Our measures of aggregated earnings estimate revisions trends have shown some of their most dramatic movements on record this year, and now may be looking extended.

After reaching historically extreme negative readings in April/May amid the initial COVID-19 lockdowns, earnings estimate revisions activity has now lurched back up to extremely positive readings. Better-than-expected Q2 earnings reports and the effects of massive monetary and fiscal stimulus are now finally reflected in analyst earnings forecasts. However, with fiscal stimulus weakening (and little imminent sign of movement toward new stimulus) and no meaningful further scope for interest rate cuts, the “snap-back” in earnings estimate activity could soon drop off.

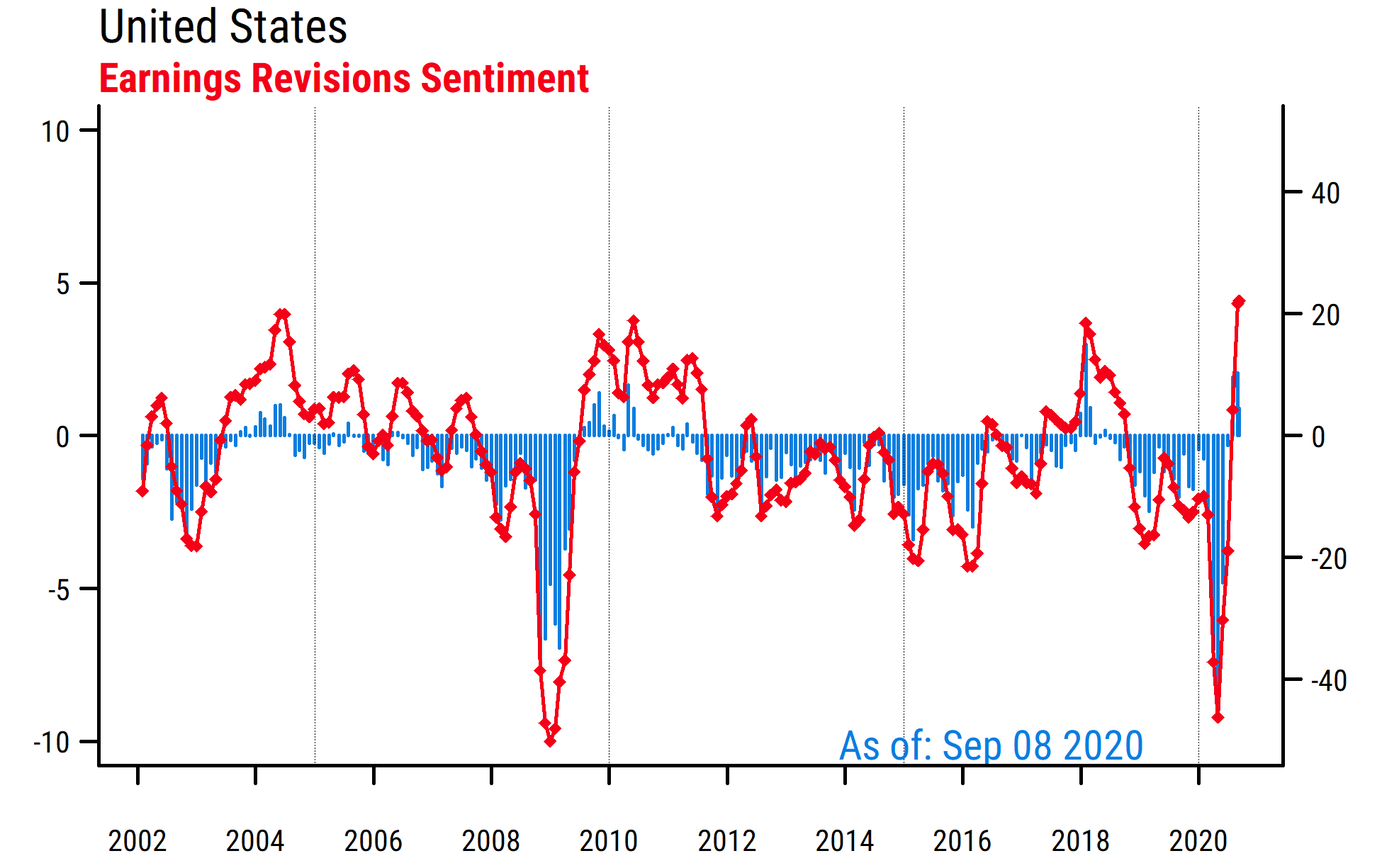

The first chart below shows our measure of aggregated analyst earnings estimate revision activity in the US, for our broad universe of over 2000 stocks (equally-weighted) on a longer-term time frame. The data are month-end values except for the latest data point. The red line represents the “breadth” of estimate revisions, meaning the aggregate net proportion of positive versus negative revisions (changes) to forward 12-month earnings estimates over the prior three months (i.e., number of analysts who have raised earnings forecasts minus the number who have reduced forecasts, as a percentage of the total number of analysts for each stock, scale right). The blue bars represent the “magnitude” of the month-on-month changes in forward 12-month forecasts, i.e., the average percentage change in earnings forecasts from a month ago (scale left).

