30 June 2022

A growing concern among economists and investors is that retailers have been rebuilding inventories rapidly recently, potentially turning what had been partly empty shelves into excess supply. And indeed, the data on inventories held by various categories of US retailers, while lagged, shows evidence of rapidly normalizing (or even excessive) inventories in many areas except for those selling cars and related products. While this might relieve some of the inflation pressure facing consumers and the Fed, it would also imply lower earnings and economic growth, at least for a while.

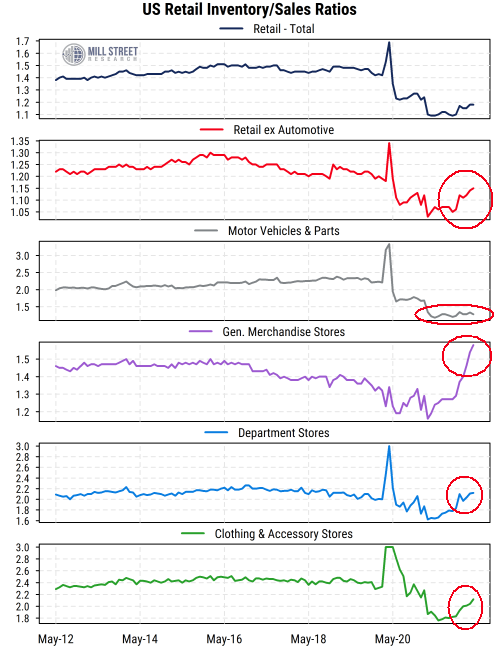

The data in the chart below are the monthly figures from the US Census Bureau, and are as of April 30th (the May data will be released July 15th). They show the ratio of the dollar value of inventories held by retailers to their monthly sales. So a ratio of 1.2, for instance, means that retailers hold goods in inventory with a value of about 1.2 months worth of sales. Using this ratio instead of the absolute level of inventories allows for better comparisons over time as inventories and sales tend to grow together.

Source: Mill Street Research, US Census Bureau

Source: Mill Street Research, US Census Bureau

One of the key features of the post-COVID economic backdrop was shortages of many consumer items (e.g. toilet paper, cleaning supplies, etc.) at stores, reflected in sudden drops in inventory/sales ratios at retailers (after a brief spike due to the initial plunge in sales). Consumers who were mostly stuck at home and who may have received stimulus checks from the government went and cleared the shelves of many items (especially those tied to working/schooling/eating at home), while retailers struggled to restock due to supply chain problems.

So while retailers in aggregate held about 1.5 months worth of sales in inventory before COVID hit, by March of last year that ratio had fallen nearly 30% to about 1.1, and stayed there until about the end of 2021. Since then, the top-line ratio has moved back up to 1.18, clearly an improvement but still well below the pre-COVID norms (top line in chart).

However, the aggregate for all retailers in the US hides considerable variation now, which continues to be felt by consumers, companies, and investors. The big outlier in many ways remains the auto industry, where shortages of inputs to the auto manufacturing process and supply chain issues have kept auto production down even while demand has been very high. This has meant that inventories at auto dealers have remained very low relative to sales. Before COVID, the “motor vehicles and parts” category of retailers held about 2.2 months worth of inventory. By April of last year, that figure had basically fallen in half to about 1.2, and has been holding around 1.3 for most of the time since then (third line in chart). So you are still going to have trouble finding the car you want on a dealer lot.

When we exclude automotive retailers from the aggregate, though, the level of inventories relative to sales has rebounded much more notably. It has risen from 1.05 to 1.15 in the last six months, rapidly approaching the 1.2 level seen before COVID hit (second line in chart).

Within that category, we see an outlier in the opposite direction. General merchandise store (like Wal-Mart or Target for example) have seen a dramatic surge in their inventory/sales ratio (fourth line in chart), going from moderately depressed readings as recently as October to the highest level since 2008 at 1.58. This is likely why some of these retailers have announced negative earnings news recently as they have to now try to bring inventories down to more normal levels.

A somewhat similar but less dramatic picture is seen in the Department Stores category (e.g. Macy’s, Kohl’s, Dillard’s). The inventory/sales ratio in that category has risen back to 2.12, slightly higher than it was at the end of 2019 and in the “normal” range it had inhabited for most of the last decade. So Department Stores may not be overstocked at this point, but in aggregate appear to be “fully stocked” now.

Finally, the Clothing & Accessory Stores category (e.g. Gap, Abercrombie & Fitch, etc.) has seen a sharp rise in inventory levels, but has not yet fully returned to pre-COVID readings.

Overall, we see evidence that many retailers in the US have been increasing their inventory levels relative to sales significantly in the last 6 months (through April), with the glaring exception of auto dealers. This implies less need for inventory rebuilding (which has been contributing to GDP growth recently) and potentially less upward pressure on consumer prices (and even discounts on certain things where inventories have grown too rapidly). This is broadly good news in terms of returning to “normal” economic activity levels and moderating inflation pressures, but could mean a bumpy ride for some retail company earnings for a while, until supply chains, demand, and inventory management have fully stabilized.