away and thus the huge percentage increases seen in the last several quarters will revert to more normal readings.

The current full year estimate for 2022 for the S&P 500 is $220.11, which would be 9% growth over the full year 2021 estimate. The index’s P/E on the 2022 estimate was thus 21.7 as of December 31st.

The 9% growth in earnings expected for 2022 is close to the expected top-line sales (revenue) growth of 7.4% (according to Factset), and in line with economists’ forecasts for nominal GDP growth in the US of 7-8%. This suggests that earnings growth projections do not depend on further significant expansion of profit margins, which are sitting near all-time highs for large-cap US stocks (though they assume margins will remain at high levels rather than contracting).

Notably, earnings estimates for the S&P 500 are still rising, a key factor supporting equity prices during their gains over the last year. However, the pace of increase in the estimates is much more moderate now than during 2021. Our data show that about 62% of S&P 500 companies have more analysts raising estimates than lowering them, so the upward trend in estimates is still fairly broad-based (over the long-run that proportion averages at or slightly below 50%).

Sector estimates show Industrials and Energy with the highest expected growth this year

S&P’s data also allows us to calculate the expected earnings growth and the proportional earnings contribution of each of the 11 GICS sectors toward the overall index earnings . The table below shows the current expectations for each sector. Source: Mill Street Research, Standard & Poor’s

Source: Mill Street Research, Standard & Poor’s

It is little surprise to see that Technology is still by far the largest contributor to overall index earnings, providing nearly a quarter of the total. Health Care and Financials are the next largest contributors at about 15% each, followed by Communication Services at 11%. Real Estate, Utilities, and Materials are the smallest, and each contribute less than 3% of total earnings.

Consensus estimates call for Industrials and Energy to have the biggest gains for calendar 2022, with both expected to show more than 30% increases from 2021 earnings. Consumer Discretionary, Health Care, and Technology are also expected to show solidly double-digit earnings gains. On the negative side, Financials and Real Estate are the only sectors expected to show lower earnings in 2022, while the remaining sectors have growth expectations in the mid-single digits.

Extrapolating broadly from the sector earnings growth expectations, the overall pattern of sector growth estimates implies analysts believe supply chain concerns and COVID will ease (helping Industrials and Consumer Discretionary in particular) but energy prices may stay elevated (helping Energy). Interest rates are expected to rise (hurting Real Estate) along with less Fed support, a potentially flatter yield curve, and more muted growth in mortgage activity (hampering Financials). The dominant Technology sector is expected to grow earnings faster than the overall index, but Communications Services (where firms like Alphabet and Meta reside) is expected to have more modest growth.