Inflation expectations have been a topic of growing interest thanks to the extraordinary fiscal and monetary support in place for much of the last year, most recently the huge $1.9 trillion American Rescue Plan that is currently sending checks out to millions of Americans.

All of this new spending by the federal government, along with the economic recovery permitted by the rollout of COVID-19 vaccines, is provoking more discussion about whether demand for goods and services will outpace the economy’s ability to produce them and push prices higher.

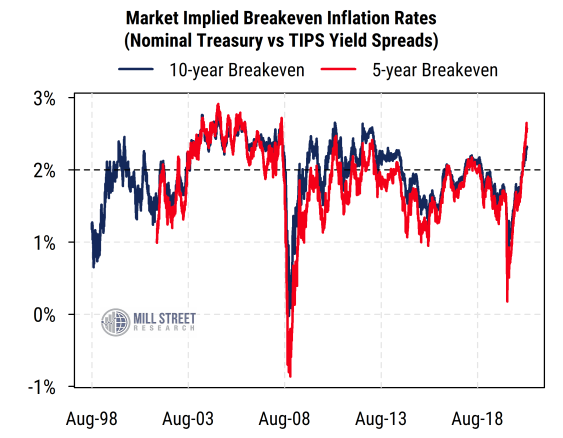

While we have previously discussed why we do not think inflation will be a major problem in the next few years, investors in the Treasury market appear to have raised their forecasts for future inflation, at least in the near-term. This is reflected in the “breakeven rate”, which is the difference between the yield on nominal Treasury bonds and that of the corresponding TIPS (Treasury Inflation Protected Security) bond. TIPS provide a “real” interest rate (currently negative) plus whatever the rate of inflation is over the bond’s duration. The difference between nominal and TIPS yields indicates the level of inflation that would produce the same return to holding either type of bond after accounting for inflation.

The chart below shows the breakeven rates for five-year and 10-year maturities, and we see that the five-year inflation expectations in particular have risen sharply recently, now back to levels around 2.5% seen after the last two recessions. The 10-year breakeven rate has risen less, as investors appear to expect a temporary jump in inflation that will subsequently ease. Both figures are roughly in line with the Fed’s stated inflation target, and thus are unlikely to provoke a tightening response at this point.

Source: Mill Street Research, Bloomberg

Reported inflation, as measured by the Personal Consumption Expenditure (PCE) Price Index (the Fed’s preferred measure), has remained low thus far. Year-on-year comparisons will soon be skewed by the price drops around this time last year when the economy buckled under the weight of COVID and the associated limits on activity. Overall, however, there are thus far few signs of significant overall inflation in the reported data.

When we look under the surface of the inflation data, however, we find that there are a lot of significant changes going on among the various components, which are thus far mostly offsetting each other. This is not unusual around recessions, and certainly consistent with the extreme and unusual kind of shock that COVID-19 has caused in the economy.

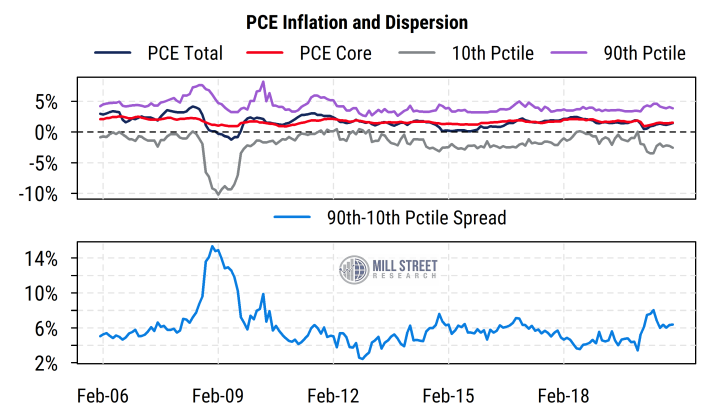

The Federal Reserve Bank of San Francisco publishes metrics that capture the dispersion and amount of underlying change in the inflation rates of the various categories of goods and services measured in the PCE data. The charts below show the increased levels of “rotation” under the surface of the muted headline PCE inflation measures.

