3 February 2022

In our view, equity markets have been shifting toward a backdrop of higher volatility and thus more modest gains relative to the last 18 months. After an all-time high in early January, the S&P 500 recently endured its first 10% decline since September 2020 before rebounding sharply in recent days. This pickup in volatility is consistent with the pullback in fiscal and monetary stimulus, and the natural development of the economic cycle. Bonds are still unattractive on a relative valuation basis compared to stocks, but market and macro conditions are no longer as lopsidedly in favor of stocks as they have been.

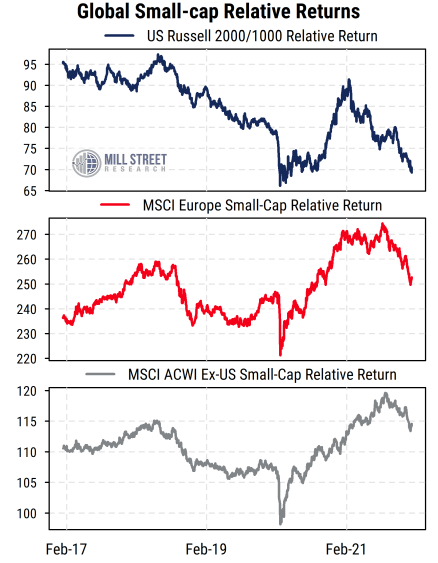

In such conditions, our indicators argue for continuing to favor large-caps over small-caps in equity portfolio allocations. As shown below, small-caps have lagged large-caps in the US for some time (top section), and more recently in Europe and the broader ex-US equity universe.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

Cyclical conditions shifted away from “early cycle” last year, now mid-cycle

Our longer-term (6-12 month) view on the relative outlook for small-caps versus large-caps is driven by a set of cyclical indicators that help us gauge where we are in the market/economic cycle. The basic thesis is that small-caps tend to perform best in the early phase of a cycle, when conditions have been negative and starting to recover, often with the help of policy support (Fed rate cuts, etc.). Smaller companies (which likely lagged in the preceding bear market/recession period) tend to get the biggest relative benefit from such economic and market rebounds.

As the cycle matures, the economic momentum eases along with policy support, and small-caps hand off the relative performance baton to larger-caps in the middle and later phases of a cycle. The indicators we track include economic inputs such as consumer confidence and earnings growth rates, cross-asset inputs like short-term interest rates and credit spreads, equity market indicators of returns and volatility, and a proxy for investor growth expectations based on stock/bond yield differentials.

The general message from those indicators is that after a dramatic but relatively short economic downturn due to COVID in 2020 (which actually came in the context of late cycle conditions in 2018-2019), “early cycle” conditions emerged thanks to massive government stimulus and the development of COVID vaccines. Those conditions led to outperformance by small-cap benchmarks like the Russell 2000 index, and to outperformance by the most volatile stocks in general, from April 2020 through about March 2021.

As 2021 progressed, investors began to consider that the historically aggressive policy support would have to be pared back, and the impact of COVID on many smaller companies was heavier than on larger companies. After a surge in equity prices and narrowing of corporate credit spreads amid signs that corporate earnings and economic data had bottomed and were recovering sharply, the “early cycle” conditions gave way in mid-2021 to current “mid cycle” conditions where growth is still supportive but markets have priced it in and momentum is decelerating. These are often conditions in which policy makers begin to look to scale back stimulus and respond to inflation pressures, as we are seeing now.

After moving from overweight small-caps to neutral in March 2021, we moved to favoring large-caps in September and that remains our view. While recognizing that small-caps have lagged sharply recently and thus could be due a bounce in relative performance at some point, the intermediate-term cyclical view remains in favor of large-caps.

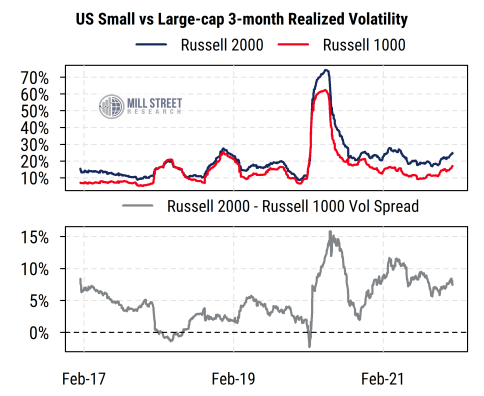

Relative risk is significantly higher for small-caps

For those who might be on the fence, another factor to keep in mind is the relative risk of small-caps versus large-caps. As shown below, small-caps are almost always more volatile than large-caps (based on the volatilities of the Russell 2000 and Russell 1000 indices of small-caps and large-caps respectively), but the volatility differential continues to be especially wide relative to pre-COVID norms. This means that one needs to expect small-caps to produce materially higher returns than large-caps in order to compensate for the higher portfolio risk small-caps bring. So our view under such conditions is that if you are not fully convinced that small-caps will outperform meaningfully, then the benefit of the doubt should go to favoring large-caps due to their lower risk. This has been our stance amid the uncertainty in recent months when many economic and market indicators have remained outside their normal bounds relative to historical norms.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset