31 March 2022

Our indicators of analyst earnings estimates revisions in the US highlight a key theme: revisions for large-cap (and mid-cap) stocks have held up much better recently than those of small-cap stocks.

While the proportion of analysts raising their earnings estimates relative to those cutting estimates has been declining ever since its extremely high peak in the middle of last year, the difference between large-cap and small-cap revisions has favored large-caps, and has shifted further in favor of large-caps most recently.

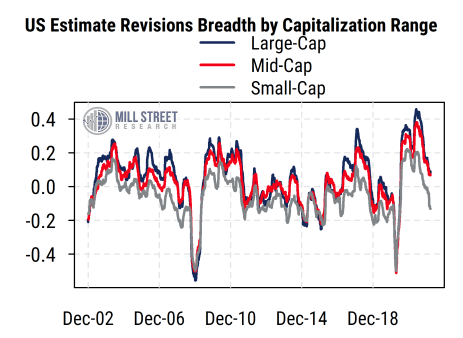

In the charts below, we break our broad US universe (currently about 2500 stocks) into large-, mid-, and small-cap groups. We do this by ranking stocks by market cap each month and using the top 20% by market cap as large-caps, the next 30% as mid-caps, and the bottom 50% as small-caps. Within each size category, the earnings estimate revisions figures are equally-weighted for each stock.

The first chart below shows the average revisions breadth reading for each of the three categories over time. Revisions breadth is our term for the net proportion of analysts raising estimates minus those lowering estimates for a stock, as a percentage of the total number of analysts. For each stock, we use the latest estimate revision that has occurred within the previous 100 calendar days (just over one calendar quarter).

Readings above zero indicate that there are more upward than downward revisions on average. Keep in mind that revisions to estimates can be negative (more down than up) even when earnings themselves are still growing in absolute terms (just growing a slower pace than previously expected).

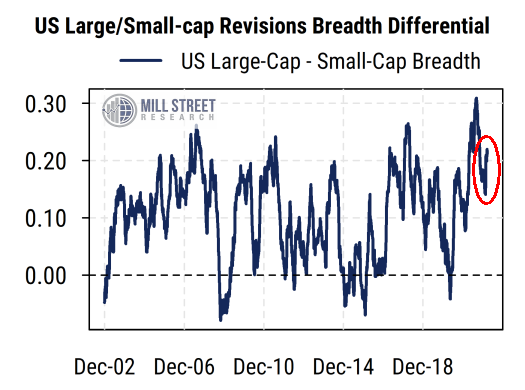

The second chart shows the difference between the large-cap revisions breadth and the small-cap revisions breadth over time, to better visualize the relative aspect. Here, readings above zero mean that large-cap stocks have better (more positive, or less negative) revisions than small-cap stocks on average.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The charts clearly show that while large-caps have historically had stronger revisions breadth than small-caps, the differential now is much wider than usual and has been expanding in favor of large-caps in recent weeks.

Why are large-cap revisions doing better than those of small-caps? In general, there is likely a greater tendency for analysts covering smaller companies to start with a more optimistic earnings estimate for more distant earnings (e.g. two years from now) and then trim it down to “reality” as the time approaches. This is a common pattern for all companies, but larger companies tend to have more information and management guidance available as well as more predictable growth rates, and thus analysts are less likely to make extreme initial long-term projections about earnings.

There are also differences in the composition of the large- versus small-cap universes, both in terms of fundamentals like profitability as well as sector weightings. One difference that stands out in our data is the much larger proportion of Health Care stocks in the small-cap universe (about 25% of the universe currently) than in the large-cap universe (where Health Care stocks make up about 12% of the constituents). Smaller Health Care companies are more likely to have small or negative earnings, and many of them have been hurt by the impacts of COVID than the larger, more diversified Health Care companies have.

More recently, there may be an argument that larger companies are better able to respond to inflation pressures and to rising interest rates than smaller companies. Higher bonds yields and wider credit spreads along with ongoing supply chain issues may be hurting smaller companies more than the large companies which have better access to capital and more flexibility in sourcing, etc.

Overall, revisions activity is now roughly in line with the long-run historical average, with large-caps slightly above average while small-caps are at or below average. The differential continues to favor large-caps, and particularly when the overall pace of earnings growth is slowing after the post-COVID surge in 2020/21.

We have favored large-caps over small-caps in our recommended asset allocation views since September, and continue to do so. While we base that view primarily on our cyclical economic and market indicators, we also keep in mind these relative bottom-up fundamental trends which are currently aligned with our macro view.