By some measures, the US housing market has been extremely strong. Sales of new homes are up more than 30% year-on-year, as many people are seeking to leave big city centers and buy single-family homes in the suburbs.

However, the chart below shows some of the extreme and offsetting influences on the housing and mortgage markets right now.

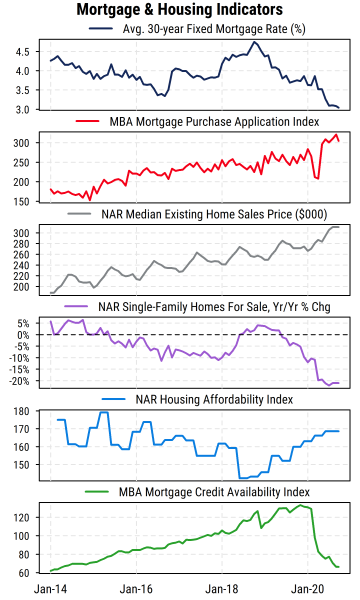

Mortgage rates have plunged to all-time lows (top section in the chart), reducing the payments needed to buy a house with a mortgage. This has led to a surge in mortgage purchase applications (second section).

While higher demand has pushed prices for houses up to a new high ($310K median for existing homes, third section), that demand is also running into the corresponding fact that many people who already have houses do not want to sell right now. So the supply of houses on the market has plunged (fourth section).

Lower mortgage rates have helped improve the housing affordability index (fifth section), but rising prices have now limited the improvement. Affordability is much better than in 2018 and similar to its level in 2014-16.

We cannot forget, though, that the economy is still very weak and employment is still far below pre-COVID levels. This means that there are likely fewer credit-worthy borrowers, and banks have tightened conditions for loans of all types significantly this year.

Indeed, the last section of the chart shows the Mortgage Bankers Association Mortgage Credit Availability Index. It measures availability of mortgage loans based on underwriting standards used by lenders. Higher readings indicate greater availability of mortgages. The plunge in the index this year reflects the dramatic tightening of lending standards for mortgages (e.g. requiring higher credit scores and income standards, lower loan-to-value, etc.). So while many people are applying for mortgages, a greater number are also likely not being approved and actually getting the loans. Houses are popular and appear affordable IF you can get a mortgage (or don’t need one).