9 June 2021

One of the biggest topics among investors recently has been inflation, particularly after the May Consumer Price Index (CPI) and Producer Price Index (PPI) reports (reflecting April data) that showed big monthly jumps in headline inflation: 0.8% for headline CPI and 0.6% for headline PPI. And the “core” rates that exclude food and energy were actually slightly higher than the headline rates in April.

There may be more: current consensus expectations for this month’s report are for another significant monthly increase in the CPI and PPI: +0.4% is the current estimate for both.

The current year-on-year inflation rates for CPI and PPI are known to be skewed due to base effects from the COVID-driven weakness in April 2020, but nonetheless reached levels not seen in many years: 4.2% for the headline CPI and 6.2% for the headline PPI.

While these current figures have raised concerns among some economists and investors, it is worth keeping in mind that inflation is a messy thing to try to estimate even in the best of times, and these are clearly not the best of times for measuring price changes accurately. So we can step back and look at the longer-term trends in inflation data, particularly since the data suggest that the recent jump in inflation is so far only enough to get back to the underlying trend in prices that had been in place pre-COVID.

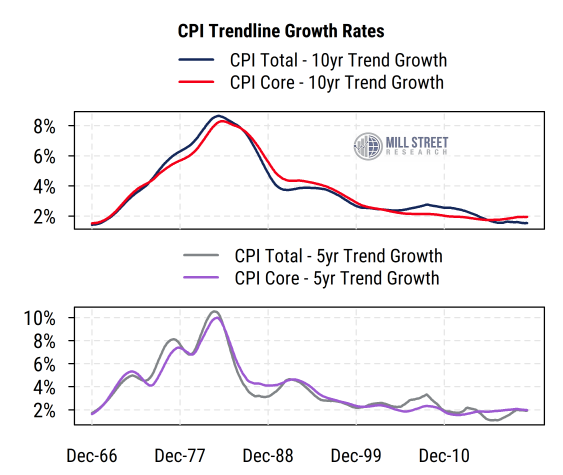

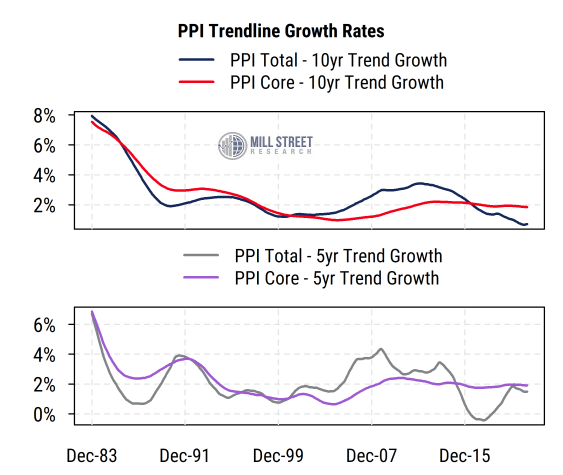

The charts below show our calculation of the 10-year and 5-year trendline growth rates of the CPI and PPI, using both the headline (“all items”) indices and the core (excluding food and energy) indices.

Using a trendline growth rate, based on regression analysis (the slope of the “best fit” line through the series, on a rolling basis), rather than the more common start-to-end percentage growth rate avoids the distortions in the calculation that can occur around peaks and troughs, so it is often used to provide a more stable growth rate estimate.

Source: Mill Street Research, Bureau of Labor Statistics

Source: Mill Street Research, Bureau of Labor Statistics

The message is essentially the same regardless of the inflation series or time window used: the trend in inflation remains quite moderate near 2%, with no clear signs of meaningful acceleration, even after incorporating the latest jumps in CPI and PPI.

While this does not mean that inflation will not accelerate significantly in the future, it reminds us that it takes time to build up real inflation pressures (as in the 1960s-70s), and that has not occurred so far. Thus far, inflation is mostly catching up to its existing low trend growth rate, which is near the Fed’s 2% target. Current macro conditions are extremely unusual, combining post-COVID reopening with historic stimulus efforts and supply chain disruptions. Most of these factors are temporary and will likely wash out in the coming 12 months or so, in our view. We continue to expect moderate overall inflation in the longer-term.