Among the various asset allocation decisions for which we provide guidance to clients is whether to favor small-caps or large-caps (i.e., the “size” factor) within the US equity market. In our view, small-caps do not reliably outperform large-caps consistently over time (as some models and studies might suggest), and instead view the “size premium” (outperformance of small-caps) more as a cyclical phenomenon that tends to show up under certain macroeconomic and market conditions.

While there are many potential conditions that might affect small-cap/large-cap relative performance, much of our work is oriented around the idea that small-caps give the best “bang for the buck” in the periods just before and through the early stages of a new economic or market cycle. That is, recessionary troughs in the economy and equity market set up the conditions for future small-cap outperformance, as smaller companies tend to benefit most from the re-acceleration of economic growth that typically occurs after recessions. This is also when monetary and fiscal stimulus tend to be strongest. In these scenarios, small-caps have typically underperformed before and during the preceding recession/bear market and become out of favor and potentially undervalued. Conversely, the later stages of an economic cycle and the early stages of a recession or bear market tend to be unfavorable for the riskier and more economically sensitive small-caps.

Looking at conditions now, there is certainly evidence that a recessionary trough has occurred or is in process, and both monetary and fiscal stimulus have been very aggressive. This would potentially argue for favoring small-caps over large-caps, and indeed small-cap relative returns have stabilized after a sustained period of significant outperformance by large-caps since mid-2018 (and arguably longer). However, it may be worth an extra dose of caution before making heavy overweight allocations to small-caps on an intermediate-term (6-12 month) basis. This is not only due to the unusual nature of the current cycle, but also more specifically to the extremely elevated relative risk still apparent in the volatility of small-caps versus large-caps.

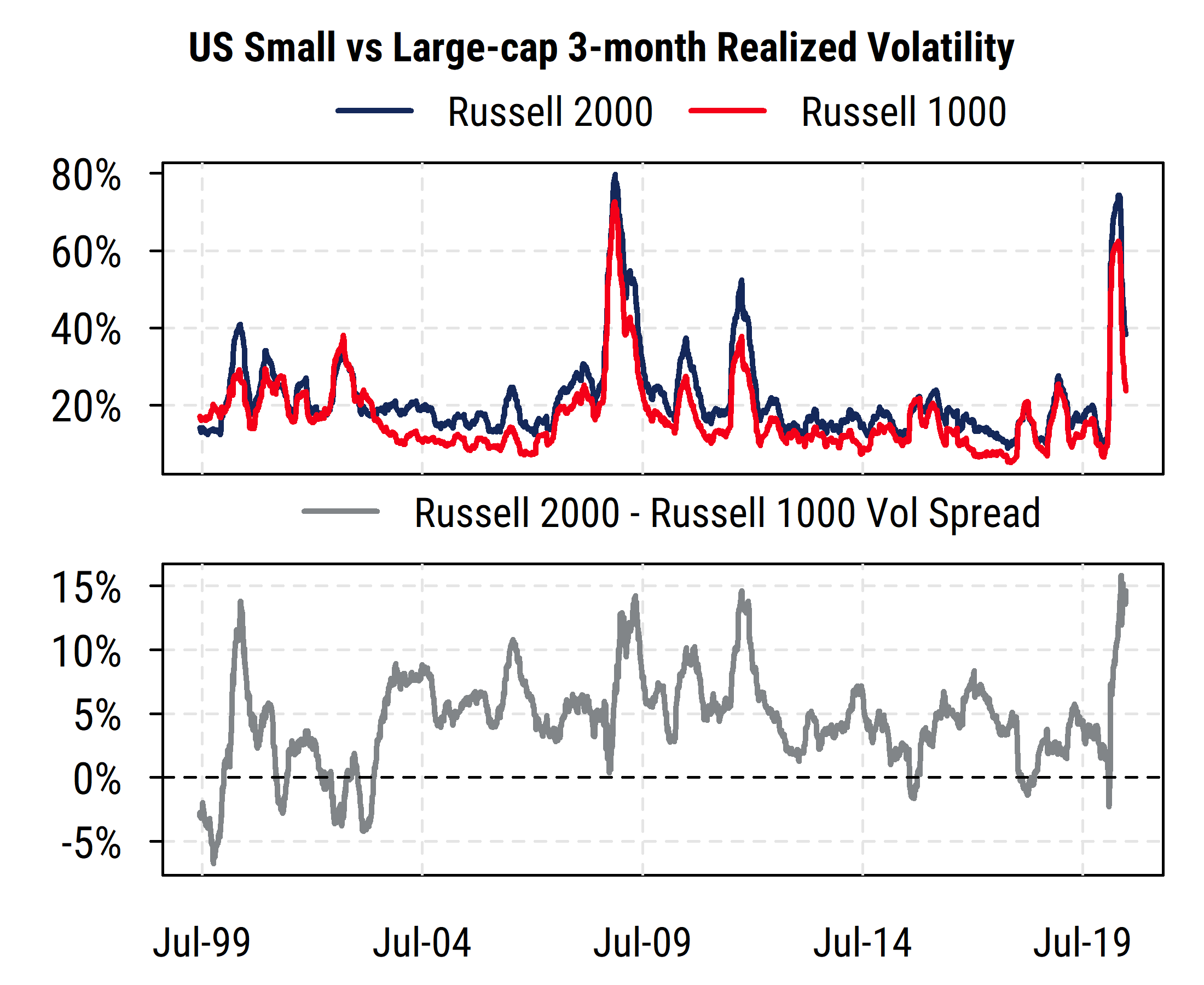

Using the Russell 2000 Index to measure returns for US small-caps and the Russell 1000 Index for large-caps, the chart below shows the rolling three-month annualized volatility of daily returns for both indices over the last 20 years (small-caps in blue, large-caps in red) in the top section, and the difference between them in the bottom section.

A few things jump out: first, volatility for all equities surged to extreme levels earlier this year, matched only by the Great Financial Crisis in the last 20 years, and has been declining rapidly thanks to the Federal Reserve’s extraordinary interventions. And second, the difference between small-cap and large-cap volatility has remained near historic extremes even as volatility has declined for both size categories.

As shown in the bottom section of the chart, small-caps are almost always more volatile than large-caps (i.e., the volatility spread is usually above zero), with a historical average of about 4.5%. However, the latest readings on the volatility spread of over 14% are the highest in the last 20 years. That is, while large-cap volatility has dropped to a (still elevated) level of just under 24% (equal to average daily index movements of about 1.5%), the small-cap index volatility has only managed to decline to 38% so far (equal to average daily movements of about 2.4%). This is still far above the normal level of volatility for small-caps historically of about 22%.

The bottom line is quite straightforward: even after sharp rallies in equities and lower market volatility in general, owning small-caps remains much riskier on a price volatility basis than owning large-caps. So if expected returns must be commensurate with expected risk, then a decision to allocate heavily to small-caps requires either 1) an unusually high excess return expectation, or 2) an expectation of drastically lower small-cap volatility soon.

Given the economic backdrop and the reliance on government stimulus as well as the relative fundamentals of small-caps versus large-caps (a possible topic for another post), it may take a little while longer to have confidence that small-cap excess returns will be sufficient to compensate for their unusually high extra risk relative to large-caps.