The news of Joe Biden winning the US presidency in November has now been joined by news that the US Senate will very likely be under the most narrow control of the Democratic party, along with a narrow majority in the House of Representatives. These developments have led investors to expect more fiscal stimulus and other support than would have been expected under continued Republican control of the Executive branch and Senate.

One of the consensus views that has emerged is that the higher level of expected fiscal support along with the aggressive monetary support from the Federal Reserve (zero policy rates and ongoing bond buying programs, or QE) will provoke accelerating inflation. The view is amplified because the recent stimulus legislation, and expected future fiscal support, have included direct payments to individuals ($600 stimulus checks, possibly becoming larger in the future) along with resumption of enhanced federal unemployment benefits (though smaller than the initial CARES Act amounts), among other programs. The view is that these sorts of direct payments are more likely to be spent on consumer goods and services (to a greater degree than spending on things like health care, infrastructure, or defense), and thus that consumer prices will be forced up by the increased demand.

We are often asked about our view on inflation, particularly in light of these unusual policy conditions. So what is our take? We think the supply side of the equation needs to be considered along with the demand-oriented arguments. Our view is that the economy has a lot of slack still left in it, and thus has capacity to meet increased demand without broad-scale acceleration in inflation. We certainly expect an increase in demand due to the stimulus relative to what it would have been otherwise, but do not expect it to be so extreme that it will push the economy past its potential output limits and produce substantial sustained inflation as a result. This does not mean relative prices will not change, as indeed they already have, but there will continue to be offsetting impacts that keep the overall inflation rate from accelerating.

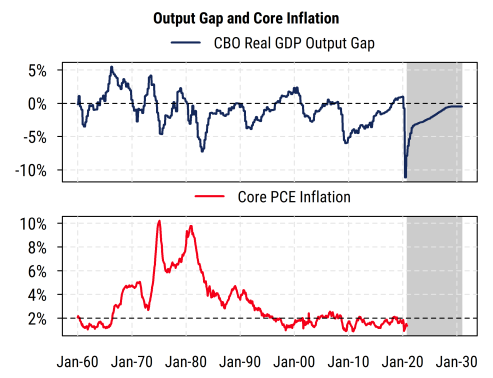

The chart below shows the historical and projected estimates from the US Congressional Budget Office (CBO) of the “output gap”, or difference between actual real economic output and the estimated potential output the economy could produce without causing accelerating inflation. The grey shaded area indicates forecasted future data from the CBO. At the end of 2020, the economy is operating more than 6% below its estimated capacity, and even after a sharp rebound that is expected in 2021, the economy is still expected to be more than 3% below its potential at the end of this year. The CBO’s projections do not anticipate that the economy will exceed its capacity over the 10-year forecasting horizon (i.e., until 2030 at least). All such long-run forecasts should be viewed with skepticism, but the broad message makes sense given the long-run secular trends in the economy and the lasting damage caused by COVID-19. The inflation data shown in the lower section (using the Fed’s preferred measure of the Personal Consumption Expenditures core price index, i.e., excluding food and energy) corroborate our view that accelerating inflation is very unlikely when the economy is operating below its potential, as has been the case for most of the last 40 years.

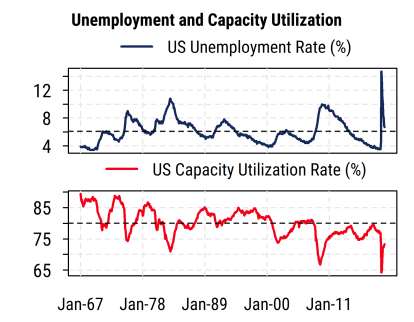

To better understand some of the key drivers of the output gap that argue that there is plenty of spare capacity in the economy, we can review the chart below. It shows the unemployment rate as a measure of labor capacity and the capacity utilization rate as a measure of manufacturing capacity. The unemployment rate remains above the long-run average (dashed line), and far from the low points near 4% where inflation (wage pressure) is more likely to become a concern. The reported (U-3) unemployment rate is also likely a conservative estimate of labor market slack, as it does not measure people who have given up seeking work but would do so under better conditions.

The capacity utilization rate reported monthly by the Federal Reserve also shows a wide gap between the current reading (73%) and the historical average (80%), much less the historical peak levels that would be associated with accelerating inflation. Indeed, the fact that capacity utilization has shown lower peaks and lower troughs over the last three decades helps explain why consumer inflation has also been declining and low for much of that time. If demand can be met by current capacity, broad-based inflation is much less likely.

Long-term structural trends in demographics, debt, and productivity in the US and much of the developed world are generally disinflationary. So it would take an unusually large and persistent effort by fiscal policy makers to generate high inflation in this environment. Naturally, that could happen, but history and current politics suggest it is unlikely, and in our view any increase in consumer demand from additional stimulus can be readily met without broad-based inflation given the slack in the economy.