The first chart below shows the last 15 years of data on the PCE headline (total, dark blue line) and core (excluding food and energy, red line) inflation rates along with measures of the dispersion among the 100+ granular subcomponents of the PCE inflation data. It shows the inflation rate for the 90th and 10th percentile subcomponents of the PCE price index and below that the spread between the 90th and 10th percentiles as a measure of the cross-sectional dispersion or variation of inflation rates among products at any given time. We can see that dispersion in inflation rates among the categories of PCE components has widened significantly recently to 6-7%, up from readings closer to 4% for much of the last several years.

Also notable is the fact that even the subcomponents with the highest inflation rates (the 90th percentile, purple line) have price gains of only about 4%, marking a fairly modest upper bound on inflation pressures so far.

Source: Mill Street Research, Federal Reserve Bank of San Francisco

Source: Mill Street Research, Federal Reserve Bank of San Francisco

With some prices falling substantially, the current inflation spread (90th vs 10th percentile) is among the widest in the last decade, and it quantifies and corroborates the intuition that the supply and demand impacts of the COVID-driven recession and recovery have led to more divergent outcomes for different industries (some hurt badly, some benefiting strongly). The inflation spread widened even more dramatically around 2008, driven by enormous volatility at that time in energy prices in particular, and there was less direct fiscal stimulus support in that recession than the current one. This analysis helps make the point that the gap between winners and losers seen in the stock market has a fundamental driver visible in the inflation data.

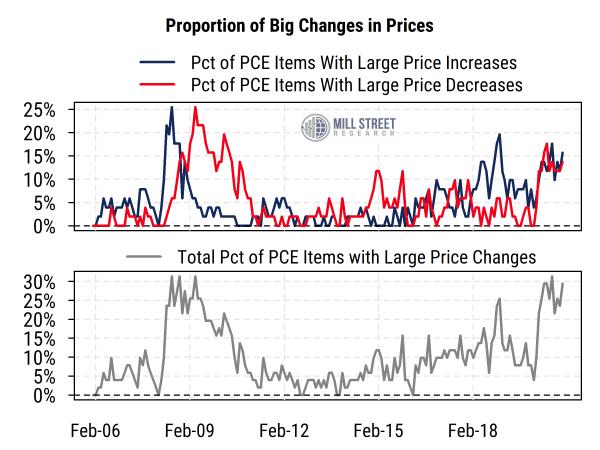

The final chart below plots another way of looking at the underlying divergences beneath the surface of the headline inflation data. The same San Francisco Fed data set also calculates the percentage of PCE price index subcomponents that have had large changes in their 12-month inflation rates relative to their previous five-year averages (“large” meaning two standard deviations from the five year average). Industries that have seen their inflation rates lurch upward would be captured in the blue line, showing the percentage of all PCE components with large upward movements in inflation, while those facing big downward changes would be captured in the red line.

Source: Mill Street Research, Federal Reserve Bank of San Francisco

Source: Mill Street Research, Federal Reserve Bank of San Francisco

The grey line below plots the sum of the two series to provide a measure of how many industries have seen major shifts in their respective inflation trends. Here we see that 25-30% of industries have recently had major shifts (up or down) in pricing power relative to their longer-term trends, much higher than the usual 5-15% readings for most of the last decade.

We also see that current readings are at similar levels to those seen around the 2008 recession, though with a slightly different pattern: in 2008, there was initially a spike in price increases, then a spike in price decreases, while this year has seen concurrent but less extreme spikes in both series as demand and supply had to simultaneously adapt to COVID’s impact on activity.

The implication is that some industries that may have had weak pricing power pre-COVID now have stronger price trends, while others that had higher industry-level inflation are now under more pricing pressure. While there are always a few such industries at any given time, there are many more right now.

These data help provide some further fundamental corroboration for the rotation in stock market industry trends and wide gaps between winners and losers, even in an environment of continued low headline inflation rates.