17 June 2021

In recent months, two of our strongest US sector allocation views have been to overweight Financials and underweight Health Care. A key feature of our sector work is that we often look at sector indicators on a “pairs” basis, i.e., the relative return, earnings momentum, and valuation of one sector versus another (as opposed to comparing sectors only to an overall benchmark like the S&P 500). This allows us to see the underlying relative performance drivers more clearly.

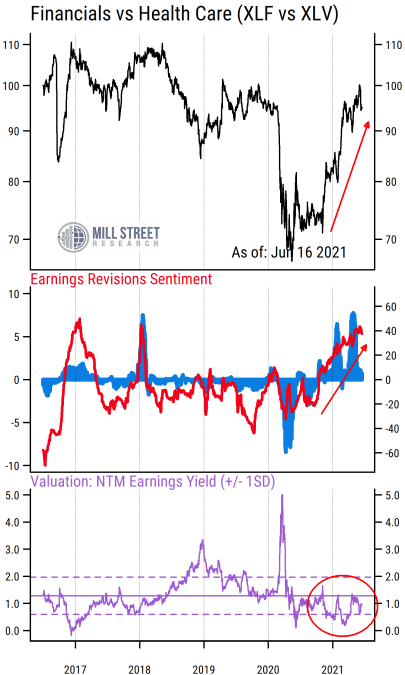

The chart below shows some of the key relative sector indicators we track for S&P 500 Financials (ETF ticker symbol XLF) relative to Health Care (ETF ticker symbol XLV).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

We can see a few things in this chart:

- The top section shows that Financials tended to underperform Health Care for much of the period from 2017-2020, with periodic rebounds in relative performance. Starting late last year, Financials began to outperform dramatically and has recovered all of its 2020 underperformance versus Health Care.

- The middle section shows our earnings estimate revisions indicators, aggregated on a cap-weighted basis for each ETF and shown as a spread (differential). Readings below zero on the red line (revisions breadth) and the blue bars (revisions magnitude) indicate Financials having weaker earnings estimate activity than Health Care, i.e., analysts tending to be more optimistic about Health Care earnings trends than Financials earnings trends (we often call this “fundamental momentum”). Readings above zero indicate Financials outperforming Health Care on a fundamental earnings momentum basis.

- We see that the return underperformance by Financials in 2017-2020 was accompanied by correspondingly weaker earnings activity, and the recent surge in Financials relative performance has clearly been supported by an equally large surge in relative fundamental momentum. Analysts have been raising estimates much more broadly and by larger amounts in Financials than they are in Health Care, and this is still the case. As a result, we are inclined to stick with our preference for Financials over Health Care.

- The bottom section shows the relative valuation for Financials versus Health Care, based on the relative forward earnings yield for each sector. The forward earnings yield is the consensus aggregate earnings estimated for the next 12 months (NTM) relative to the price for the sector (ETF), and thus the inverse of the traditional P/E ratio. A higher reading on the valuation spread (purple line) means Financials is cheaper than Health Care, and lower readings indicate better relative valuations for Health Care.

The Financials sector has almost always been cheaper than Health Care, as all the readings on the valuation spread are positive and the five-year average (solid horizontal line) is well above zero. This is very much as expected given that Financials is typically a Value sector with lower perceived growth potential and more cyclicality than the less-cyclical, Growth oriented Health Care sector.

Recently, the relative valuation has been hovering near its longer-term average, just slightly in favor of Health Care. However, the more notable result is that relative valuation has not meaningfully weakened for Financials even after a huge surge in relative performance. Normally, outperformance of the magnitude seen since November 2020 would cause relative valuations to deteriorate sharply (i.e., Financials would be much more expensive versus Health Care). But because earnings have also been much stronger in Financials than in Health Care recently, the relative performance has not caused valuations for Financials to get worse – they have largely held steady. So Financials is not outperforming Health Care simply as a result of “multiple expansion”, i.e., being awarded a higher relative valuation by investors. It is being driven by underlying earnings growth trends – trends that are still in place currently.

This sector “pair” analysis of Financials versus Health Care also partly captures the broader Value versus Growth trends in recent years. The underperformance of Value sectors (like Financials) relative to Growth sectors (like Health Care, or Technology) in the years up to November 2020, along with the powerful macro tailwinds from stimulus and re-opening from COVID, suggests that the fundamentals may stay in favor of cyclical, Value-oriented sectors for a while longer before a sustained rotation toward Growth or Defensive sectors appears. Thus we maintain our preference for Financials relative to Health Care among US sectors.