24 February 2022

With macro events dominating the headlines (Ukraine, Fed, oil), along with a high-profile “blow up” or two (i.e., Meta, PayPal), it is perhaps not surprising that there has been less attention lately on the overall Q4 earnings season results. And while almost any earnings season might seem disappointing after the string of blockbuster quarters from late 2020 through 2021, the reports for Q4 2021 have in fact been reasonably good overall. Thus far, the company guidance has been sufficiently supportive that analysts are still raising estimates for this year and next, a contrast to the usual pattern of trimming calendar year estimates over the course of a year.

To summarize:

- With 87% of S&P 500 companies having reported, 77% of those have reported better than expected earnings.

- Earnings for Q4 are expected to be up 31% from the year-ago quarter.

- The Technology sector has had the highest proportion of upside surprises at 91%.

- The Utilities has had the lowest proportion of upside surprises at 58%.

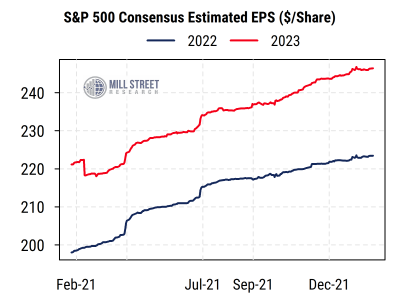

- The calendar 2022 estimate for the S&P 500 was at $221.80 on Jan. 3rd, and has risen to $223.46 currently.

- The 2023 estimate has risen from from $243.62 at the start of the year to $246.41 currently.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

For mid- and small-cap companies, somewhat fewer have reported thus far and the “beat rates” are slightly lower, reflecting the relative earnings strength of large-caps recently.

- For the S&P 400 MidCap index, 78% of the index constituents have reported Q4 earnings so far, with 71% positive surprises. Earnings are on track to show 32% growth from the year-ago quarter.

- For the S&P 600 SmallCap index, 61% of the companies have reported, with 68% reporting positive surprises. Year-on-year earnings growth is expected to be about 37%.

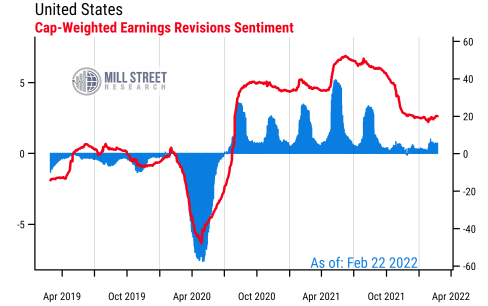

Our cap-weighted earnings estimate revisions data for our broad US stock universe shows analysts still raising estimates on balance, though at a more moderate pace than in 2020/2021.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

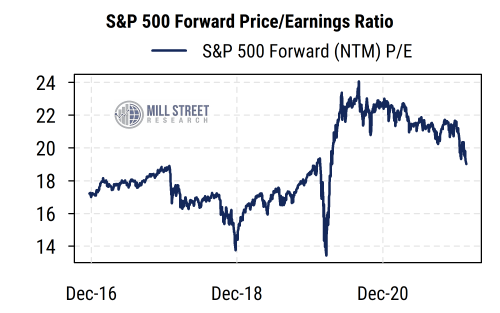

With stock prices pulling back and earnings estimates rising, the S&P 500 forward P/E has declined further, now below 19x.

Source: Mill Street Research, Factset

Source: Mill Street Research, Factset

We view earnings as an ongoing tailwind for stock prices, especially for large-caps. However, the influence of interest rates, inflation, geopolitical risks, etc. can overshadow earnings news and drive risk appetite and valuation multiples up or down. We recently moved from overweight to neutral (benchmark) weight in equities on signs that tactical conditions have deteriorated and market volatility is likely to remain higher this year than last year. Stocks are still more attractively valued than bonds in our view, but valuation is best used as a longer-term tool than a tactical timing indicator.