20 July 2022

Tracking analyst earnings estimate revisions activity (i.e., are estimates rising or falling, and by how much?) is a key feature of our research. With earnings season underway, we can check in on how revisions activity looks across the 11 US sectors, where we find, among other things, a big divergence between the commodity-related sectors of Energy and Materials.

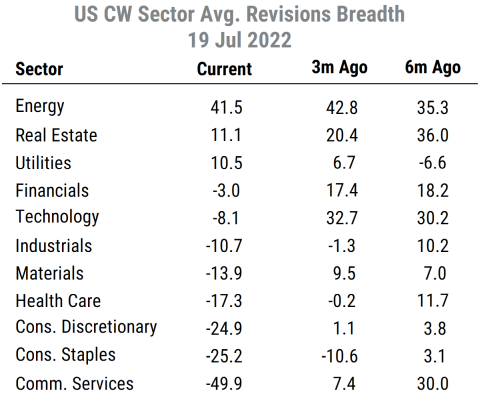

Below is an updated table of revisions activity by sector. It reflects “revisions breadth”, which is the net proportion of analysts who have raised earnings estimates in the last three months minus the number of who have reduced estimates. For any individual stock, revisions breadth can range from +100% (all analysts raising estimates) to -100% (all analysts cutting estimates), with 0% indicating a balance between positive and negative revisions to earnings forecasts.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

The data in the table are capitalization-weighted (CW) averages of the revisions breadth for the stocks within each GICS sector in our 2000+ stock US universe (i.e., it gives more weight to larger companies). It shows the current readings along with the figures from three months ago and six months ago for comparison.

Looking at the current readings, we can see three general groups of sectors:

- Three sectors have outright positive revisions breadth: Energy, Real Estate, and Utilities

- Three sectors have mildly negative revisions breadth, in line with the overall US average right now: Financials, Technology, and Industrials

- Five sectors have substantially negative revisions breadth and thus have the weakest fundamental momentum right now: Communication Services, Consumer Staples, Consumer Discretionary, Health Care, and Materials

When compared to the values three months ago, we note that:

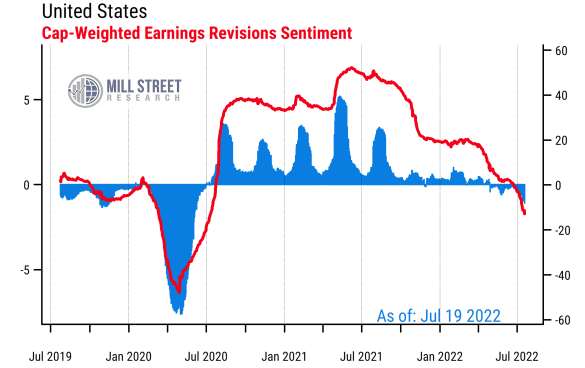

- Most sectors have seen substantial declines in revisions breadth in recent months – the cap-weighted average of revisions in the US has been falling and is now moderately net negative for the first time since 2020 (chart below). Note that this is not unusual historically, as analysts tend to start off with optimistic longer-term forecasts and then trim them down as time goes on (the high readings in late 2020 and 2021 reflect a very unusual period for analyst activity).

- The only sector with higher revisions breadth now than three months ago is Utilities, while Energy is essentially the same.

- Communication Services (dominated by Alphabet and Meta Platforms) has seen the biggest drop (from 7.4% to -49.9%), followed by Technology, Consumer Discretionary, and Materials.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

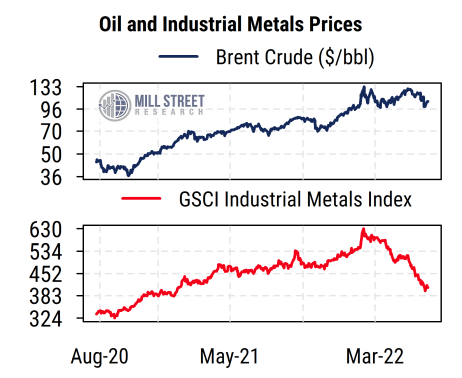

With inflation and commodity prices being a key focus this year, we have been watching the revisions trends for the Energy and Materials sectors closely. Energy has been stronger than Materials for some time, but both had very strong revisions in the May-June period when prices for many commodities had surged. Since then, however, commodity prices have diverged, especially between oil and industrial metals (copper, aluminum, nickel, zinc, etc.). Oil prices have pulled back moderately in the last month or so, but industrial metals prices (which actually peaked in March) have plunged to 15-month lows recently (chart below). Precious metals prices (not shown) have also dropped to near two-year lows lately.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

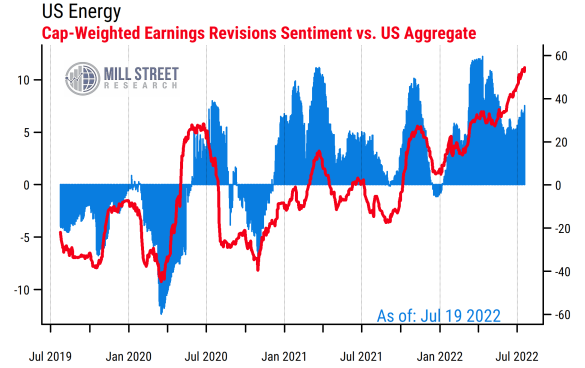

This commodity price divergence has quickly become visible in earnings estimates between Energy and and Materials. While overall estimate revisions in the US have weakened (particularly for larger-caps lately), those of the Energy sector have held up, meaning that on a relative basis (Energy vs the US average, chart below), Energy’s revisions are even stronger now and making new highs.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

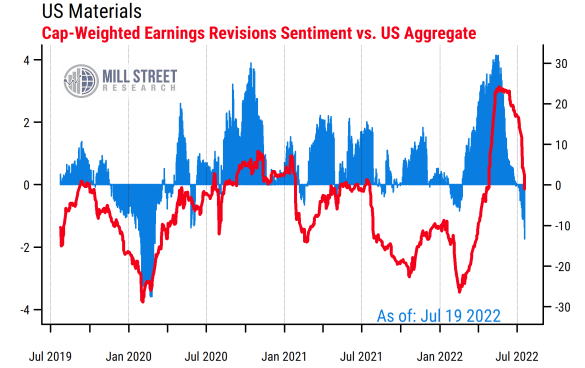

The Materials sector, by contrast, has seen an abrupt and dramatic reversal in its relative revisions breadth, going from far above average to slightly below average now (and still falling) while the average relative percent change in Materials sector estimates (represented by the blue bars in the chart below) have turned decidedly negative (i.e., estimates have been cut by larger percentages in Materials than for the US market as a whole).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

So we can no longer say that “commodity sectors have stronger revisions”, we now have to narrow it to “Energy stocks have strong revisions”, and potentially adjust sector allocations accordingly.

And the improvement in revisions for Utilities stocks may be in part tied to inflation-driven pricing power (utilities have a lot of fixed costs, so higher electricity and natural gas prices can improve margins) and growing demand for electricity and natural gas.

Overall, the revisions picture shows analysts becoming more cautious about earnings amid a slowing economy and tighter monetary and fiscal policy. The rapidly changing inflation/commodity trends have provoked divergences in revisions for the inflation-sensitive sectors, with Energy remaining the top dog and Utilities improving, while Materials loses its earnings support.