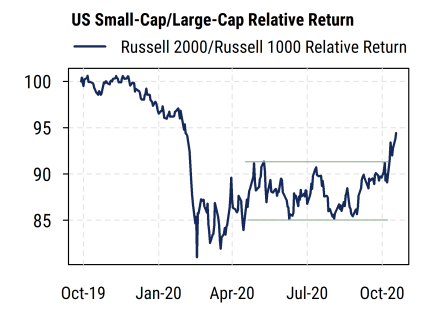

After a long period of either underperformance or mixed relative returns, small-caps in the US are now finally gaining meaningful traction relative to large-caps.

As shown below, the relative return of the small-cap Russell 2000 index versus the large-cap Russell 1000 index has broken out of the range it has been in since June. The latest move started after the Pfizer vaccine news hit on November 9th, after making an initial move in early October.

Our view has long been that small-cap relative performance follows a cyclical pattern, with the best return/risk payoffs coming when the economic and market cycle have been weak and are starting to recover. The early stages of a new expansion or bull market are thus typically the best for small-caps, while the later stages of an expansion or the early phases of a bear market or recession tend to be better for large-caps, especially after accounting for risk.

The current economic cycle has been very unusual. After a record-long expansion, a very rare external shock (a virus) hit, causing far higher amplitude in the economic data (record-setting declines and recoveries), along with historically huge policy interventions (fiscal and monetary stimulus, etc.). The heavy uncertainty about how the current cycle will play out may explain why small-cap relative performance has only recently started to show the upturn we would expect as conditions start to improve after a recession. The recent signs of progress on a vaccine (or multiple vaccines) offer the prospect of “getting back to normal” next year, and may reduce some of the headwinds facing smaller companies relative to larger firms.

Several other indicators suggest the small-cap outperformance trend may be a better bet now than earlier this year.

First, US small-caps are outperforming across all sectors over the last month, indicating a broad-based trend. This includes the Technology sector, where large-cap Tech had outperformed small-cap Tech by 30% for the year through September 1st, but since then small-cap Tech has outperformed its larger brethren by 12%.

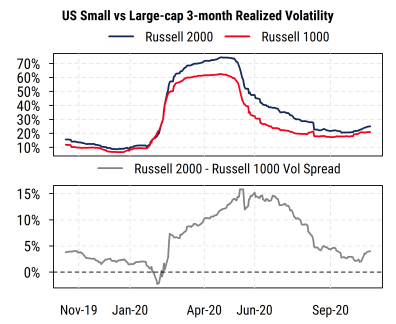

Second, as shown below, the “volatility penalty” for owning small-caps has declined and is now back to relatively low levels. The rolling three-month volatility of the Russell 2000 index has now fallen back to just a small differential over the volatility of large-caps (Russell 1000). That is, investors do not have to take on substantially more risk (volatility) in their portfolios by choosing small-caps over large-caps, as they would have done earlier in the year.

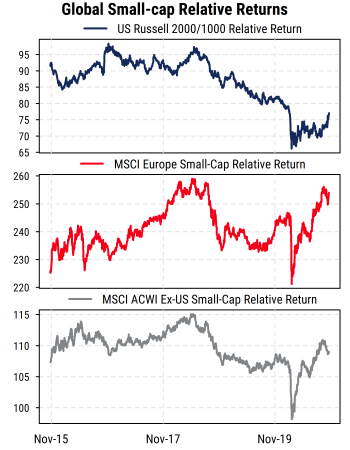

And third, small-caps outside the US have been outperforming for some time now (as shown in the lower two sections of the chart below), and therefore US small-caps may have some catching up to do.

With price activity looking better and the cyclical backdrop potentially becoming more favorable, there could be more room for the recent trend of small-cap outperformance to run over the coming months.