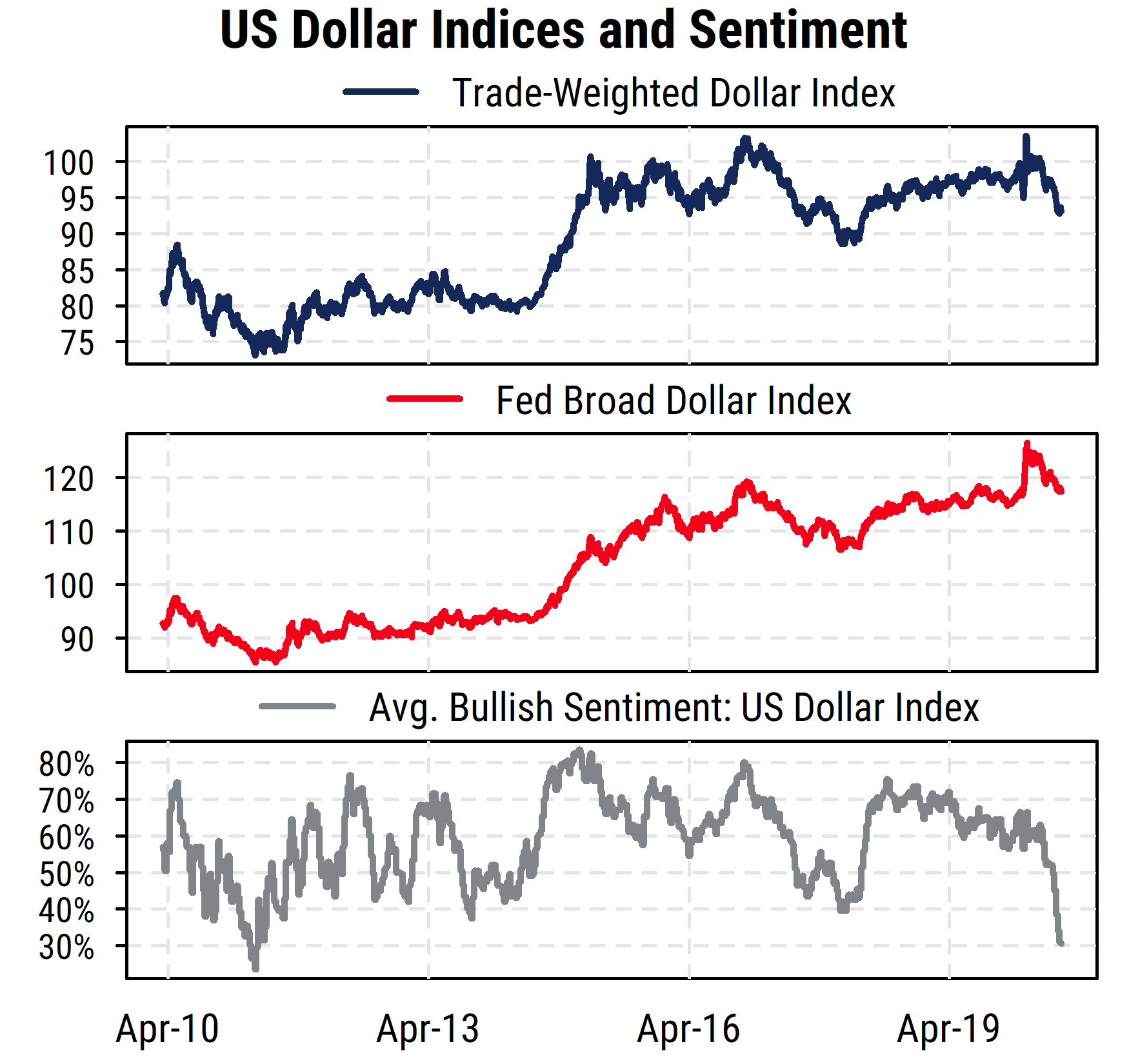

One of the most notable trends in markets recently has been the weakness in the US dollar. After a choppy strengthening trend since early 2018 (as the Fed was tightening policy), the US Dollar Index surged in the immediate aftermath of COVID-19’s arrival in March. Since then, however, as monetary and fiscal stimulus engulfed markets and investor risk appetite returned, the dollar has been weakening versus a number of other currencies. Indeed, the dollar’s weakness has accelerated recently, and the Dollar Index has reached its lowest levels since May 2018.

The latest movement is in large part attributable to strength in the euro, which has a big (58%) weight in the Dollar Index among the six major developed market currencies in the index. However, the recent decline can also be seen to a lesser degree in the Fed’s Broad Dollar index that encompasses a wider range of currencies. Certainly the prospect of US interest rates across most of the yield curve being near zero for the foreseeable future makes the dollar less attractive now versus other currencies.

However, we are now seeing signs that bearishness towards the US dollar has become extreme, and such sentiment is likely correlated with broader trends in investor risk appetite.

When reviewing the data on sentiment toward the dollar, one key metric that has jumped out at us is shown in the chart below. It plots an average of the proportion of market commentators (strategists, newsletter writers, etc.) who are bullish on the US dollar as reported by Consensus Inc. and Market Vane (services which track investor sentiment). We can see that bullishness on the dollar has now plunged to its lowest levels in nearly a decade. And while sentiment can remain bullish or bearish for some time, we can clearly see where the heavy consensus view on the dollar is right now. It is thus more likely that the dollar’s decline is in its later stages rather than a newly developing trend.

Since the US dollar behaves as a “risk-off” currency (along with the Japanese yen and Swiss franc), selling the dollar is often a sign of risk-on behavior, and consistent with recent risk-on activity in equity and debt markets. Bullish sentiment toward stocks and bonds is also back to pre-COVID levels, so the dollar sentiment readings are consistent with those trends as well. With monetary and fiscal stimulus in the US fading now, the surge in the supply of US dollars is also likely to ease, and the US economy and inflation are likely to slow without additional stimulus. A reversal of the current lopsided sentiment trends would potentially be bullish for the US dollar and bearish for equities, though the precise timing of any such change is always a challenge.