16 September 2021

For some time we have noted that traditional Cyclical and Value sectors have had much stronger earnings estimate revisions activity (“fundamental momentum”) than Growth or Defensive sectors. That has been changing recently as cyclical sector estimates are less strong than before, and Growth and Defensive are holding up better. Thus we have recently been looking more favorably on certain Growth or Defensive sectors and neutralizing exposure to Cyclical/Value areas.

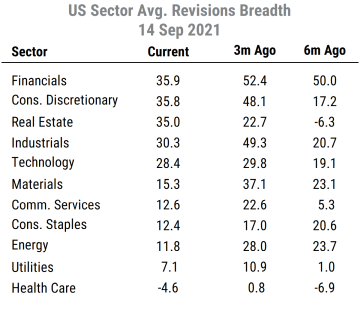

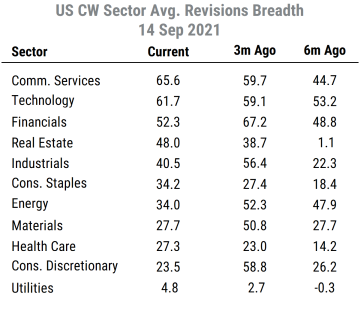

The tables below update our US sector revisions breadth readings, based on our ~2300 stock US universe (revisions breadth = net % of analysts raising earnings estimates vs lowering estimates). The left table shows the calculations that give equal weight to each stock’s revisions breadth in a sector, and the right table shows figures that weight each stock’s breadth by its proportional market cap (like cap-weighted market indices do).

Source: Mill Street Research, Factset

A few key points jump out:

- Most sectors still have positive net revisions breadth, meaning more analysts have been raising estimates than lowering them. So almost none are outright weak, and earnings estimates generally continue to rise at a solid pace.

- The sectors showing improvement versus three months ago on a cap-weighted basis are all Growth or Defensive sectors: Communication Services, Technology, Real Estate, Consumer Staples, Health Care, Utilities. The rest (Value/Cyclical areas) have weakened from earlier high levels, some significantly.

- On an equal-weighted basis, the only sector to see improvement versus three months ago is Real Estate. The biggest decliners have been Materials, Industrials, Energy, and Financials – all Value/Cyclical sectors. Technology was little changed.

- There are notable differences in the equal-weighted versus cap-weighted (CW) breadth readings, especially in Consumer Discretionary, Technology, and Communication Services. This is due to the influence of a few mega-cap stocks that dominate the cap-weighted readings in those sectors, such as Amazon.com (AMZN), Apple (AAPL), and Alphabet (GOOGL). Overall, large-caps (that heavily influence the cap-weighted data) have stronger revisions activity than mid/small-caps.

These trends suggest that Cyclical/Value sectors no longer have the commanding lead in fundamental momentum that they did earlier in the year, which is consistent with solid but more moderate economic growth and concerns about the renewed impacts of the Delta variant of COVID on both demand and supply chains. These fundamental trends align with relative performance of Growth and certain Defensive areas versus Value or Cyclical areas recently, especially when viewed on a cap-weighted basis, and suggest there could be more to come. Our preferences along these lines are for Technology, Communication Services, and Real Estate. For those seeking Value exposure, Financials looks most attractive among sectors.