20 October 2022

The markets have remained focused on the Fed (and occasionally the Bank of England), and the Fed has kept its focus on the trailing reported inflation data (CPI, PCE, etc.) and on the labor market data (job growth, wages, etc.).

The Fed’s view is that inflation cannot sustainably come down to a suitable level (2-3%) unless income growth slows down significantly. That is, income growth must decline to reduce excess demand. This certainly makes sense up to a point, but of course prices are determined by the combination of demand and supply.

There is growing evidence that demand is already slowing (but may not have shown up in year-over-year comparisons yet), and also that supply is increasing, particularly in goods-related parts of the economy (as opposed to services). Oil, semiconductors, shipping capacity, and merchandise retail are examples of areas where demand has fallen and/or supply has increased, keeping prices stable or falling in those areas recently.

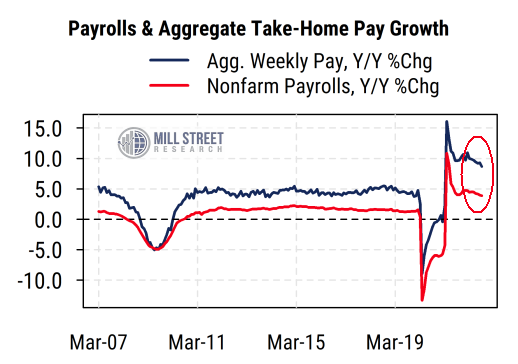

Labor markets: too many workers making too much money

The chart below shows what the Fed is looking at: the year-on-year growth of non-farm payrolls (currently 3.8%) and the growth of total aggregate pay (number of workers X average weekly earnings), which is currently up 8.6% from a year ago. Most of the pre-COVID decade saw aggregate income growth of 4-5%, so 8.6% income growth (though off its highs) is still far too high in the Fed’s eyes, particularly since reported productivity data is far below those levels (higher pay could be non-inflationary if it is compensation for higher productivity).

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

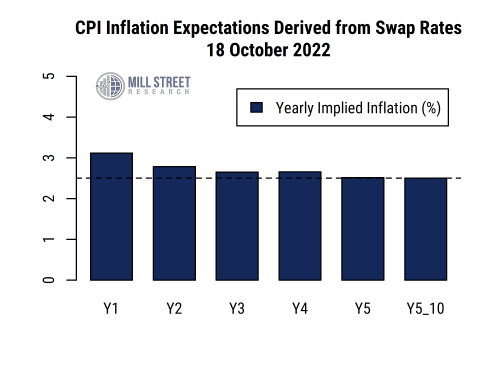

Unlike the Fed, markets see CPI returning to target fairly soon

But market participants clearly have a different view. As shown below, the prices of inflation swaps indicate that investors expect CPI inflation even over the next year to be around 3%, and to remain below that level for the foreseeable future. While the market could of course be wrong, it marks a stark contrast with the current trailing inflation rate of 8.2%, and with the Fed’s projections. The Fed is presumed to be targeting a CPI inflation rate of around 2.5% over the longer-term (dashed line).

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

Markets thus seem to be looking at the forward-looking economic indicators that show signs of slowing of demand and increased supply. It is therefore less surprising that some continue to look for (or argue for) a “pivot” by the Fed to a less aggressive policy stance, but thus far there is little sign that the Fed will alter its stance soon given the trailing data it is watching.

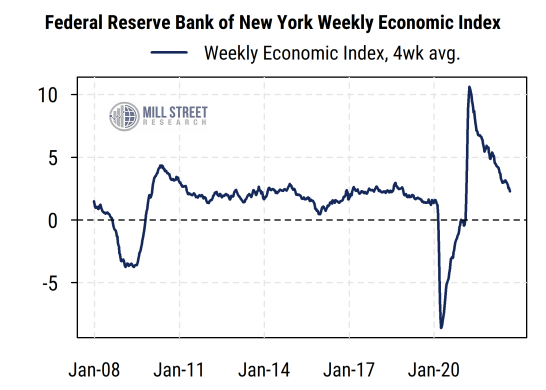

US economy still doing ok, but slowing rapidly

The US economy does not appear to be in recession now, and growth has returned to its pre-COVID range based on the Fed’s Weekly Economic Index (chart below). This index uses higher frequency (daily and weekly) data series such as unemployment claims, withholding taxes, retail sales, steel production, fuel sales, temporary employment, and electricity consumption. The index is scaled to align with the annual real GDP growth rate.

The latest four-week average reading of 2.3% is the lowest since the early 2021 surge, and is now close to the readings seen in much of the 2010-2019 period.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

This data highlights the fact that the US economy is still doing ok, but is rapidly decelerating. Will growth slow and then plateau (a “soft landing”), or keep slowing straight into recession?

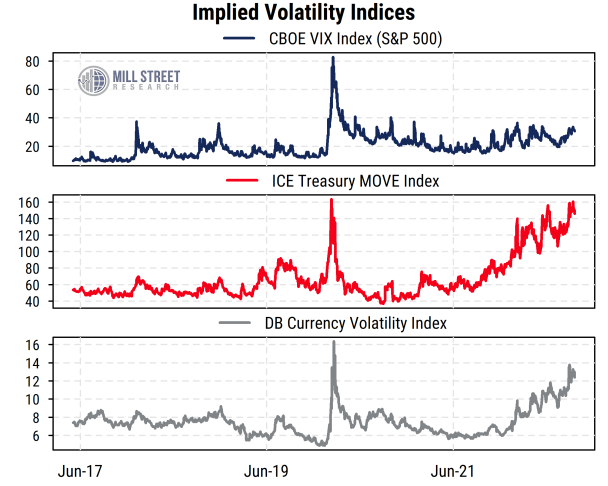

Fed is keeping volatility high across asset classes

The extremely aggressive tightening policy by the Fed and some other central banks has done nothing to soothe investor concerns. Bond and currency market volatility are far higher than normal (chart below), and equities remain very volatile too.

Source: Mill Street Research, Bloomberg

Source: Mill Street Research, Bloomberg

Corporate earnings are likely to be ok for now, and in our view, stocks are still more attractive than bonds on a relative valuation basis. The extreme pessimism toward both stocks and bonds (and optimism toward the US dollar) suggests we may be in the process of forming an equity market low, but it will be hard for stocks to rally sustainably until the investors can more clearly see the end of the Fed tightening cycle. That day may look somewhat closer once the November 2nd Fed meeting is done, but the extreme nature of the current cycle makes it harder than usual to predict policy and its impacts.