The growth of online shopping has been well-established for years now, but the pandemic has prompted an acceleration in that trend, which continues to be felt in relative stock returns.

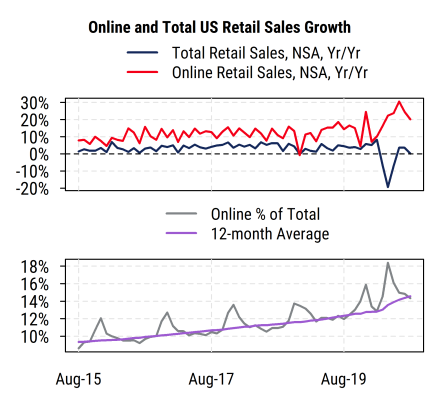

The chart below shows the year-on-year growth rates of total US retail sales and online retail sales (non-store retailers) over the last five years (based on monthly retail sales reports from the US Census Bureau). We can see that online sales have been growing significantly faster than total sales the entire time, and most notably, are now near their highest growth rate (20%+) even as total retail sales dropped sharply earlier this year and are currently roughly unchanged from year-ago levels (indicating that non-online sales are down from a year ago).

The bottom section of the chart plots online sales as a percentage of the total. While there are seasonal swings in the monthly data, the 12-month average shows a clear upward trend over the last five years, with a distinct acceleration most recently. In the last five years, online sales have grown from less than 10% of all sales to almost 15% (on a 12-month basis), and briefly surged to 18% amid the lockdowns earlier in the year.

The reasons for the shift to online shopping during the pandemic are mostly obvious, as the ability to shop in physical stores was sharply limited in many areas due to lockdowns and worries about the coronavirus. This is, however, another example of a trend that was in place well before COVID-19 arrived, and has simply accelerated. While store-based retailers may take back a bit of share near-term, the longer-term trend towards online shopping (at least for things that can be bought online) and entertainment services like video games looks likely to continue.

What about the impact on stock prices? The year-to-date returns to some industries in the broad S&P 1500 Supercomposite Index that are closely tied to these trends make the point (example constituents are shown for reference in parentheses — these are not recommendations to buy or sell). For comparison, the S&P 1500 index has returned 8.6% for the year-to-date.

- Internet & Direct Marketing Retail (Amazon, EBay, Etsy): +71%

- Air Freight & Logistics (FedEx, UPS): +54%

- Interactive Home Entertainment (Activision Blizzard, Electronic Arts, Take-Two Interactive): +32%

One clear loser has been commercial real estate, especially the REITs (real estate investment trusts) that own retail space (malls, etc.) that rely on store-based retailers. Department stores make up many of those, and have been hurt badly, as have some of the companies that make the products sold in stores, particularly fashion clothing and accessories.

- All REITs: -9%

- Retail REITs (Simon Property Group, Regency Centers, National Retail Properties): -40%

- Department stores (Macy’s, Nordstrom, Kohl’s): -62%

- Apparel & Accessories (VF Corp., Ralph Lauren, UnderArmour, Movado): -28%

The impact of the shift to online buying is ongoing, as is the impact on company earnings forecasts and stock returns. While in-person shopping will always be there, it seems that there is scope for further shifts toward online shopping, and finding the winners and losers from it will likely remain important even after the impact of COVID-19 has eased.