18 August 2021

Major equity indices globally have been remarkably stable in recent months, pushing realized volatility readings to very low levels.

Our own research along with that of many others has shown that volatility in equities tends to be persistent in the shorter-term, while tending to mean-revert in the long-term.

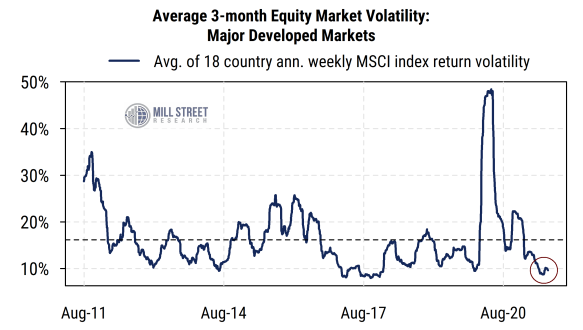

Beyond the movements of a single index like the MSCI ACWI or S&P 500, we can also see that the average three-month volatility across a broad array of major developed markets individually is extremely low (chart below). This average of 18 countries’ volatility (based on their respective MSCI country equity benchmark index) is in the bottom decile of its 10-year range right now. This means that it is not just the dominant US market that has had low volatility, nor is it only the diversification effects that can dampen volatility in a broad global index, it is in fact a global pattern of low equity market volatility across many markets.

While mean-reversion suggests an eventual return to (or above) the average (dashed line), history shows that low volatility periods can last quite a while at times.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

Given the ongoing uncertainty about the path of COVID-19 and its newer variants along with the growing impact of climate-related events (heat, fire, drought, floods, etc.), why are equity markets showing such low volatility recently?

From an investor’s standpoint, volatility in markets is more and more tied to uncertainty regarding fiscal and monetary policy. In 2018-2020, there was increasing uncertainty about both fiscal/trade and monetary policy that combined with a backdrop of sluggish economic growth globally.

These conditions essentially raised investor uncertainty about both future earnings and the discount rate that should apply to those future earnings. The arrival of COVID-19 early last year then injected a huge sudden burst of uncertainty about global health and how governments and health systems would respond.

More recently, however, the level of uncertainty about policy and (to a lesser degree) COVID-19 has declined substantially. Fiscal policy, especially in the US, has been extraordinary in both scale and scope, providing strong support to the economy. Monetary policy has also been extremely supportive, and major central banks have mostly maintained a consistent message that easy monetary conditions will remain in place, with much less likelihood of preemptive tightening.

Source: Mill Street Research, Factset, Bloomberg

Source: Mill Street Research, Factset, Bloomberg

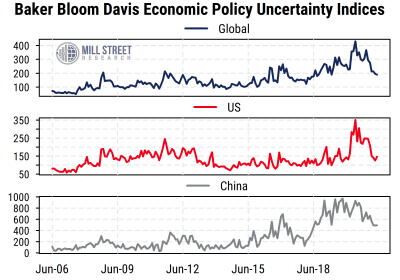

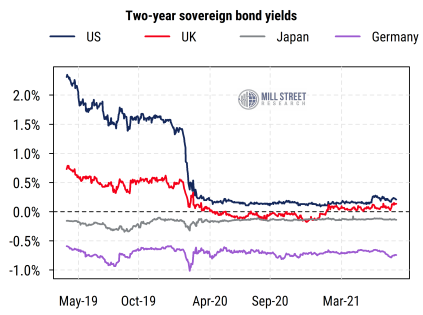

We can see this in measures of economic policy uncertainty derived from newspaper mentions of related topics (top chart above), with a decline visible globally as well as specifically in the US and China. The behavior of short-term interest rates (two-year sovereign bond yields, bottom chart above) in major markets has also been extremely low and stable. This suggests that for at least another year or two, monetary policy is expected to remain both supportive and predictable. “Supportive and predictable” policy, in our view, is a key element in keeping equity market volatility relatively low.