The headlines on Monday (Nov. 9th, 2020) from Pfizer announcing favorable early results in their COVID-19 vaccine trials, while certainly welcome, clearly caught investors off guard. While the major indices were either up or flat on the day, there was a historic level of divergence within the market among the various styles and sectors.

Such extreme rotations remind us that there is risk in the equity markets even when stocks overall do not fall. Investors focused on relative performance likely either had a huge win or huge loss on Monday.

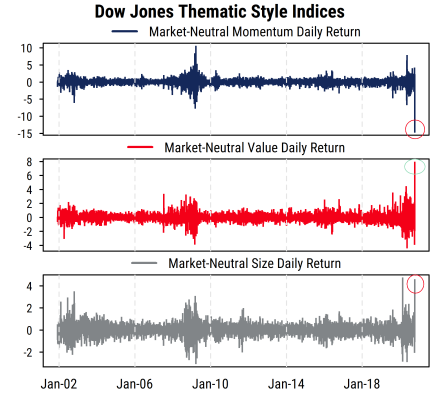

The charts below give some perspective. We highlight returns to widely-used market-neutral factors (styles) that were most impacted yesterday: price momentum, value, and size (small-caps).

The first chart below shows how extreme the returns on Monday were in historical context. We use the daily returns of the Dow Jones Thematic Market Neutral indices for the three styles, data for which goes back to 2002. These indices assume equal dollar amounts invested in long and short portfolios (netting out to zero, or “market neutral”) based on the standard textbook definitions of price momentum (which favors stocks that have outperformed over the last 12 months), value (which favors stocks that have low multiples of price to book value, earnings and cash flow), and size (which favors stocks with lower market capitalizations). The indices are rebalanced quarterly.

The market-neutral Momentum style had the biggest move on Monday among these indices: a daily return of -14%, the largest daily movement (up or down) in the history since 2002. The next most negative day (April 9, 2009) was a -7% return, so Monday was twice the magnitude of the next-worst day. The biggest positive return historically (April 20, 2009) was +10%. The normal range for daily returns since 2002 (where 95% of observations have fallen) has been -1.3% to +1.3%. So Monday’s Momentum return was extraordinarily extreme.

The Value style was one of the big winners, showing a market-neutral return of +8% for the day on Monday. Before this week, the Value factor’s biggest gain was earlier this year (May 26th) at 4.4%, so Monday’s return was almost twice the next-largest move (the biggest decline was similar at -4.3%). The normal range for daily returns for Value since 2002 has been -0.9% to +0.9%.

The Size style also had a big day, showing a +4.5% return, meaning small-cap stocks outperforming large-cap stocks by nearly 5%. This basically matches the previous maximum return of +4.7% from March of this year. The Size factor has had a similar typical daily range as Value (+/- 0.8%).

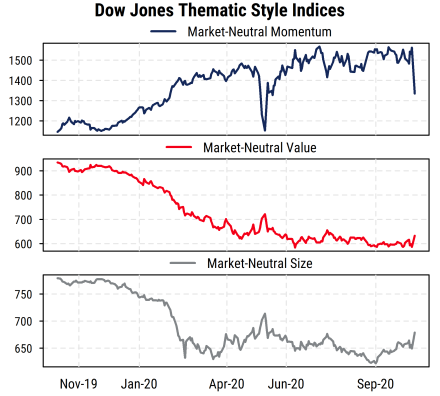

However, context is important here. These extreme moves in styles essentially constitute reversals of the general trend they’ve shown most of this year. Momentum had been one of the stronger styles until this week, while Value and Size had been performing poorly. The second chart below shows the indices themselves (rather than daily changes) over the last 12 months.

We see that market-neutral price Momentum had posted a return of +36% over the 12 months through November 6th, so Monday’s drop cuts into that gain but still leaves the strategy with a positive return for the last 12 months.

Value, by contrast, had been the reverse: it had shown a -37% return (market neutral) through November 6th, so Monday’s gain helped but leaves the style still significantly negative over the last 12 months.

Size (small-caps) had also underperformed coming into this week, showing a -16% return through November 6th. Thus the 4.5% gain reduces the 12-month loss, but still leaves small-caps lagging large-caps by a wide margin over the last year.

The question remains open as to whether Monday’s sharp reversals in relative performance within the major equity market styles (and related sectors) mark the beginning of a durable new trend, or a short-term positioning event that will reverse like a similar event in May/June of this year. Further developments in COVID-19 vaccines, fiscal stimulus plans, and corporate earnings will likely help answer that question, but the uncertainty surrounding these developments means that elevated internal volatility and rotation in stocks may well continue in the coming months.