9 December 2021

We remain overweight the Energy sector, as analysts continue to raise earnings estimates and the sector is very favorably valued, though the picture has become somewhat more mixed as crude oil prices have been volatile recently. News of the new Omicron variant of COVID-19 and corresponding constraints on international travel have renewed concerns about fuel demand, while OPEC’s decision to go ahead with output increases has reduced the earlier concerns about insufficient supply.

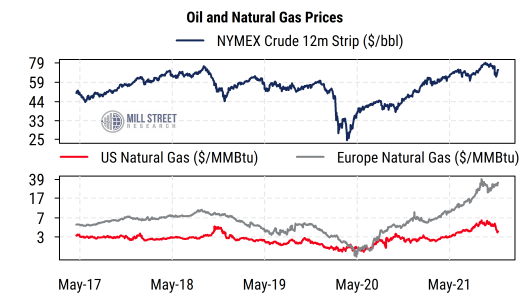

Crude prices and natural gas prices in the US (but not in Europe) have pulled back but remain near the upper end of their multi-year range.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

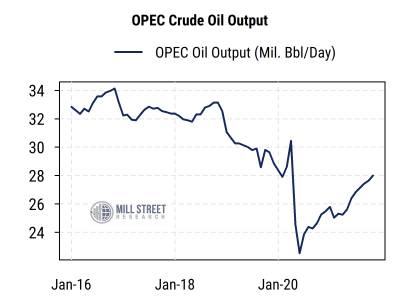

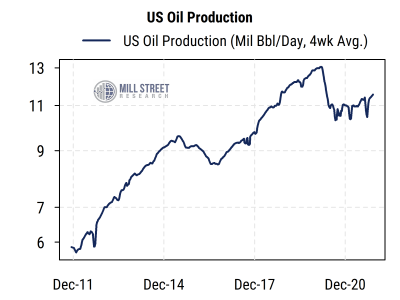

Importantly for energy companies, with prices elevated output has continued to recover from COVID-related declines. The charts below plot the reported output rates for OPEC (top chart) and the US (from the Dept. of Energy). OPEC’s output has moved higher, in line with the group’s stated plans, but remains well below pre-COVID levels as demand has not fully recovered.

In the US, oil production is also rebounding, but like OPEC’s, remains below pre-COVID levels. Companies are weighing the current elevated prices against the costs of restarting closed oil and gas rigs and uncertain longer-term demand trends.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

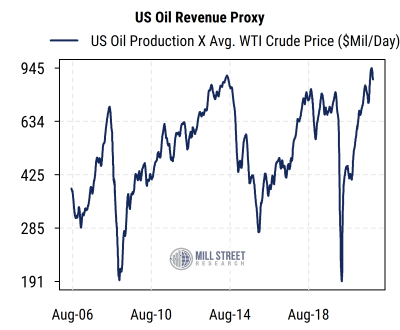

The higher prices for crude compared to much of the last six years have combined with the partial recovery in US output to push our simple US oil revenue proxy (US crude output times average WTI crude price) up to new highs (chart below). That is, top-line revenues for US oil companies are strong even though output is still well below its peak.

Source: Mill Street Research, US Dept. of Energy, Bloomberg

Source: Mill Street Research, US Dept. of Energy, Bloomberg

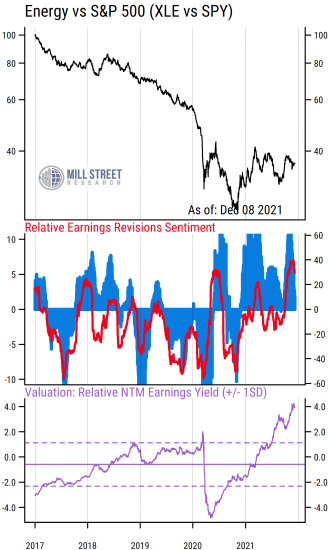

So oil and gas producers (especially the larger integrated firms) still appear to have solid earnings tailwinds. Our aggregated earnings estimate indicators for the S&P 500 Energy sector (middle section, chart below) still show analysts raising estimates in the Energy sector much more than for the overall S&P 500 (red line and blue bars above zero indicate above-average analyst revisions activity).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

Even more dramatic is the extreme valuation level, as the Energy sector’s forward (next 12 month) earnings yield (inverse of P/E ratio) is at its highest (most favorable) level relative to the S&P 500 in many years (purple line in chart). Put in P/E terms, the Energy sector is trading at just 11.6 times earnings expected in the next 12 months, compared to the forward P/E of 21.1 for the overall S&P 500, which is a historically wide valuation gap and follows years of underperformance vs the market (black line in chart).

So while oil price volatility could continue to make the Energy sector a somewhat bumpy ride, valuations suggest a lot of negative news may be priced in, and analysts are still raising earnings forecasts as output levels rebound.