20 May 2021

In response to client questions, we update some indicators we discussed back in January to address the debate about whether recent market action is indicative of a defensive shift (potential equity market top) or a rotation within equities that maintains a “risk-on” environment. Our current view, as it was in January, is that risk appetite remains broadly intact and the weight of the evidence suggests that we are seeing a rotation, not a “risk-off” environment.

Even as some of the highly valued Growth-oriented “theme” stocks (such as those in the ARK Innovation ETF) have seen sharp sell-offs recently, the broader pattern of positive risk appetite remains intact based on several different measures. The recent market fluctuations have been mostly driven by rotation under the surface, especially the shift from small-cap Growth to large-cap Value.

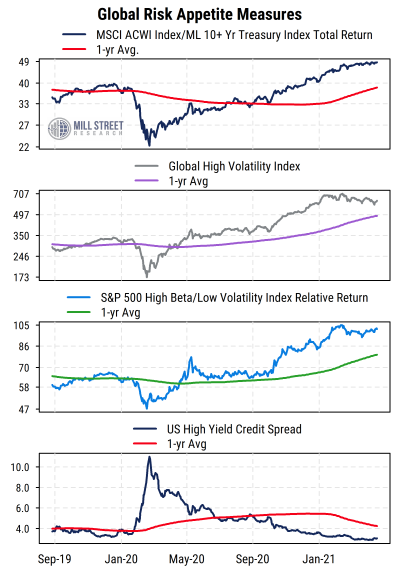

The chart below plots four measures of risk appetite, using both global and US data.

Source: Mill Street Research, Factset, Bloomberg

Source: Mill Street Research, Factset, Bloomberg

The top section shows global stocks (MSCI ACWI index) relative to benchmark 10-year Treasury bond returns. We see that the uptrend in stock/bond relative performance remains intact, and still well above its own one-year average.

The second section shows the absolute returns of our Global High Volatility Index, which captures the returns of the most volatile stocks globally (top decile by historical volatility). It has clearly paused in recent months after huge gains between October and February, but has not reversed into a downtrend. It also remains above its own one-year average.

The third section shows the relative returns of the S&P 500 High Beta versus Low Volatility indices. High beta (riskier) stocks continue to outperform, continuing a stair-step pattern in place since the initial stimulus efforts hit last April.

Finally, the bottom section shows the credit spread (yield differential versus comparable duration Treasury bonds) of the Bloomberg Barclays US High Yield index. We see that credit spreads on risky debt remain at historically low levels, with no signs yet of any stress or risk aversion in credit markets.

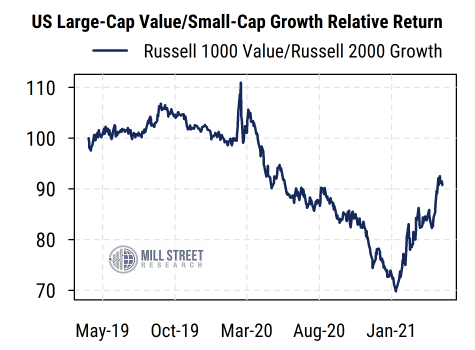

With few top-down signs of a reversal in risk appetite, the source of much of the concern recently has been caused by the dramatic rotation in equity styles under the surface. This is best seen in the relative returns of the Russell large-cap Value versus small-cap Growth indices (chart below). Large-cap Value lagged small-cap Growth badly (blue line falling) for most of the 12 months through February, but the relative return has since rebounded sharply in favor of large-cap Value. Since February 15th, large-cap Value is up about 10% while small-cap Growth is down about -13%, an extreme gap in only about three months. So those who had big gains in small-cap Growth stocks are now feeling differently about the market than large-cap Value investors, but in aggregate the equity market trend remains net positive.

Source: Mill Street Research, Factset, Bloomberg

Source: Mill Street Research, Factset, Bloomberg

It is worth remembering that “high beta” stocks are not restricted to those volatile high-growth Tech-related names that were among the most popular last year and early this year. Indeed, a look at the S&P 500 High Beta index shows a clear Value tilt, with the heaviest weightings in Financials (29%) and Energy (20%), with a relative underweight in Technology (9%). So “risk on” is not equivalent to outperformance by certain highly-valued speculative Growth stocks. And our sector and industry work has been supportive of Value and cyclical areas more broadly for some time now, which is consistent with the macroeconomic backdrop.