We can see that the low point in April matched (or exceeded) the extremes seen in the 2008 Great Financial Crisis (GFC) period, which is not surprising given that the drop-off in economic activity this year was greater than in the GFC. However, the combined fiscal and monetary stimulus recently produced in response was also greater than any previous post-WWII period, and so revisions metrics have shown a faster and more extreme rebound than at any previous point in our data. Stock prices appear to have moved ahead of aggregate estimate revisions, raising the question of whether this apparent good news for earnings is already priced in.

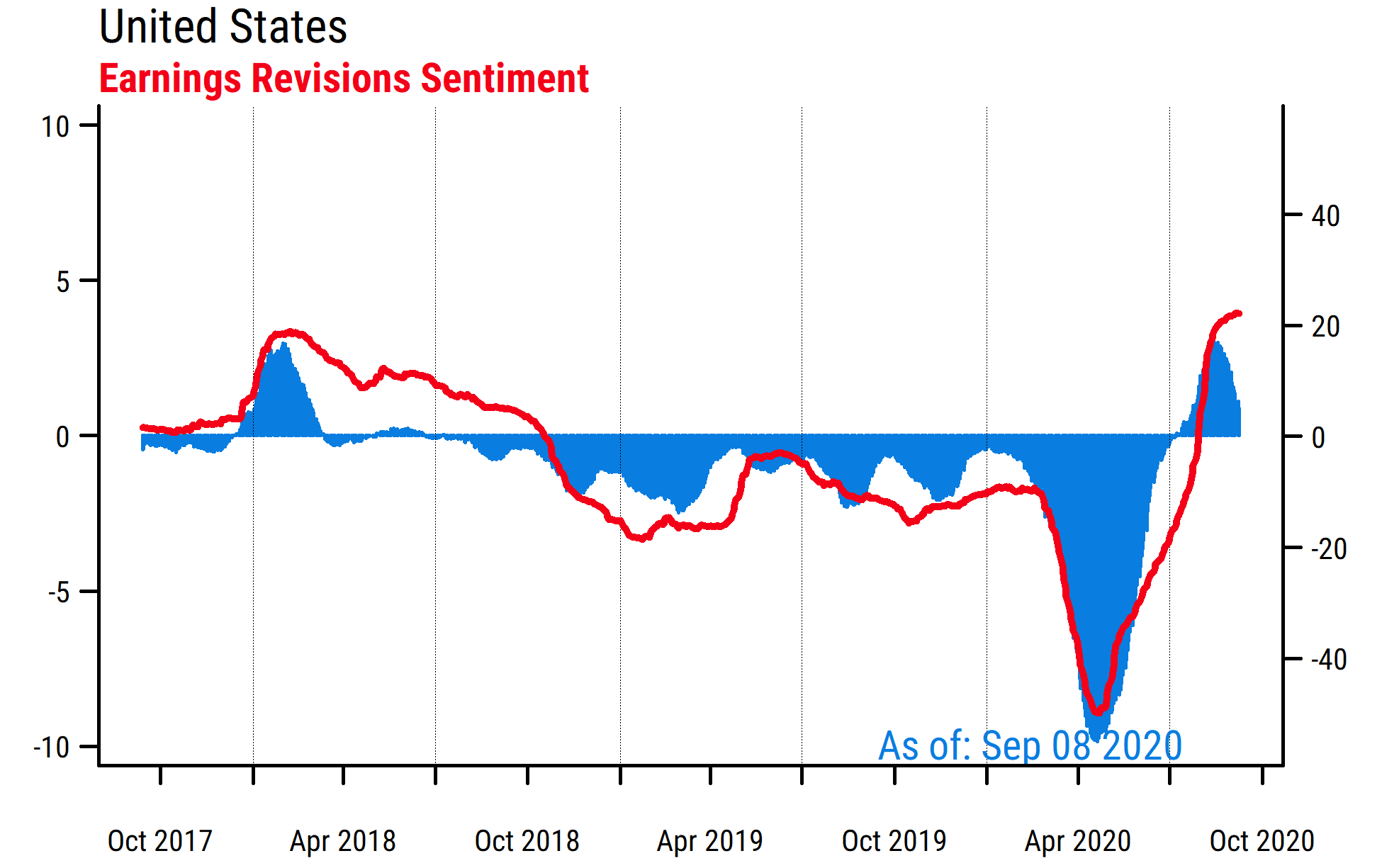

Perhaps more concerning is the risk that revisions (i.e., analyst sentiment) have reached highly optimistic readings now and may already be starting to revert. The chart below is calculated identically to the one above, but plots the daily figures (rather than monthly) over the last three years. Here we can see that the blue bars are already coming down from their latest peak, suggesting that the upward momentum of earnings estimate revisions may be fading now that Q2 earnings reports are over. The breadth series (red line) is based on revisions over the last three months, so it encompasses a full calendar quarter and is thus more stable. If revisions breadth starts to turn down (as it did after the tax-cut surge in early 2018) alongside current elevated valuations for equities, then the recent signs of higher stock market volatility could persist into Q4.