10 February 2022

Earnings estimates in the US continue to rise overall, helped by the continued solid economic backdrop, but the pace has eased from last year’s extraordinarily positive levels and divergences among sectors are more visible now.

Part of our sector analysis includes monitoring the aggregate earnings estimate revisions trends for the 11 GICS sectors as well as the more granular industries (we track 62 in the US currently). One of the key metrics is what we call “revisions breadth”, which is the net proportion of analysts covering a stock who have most recently raised their earnings forecasts versus those who have lowered estimates. Thus breadth readings can theoretically range from +100% (if all analysts are raising estimates) to -100% (if all analysts are reducing estimates). Thus higher is better on revisions breadth as it indicates the fundamental news is broadly improving within a sector.

We take the breadth figures for each stock and average them within each sector to get an aggregate reading on each sector’s “fundamental momentum” based on the direction of movement of earnings estimates. We can calculate the average either by giving every stock in the sector equal weight, or by weighting them based on their market capitalizations to produce cap-weighted (CW) revisions breadth readings. Cap-weighting naturally gives more weight to the largest stocks, and is consistent with how most major market indices are constructed, with the potential drawback that the results can be more volatile and influenced by a small handful of stocks at times.

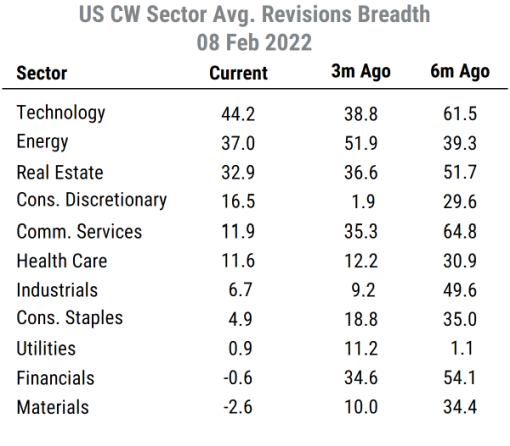

The table below shows the sector cap-weighted revisions breadth readings currently as well as three months and six months ago.

Source: Mill Street Research

Source: Mill Street Research

Some key points we can draw from this table:

- First, we can see that there is a wide range of readings across sectors, from +44% to -2%. This reflects the divergences in fundamentals across sectors that is more evident now than it was for much of last year when almost all sectors had strong revisions activity (i.e., six months ago nearly every sector had very high readings of +30% or higher, ranging up to +65%).

- Second, all sectors have lower readings than they did six months ago (some more so than others). This reflects the moderation of earnings revisions activity as the extraordinary fiscal and monetary stimulus efforts are being withdrawn and analysts’ forecasts have “caught up” to the level of earnings companies are generating now.

- Third, we can see three sectors that stand out well ahead of the rest: Technology, Energy, and Real Estate have very strong revisions breadth readings above 30%, while all others are 16% or less. Three sectors are now near or slightly below zero: Materials, Financials, and Utilities.

- Fourth, we can compare current readings to those of three months ago and see where there has been improvement or deterioration. Technology and Consumer Discretionary are the only two sectors to have higher revisions breadth now than three months ago. The biggest drop has been in Financials (from +34.6% to -0.6%), as some mega-cap Financials disappointed in their latest earnings reports and caused analysts to reduce estimates. Communication Services has weakened substantially as well, led by weakness in heavyweight Meta (FB).

Overall, the revisions trends still have a cyclical bias, but less so than before and are heavily influenced by developments with COVID, inflation, supply chain, and interest rates. Even amid a recent pullback in stock prices, large-cap Tech companies have mostly maintained strong earnings trends, and are typically less sensitive to the economic cycle, energy costs, or interest rates (e.g., leaders AAPL and MSFT most recently reported strong results, while NVDA has had nearly 100% positive revisions for months).

Energy is benefiting from continued high crude oil and natural gas prices, as OPEC and domestic producers have been conservative about increasing production so far, keeping it just below the growth in demand. Real Estate is benefiting from people returning to offices and stores as well as things like warehouse space for online retailers.

Utilities, by contrast, have to pay higher prices for fuel without necessarily being able to raise their own regulated prices right away. Consumer Staples stocks got a big boost when everyone was staying at home, but now that tailwind has eased and supply chain and inflation pressures are weighing on some areas of the sector.

While not the only driver of our views, these sector revisions trends are a key component of our sector allocation recommendations to clients. Consistent with these metrics, we have been overweight Technology, Energy, Real Estate, and Consumer Discretionary in our client allocation recommendations recently. We have been underweight Materials and Utilities, and just recently moved to neutral from overweight in Financials as its indicators have weakened. We remain underweight in Consumer Staples, Utilities, Industrials, and Communication Services, and now neutral on Health Care.

In future posts we will highlight some of the leading constituents of the sectors and their revisions trends.