Within the broad Technology sector, there are often significant divergences among the various industries. A key intra-sector industry relationship that many investors use as a touchstone is the relative performance of Semiconductors versus Software.

These two industries capture different parts of the Technology ecosystem. Due to their widespread use in so many devices and products, the Semiconductors and Semiconductor Equipment industry reflects demand for hardware, both within Technology (servers, PCs, phones) and in other sectors (e.g. autos), and thus tends to be much more cyclical. Software tends to be much more stable, with more recurring revenue, and nowadays is closer to a service-type industry. There is much less chance of major “shortages” or “oversupply” of software of the kind that semiconductor makers must often deal with.

So even though software and semiconductors are complementary products (each requires the other), it is not hard to see that they can often have significantly different fundamentals and relative returns on an intermediate-term basis.

Our indicators currently show a growing shift in favor of Semiconductors over Software, both in fundamental earnings trends and relative returns. This is a reversal of the trend seen in the 2017-2019 period, when Semis lagged Software, and much of 2020 when relative performance was mixed.

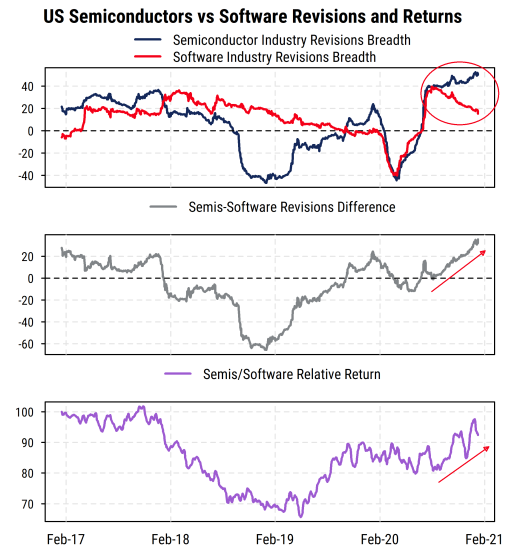

The chart below shows the strong relationship between relative earnings estimate revisions activity in the two industries and their relative returns. The data are drawn from our broad US stock universe of about 2300 stocks (roughly, all US stocks with at least $200 million market cap and three analysts reporting estimates), and the constituents of each industry are equal-weighted in both the revisions and return series. The return series uses a five-day moving average to show the trends more clearly. Earnings estimate revisions breadth measures the average net proportion of analysts raising versus lowering estimates for each stock. Readings above zero mean more analysts raising estimates than lowering them on average.

We see that Semiconductor revisions breadth began losing its relative strength versus Software back in 2017, and continued through early 2019. At that point, Semiconductor revisions started to recover while Software continued a slow deterioration, allowing the relative revisions spread (middle section) to turn up from very negative (i.e., pro-Software) readings. That spread turned positive (favoring Semiconductors) in early 2020, just before COVID-19 hit, and then weakened again as many industries weakened simultaneously in the spring. Both industries then had a simultaneous sharp rebound, along with most of the rest of the market, through the fall.

The last few months are where we again see a distinct divergence. Software revisions have clearly been losing momentum since September while those of Semis have held up and actually grown somewhat stronger. The spread is now quite wide and at multi-year highs in favor of Semis.

The bottom section of the chart shows the relative returns of the two industries, and we see the clear tendency for relative returns to follow the relative revisions. The relative return series has recently broken out of the range it inhabited for most of 2020, and looks set to follow the relative revisions higher. This suggests that Semiconductors should continue to outperform Software as long as the relative earnings indicators maintain their recent clear bias toward Semis.