In financial markets, it seems like “everything” is going up recently. Stocks, bonds, precious metals, even Bitcoin. Perhaps that should not be surprising given the huge amount of liquidity being produced by global central banks in addition to the fiscal stimulus earlier this year. That tends to have the effect of pushing asset prices up generally.

But when we look at relative returns of some key assets, it looks more like the “risk on” trend has not really gone anywhere since early June. That is, owning the riskier option within various asset classes has not generated excess returns to compensate for that extra risk since the recent peak in risk about June 8th.

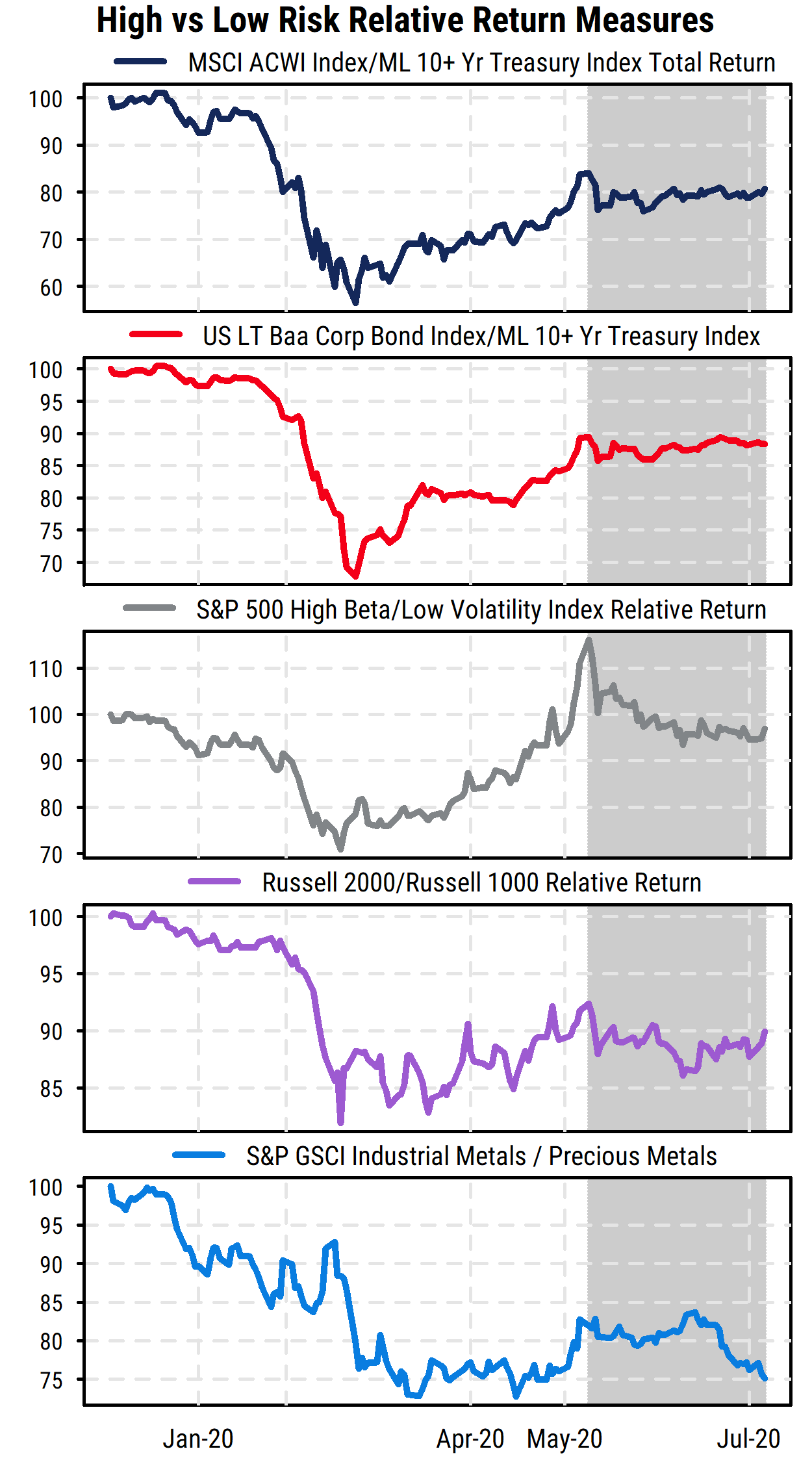

As shown in the chart below, buyers of risk in many areas have not been rewarded for about two months now (shaded area since June 8th). Brief comments on each section of the chart are below it.

This could be a natural consolidation after a surge in return to risk after the late-March lows, or a sign that the impact of stimulus, and stimulus itself, is fading. Many prices/valuations are back near pre-COVID levels even while the economy and earnings are still far weaker than they were in January. Uncertainty about additional fiscal stimulus, now that much of it has expired or been spent, and worries about the continued aggressive spread of COVID-19 in the US are potentially countering the positive hopes for vaccine developments and ongoing central bank support.

We will be watching these returns closely for indications of whether investors are getting properly “paid” for taking on additional risk.

- Top section: Global stocks, measured by the MSCI All-Country World Index (ACWI) have performed no better than long-term US Treasury bonds since early June, and are still far behind bonds on a year-to-date basis.

- 2nd section: Similarly, within the fixed income market, long-term Baa-rated US corporate bonds have done no better than long-term US Treasuries since early June (despite the ongoing support from the Federal Reserve), and remain well behind Treasuries for the year-to-date.

- 3rd section: High-beta stocks in the S&P 500 have lagged low-volatility stocks in the index since early June, even as the S&P 500 itself has moved somewhat higher.

- 4th section: US small-caps have lagged large-caps since early June, and small-caps remain significantly more volatile.

- Bottom section: Among commodities, industrial metals (copper, aluminum, zinc, etc.) that are used in manufacturing are typically a measure of global growth that rise when the economy is improving (“risk on”). Precious metals are more often preferred as an inflation or currency hedge (“risk off”). So while both industrial and precious metals prices have individually risen significantly recently, industrial metals prices have lagged those of precious metals since June.