23 September 2021

The primary news from the Fed meeting yesterday was to clarify the likely timing of reducing and then ending the current QE (quantitative easing, or bond buying) program. Fed Chair Powell indicated that (barring any big surprises) the tapering would begin at the next FOMC (Federal Open Market Committee) meeting in early November and aim to be completed (bond buying would end) by the middle of 2022. This would be a somewhat quicker move to end QE than occurred previously, but markets seem prepared for this and thus unlikely to have a “taper tantrum” again.

Powell made clear that he does not view the end of QE as necessarily then immediately leading to the beginning of rate hikes. However, the “dot plot” of interest rate projections of FOMC members (available here) indicated a somewhat earlier “liftoff” from current near-zero rates than the previous (June) projections. This was viewed as somewhat of a hawkish move, but Powell made the point (again) that the dot plot is not a road map and that many things can change over the next year. Also, the regular rotation of FOMC members (and possible new appointments made by the Biden administration) means that some of the current FOMC members will not be serving by the time such rate hikes would be starting, so the composition of the Board and FOMC will make a difference.

The markets took the Fed news well, with stocks gaining and bond yields not moving much. There was some yield curve flattening as 5-year Treasuries rose in yield while 30-year Treasury yields declined, though the 5/30 yield spread has been declining fairly steadily since May. The market’s view is that rate hikes by the Fed in a year or two will not drive up long-term bond yields, thus causing short-term and long-term bond yields to move closer together now.

However, in our view the Fed’s balance sheet (QE) is arguably less important than it was previously, since the banking system currently has plenty of reserves/liquidity. Slowing and then ending the current QE program next year will leave the banking system with plenty of excess reserves, so there should be no meaningful tightening of liquidity conditions. Thus the market’s mild reaction to yesterday’s FOMC meeting is not surprising, as 1) the tapering plans had been telegraphed earlier, with little market concern, and 2) the cumulative effect of the QE since last year has been large and likely is not helping much at this point anyway.

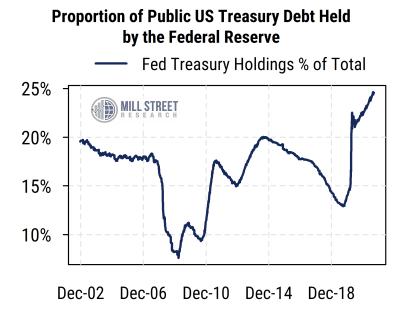

It is also helpful to put the size of the Fed’s balance sheet in context:

- Relative to the US Treasury market it is at a new high (i.e., the Fed owns a record percentage of outstanding Treasuries, first chart below). This means the Fed has even more influence on rates across the curve than in the past.

- Relative to the size of the US equity market, the balance sheet is near the post-2008 average. Periods before 2008 are not comparable (bottom section of second chart below). Thus the size of the Fed’s balance sheet has mostly stayed in line with the growth of stock prices (and corporate earnings) since 2008.

Source: Mill Street Research, Federal Reserve, Factset, Bloomberg

Source: Mill Street Research, Federal Reserve, Factset, Bloomberg

In our view, fiscal policy is arguably more important than the Fed’s balance sheet at this point. So we track the federal deficit as a percentage of equity market value (or GDP) as a proxy for fiscal policy. The deficit/market cap ratio is still elevated but not at a historic extreme (2009 was higher than 2020), as shown in the top section of the second chart above.

Our view is that stimulating demand (fiscal policy) is the key nowadays, not reducing borrowing costs (monetary policy), since interest rates are already so low and banks and other lenders have plenty of money to lend.

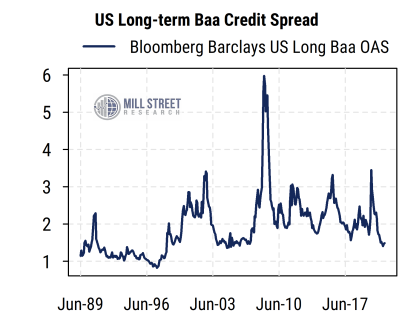

The prospect of Fed tapering is largely well known by now, and credit markets have not reacted. Credit spreads (difference between long-term Baa-rated corporate bonds and corresponding US Treasury yields) are still extremely low, confirming that there is lots of liquidity in the system and investor demand for yield (chart below, showing option-adjusted spreads or OAS).

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

In our view, the biggest impact on credit spreads is the fact that the Fed expanded its powers to buy corporate (and even junk) debt last year. It did not actually end up buying much corporate debt, but the fact that it could caused credit spreads to contract and is likely keeping them low. And we now know the Fed can buy as many bonds as it needs to if things get turbulent.

That is arguably the key for markets: what the Fed CAN do is more important than what the Fed is actually doing right now. Last year basically removed all effective constraints on the Fed’s ability to intervene in an emergency (except for buying stocks directly). Even as Congress has allowed some of the legal backing for emergency Fed interventions to expire, markets assume the Fed would be able to do so again in the future if needed.

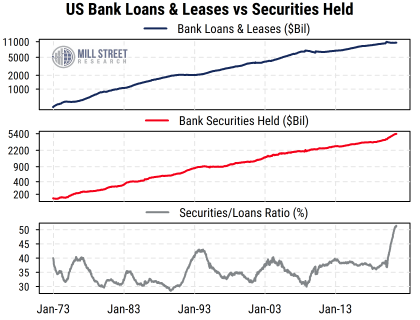

The banking system is oversupplied with reserves now, and loan demand is modest, so banks are having to buy securities with their excess assets rather than make loans. We can see this in the fact that the securities/loan ratio for US banks has risen sharply, now far above all previous peaks historically in the last 50 years (chart below).

Source: Mill Street Research, Federal Reserve

Source: Mill Street Research, Federal Reserve

US banks currently have $4.2 trillion in reserves (and still rising), up from $1.5 trillion in mid-2019 (which turned out to be too low then). This tells us there is a great deal of liquidity in the system, so tapering QE should not cause a problem.

The larger concern would be if/when the Fed actually raises rates, and by how much. While the new dot plot released yesterday suggests that rate hikes could start in late 2022, even then rates will likely not go up much. The latest median dot plot projection for the federal funds rate for year-end 2023 is still at only 1%, and the fed funds futures are somewhat below that level, suggesting the markets see fewer rate hikes than the dot plot implies.

We know that the Fed has been burned by raising rates too quickly in recent cycles, and has seen similar mistakes made by the European Central Bank (ECB) and Bank of Japan (BOJ) in the past. Also, the new average inflation targeting (AIT) framework the Fed has adopted gives them scope to keep rates lower than otherwise, especially if COVID remains a global health issue well into next year. Our view remains that longer-term trends in demographics, debt, and productivity will likely keep inflation from accelerating on a longer-term basis once the COVID-related supply shocks have passed.

For the stock market as well as the economy, the Fed is moving from being a large tailwind to a more neutral influence, but is unlikely to be a major headwind any time soon. If fiscal support moderates (or temporarily goes in reverse if the US government shuts down again), then secular Growth areas of the stock market (Technology, etc.) will likely take on leadership again. We have already been seeing a moderation in the cyclical leadership in our earnings estimate revisions metrics (as noted here recently), and weakness in China is an incremental headwind for global growth.

The Fed will always be important, and they can still make policy mistakes that cause problems for the markets and economy, but such mistakes do not look likely to occur soon in our view. So far, they have managed the market’s expectations with regard to reducing QE better than they did previously, and should thus avoid another “taper tantrum” like the one that occurred in 2013. We are more focused on fiscal policy (Congress) than monetary policy these days as the bigger macro driver for the economy and markets.